Asia Pacific Luxury Car Market outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD5356

December 2024

98

About the Report

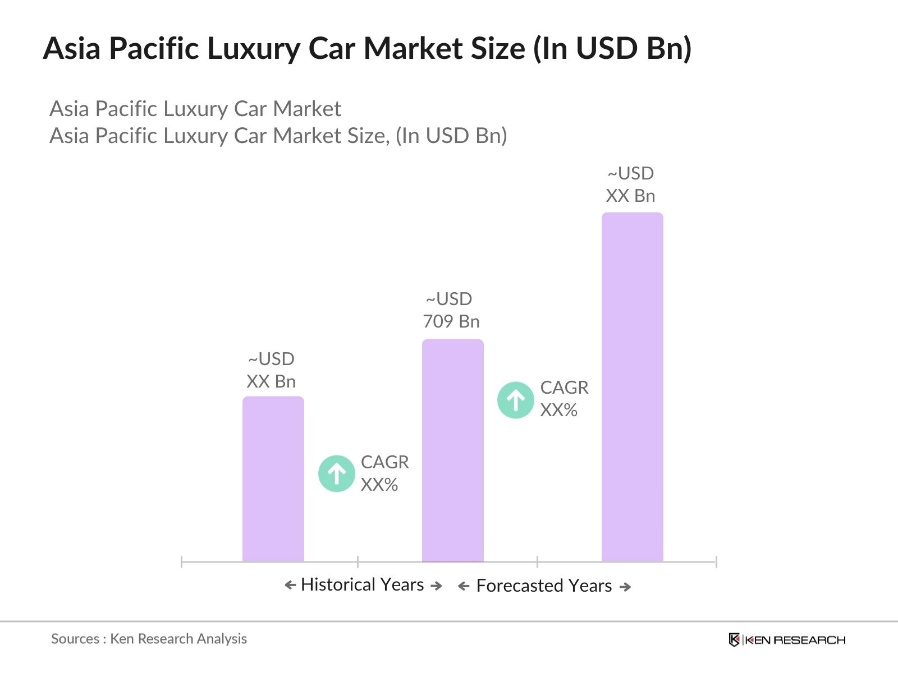

Asia Pacific Luxury Car Market Overview

- The Asia Pacific Luxury Car Market, based on comprehensive analysis of five years of historical data, is valued at USD 709 billion. This market is driven by the region's rapidly growing affluent population, which has significantly increased the demand for high-end vehicles. The adoption of advanced automotive technologies, increased consumer spending, and evolving preferences toward premium, electric, and hybrid luxury cars also contribute to market growth.

- China and Japan dominate the Asia-Pacific luxury car market, with China being the leading market due to its large base of high-net-worth individuals and strong consumer demand for premium automobiles. Japan follows closely, supported by its advanced automotive manufacturing capabilities and significant demand for luxury cars with advanced technology. Both countries have robust infrastructures for luxury car sales and after-sales services, making them key players in the region.

- The Indian government continues to maintain high import taxes on luxury cars to promote local manufacturing. Imported luxury cars face customs duties as high as 110%, in addition to other taxes like GST, which can significantly increase the overall price of luxury vehicles. This policy aims to encourage automakers to set up local production facilities rather than relying on imports. However, these high tariffs challenge foreign luxury car brands entering the Indian market.

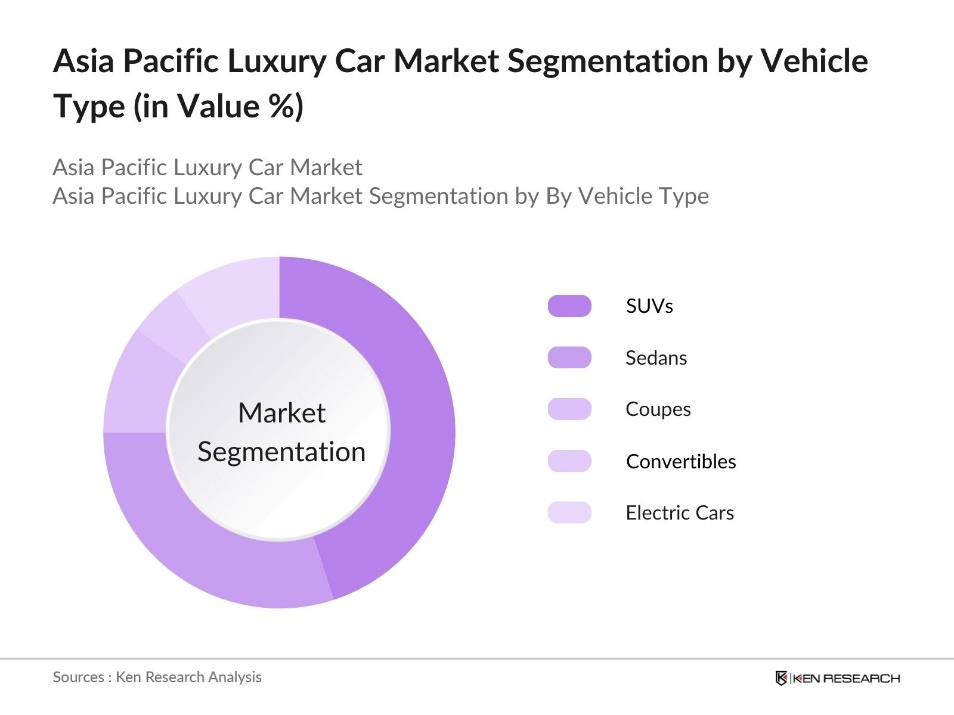

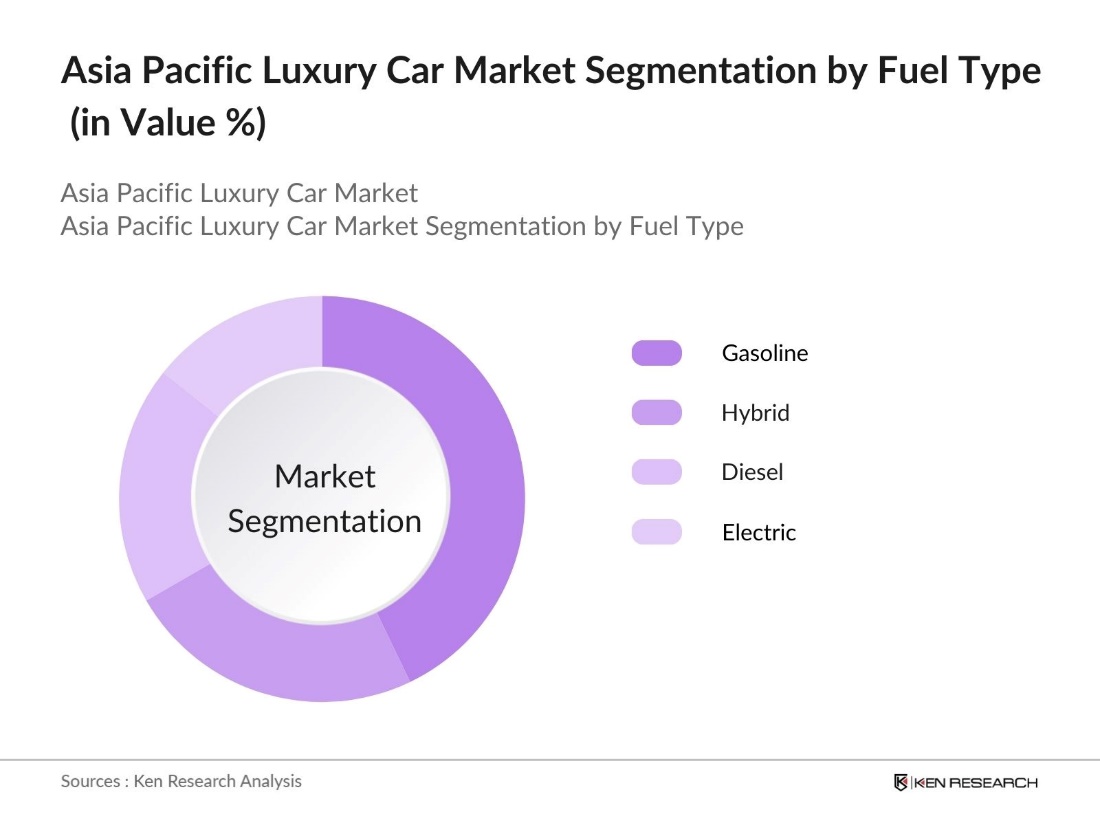

Asia Pacific Luxury Car Market Segmentation

By Vehicle Type: The Asia-Pacific luxury car market is segmented by vehicle type into sedans, SUVs, coupes, convertibles, and electric luxury cars. Recently, SUVs have dominated the market under this segmentation. Their dominance is attributed to their versatility, luxury appeal, and growing popularity among affluent consumers. SUVs offer a mix of comfort, space, and off-road capability, making them a preferred choice in countries like China and Australia, where road conditions and consumer preferences lean towards larger vehicles.

By Fuel Type: The Asia-Pacific luxury car market is segmented by fuel type into gasoline, diesel, hybrid, and electric. Electric luxury cars are witnessing significant growth due to increasing environmental concerns and government incentives promoting electric vehicle (EV) adoption. Countries like China are pushing forward aggressive EV policies, which has spurred a rise in electric luxury car sales, making this segment a rising star within the broader luxury car market.

Asia Pacific Luxury Car Market Competitive Landscape

The market is dominated by global brands that have established strong footholds in the region, leveraging their brand equity, extensive dealership networks, and innovative technologies. Notable players include German automotive giants such as BMW and Mercedes-Benz, as well as electric vehicle pioneers like Tesla. Local manufacturers in China are also gaining traction by offering competitive luxury EV models.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

No. of Models |

EV Models |

Luxury SUV Sales |

Presence in China |

Tech Collaborations |

|

Mercedes-Benz |

1926 |

Stuttgart, Germany |

||||||

|

BMW |

1916 |

Munich, Germany |

||||||

|

Audi |

1909 |

Ingolstadt, Germany |

||||||

|

Tesla Motors |

2003 |

California, USA |

||||||

|

Lexus |

1989 |

Nagoya, Japan |

Asia Pacific Luxury Car Industry Analysis

Growth Drivers

- Rising Disposable Income: The Asia-Pacific region has experienced significant growth in disposable income, a key driver for the luxury car market. China, the largest market in the region, saw its per capita income rise to $12,174 in 2023, further increasing consumer capacity to purchase luxury items. With rising disposable income, the market has seen a steady rise in the demand for luxury cars, particularly in cities such as Beijing, Tokyo, and Singapore.

- Demand for Premium Features: Consumers in the Asia-Pacific region increasingly demand premium features in vehicles, including advanced driver assistance systems (ADAS), autonomous driving capabilities, and high-end entertainment systems. In 2023, the luxury vehicle market in India saw significant growth, with total sales reaching approximately 46,000 to 47,000 units, marking a 21% increase from around 38,000 units in 2022. This surge reflects a broader trend where younger professionals are increasingly opting for high-end automobiles, driven by rising income levels and changing lifestyle preferences.

- Urbanization and Lifestyle Changes: Urbanization in the Asia-Pacific region is driving significant changes in lifestyle that directly impact the luxury car market. As more people move to urban centers, particularly in large cities like Shanghai, Tokyo, and Sydney, the demand for luxury cars has grown. The increasing concentration of wealth and lifestyle preferences in these cities contributes to higher vehicle ownership rates, with luxury cars becoming a status symbol for urban dwellers. Additionally, the improved infrastructure in metropolitan areas supports the use of high-end vehicles, making luxury cars a popular choice among the affluent urban population.

Market Challenges

- High Import Tariffs: High import tariffs present a significant challenge to the luxury car market in the Asia-Pacific region. Many countries impose heavy duties on imported luxury vehicles, making them significantly more expensive than domestically produced alternatives. This makes it difficult for foreign luxury brands to compete on price and limits the market to only the wealthiest consumers. These tariffs often act as a barrier for luxury car manufacturers attempting to penetrate new markets, further reducing their appeal and market share in countries with protectionist trade policies.

- Environmental Regulations: Stringent environmental regulations are a key challenge for traditional luxury car manufacturers in the Asia-Pacific region. Many countries have introduced stricter emission standards, requiring automakers to develop cleaner, more environmentally friendly technologies. These regulations often increase production costs for luxury car manufacturers, particularly those relying on internal combustion engines. At the same time, government policies in several countries are offering incentives for electric and hybrid vehicles, making it harder for traditional luxury vehicles to remain competitive without adopting green technologies.

Asia Pacific Luxury Car Market Future Outlook

The Asia-Pacific luxury car market is poised for significant growth in the coming years, driven by continuous technological advancements, increased investment in electric vehicle infrastructure, and the rising purchasing power of the middle class. Demand for electric luxury vehicles is expected to grow at a fast pace, supported by government policies promoting sustainability and carbon neutrality. The luxury car segment will continue evolving, with automakers focusing on electrification, connectivity, and autonomous driving technologies.

Market Opportunities

- Rise of Electric Luxury Cars: The rise of electric luxury cars is creating significant growth opportunities in the Asia-Pacific region. As consumer preferences shift towards environmentally friendly options, luxury automakers are increasingly focusing on electric models. The growing interest in electric vehicles (EVs) is further supported by government initiatives aimed at promoting green mobility, including investments in charging infrastructure. This combination of consumer demand for sustainability and government backing for EVs has positioned the luxury electric vehicle market for future expansion, offering automakers a chance to tap into a new segment of affluent, eco-conscious buyers.

- Expansion into Tier-2 and Tier-3 Cities: Luxury car manufacturers are increasingly targeting Tier-2 and Tier-3 cities in the Asia-Pacific region, particularly in rapidly growing economies like India and China. As wealth distribution improves and economic growth accelerates in these smaller urban centers, they are becoming attractive markets for luxury brands. The growing affluence in these regions has led to increased demand for premium vehicles, providing luxury car manufacturers with the opportunity to expand beyond traditional metropolitan areas.

Scope of the Report

|

By Vehicle Type |

Sedans SUVs Coupes Convertibles Electric Luxury Cars |

|

By Fuel Type |

Gasoline Diesel Hybrid Electric |

|

By End User |

Individual Buyers Corporate Buyers Rental and Leasing Services |

|

By Sales Channel |

Direct Sales Online Sales Authorized Dealers |

|

By Region |

China Japan South Korea India Australia |

Products

Key Target Audience

High Net-Worth Individuals (HNWIs)

Automotive Dealerships

Luxury Car Manufacturers

Automotive Aftermarket Service Providers

Electric Vehicle Charging Infrastructure Providers

Government and Regulatory Bodies (Ministry of Transport, Energy Regulatory Authorities)

Investor and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Mercedes-Benz

BMW

Audi

Tesla Motors

Lexus

Porsche

Rolls-Royce

Ferrari

Lamborghini

Bentley

Jaguar Land Rover

Volvo

Maserati

Aston Martin

McLaren Automotive

Table of Contents

1. Asia-Pacific Luxury Car Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Luxury Car Segmentation Overview

2. Asia-Pacific Luxury Car Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia-Pacific Luxury Car Market Analysis

3.1. Growth Drivers

3.1.1. Rising Disposable Income (Per Capita Income, Purchasing Power Index)

3.1.2. Demand for Premium Features (Luxury Technology Penetration)

3.1.3. Urbanization and Lifestyle Changes (Urbanization Rate, Vehicle Ownership Rate)

3.1.4. Growing Wealth Concentration (High Net-Worth Individual Growth, Luxury Goods Spending)

3.2. Market Challenges

3.2.1. High Import Tariffs (Luxury Car Import Duties)

3.2.2. Environmental Regulations (Emission Standards, Green Vehicle Policies)

3.2.3. Cost of Ownership (Maintenance Costs, Insurance Premiums)

3.3. Opportunities

3.3.1. Rise of Electric Luxury Cars (Electric Vehicle Adoption, Charging Infrastructure)

3.3.2. Expansion into Tier-2 and Tier-3 Cities (Luxury Car Sales Growth in Emerging Cities)

3.3.3. Collaborative Ventures (Luxury Brand Partnerships, Joint Ventures with Tech Firms)

3.4. Trends

3.4.1. Shift Towards Electric and Hybrid Vehicles (EV Penetration, Fuel Economy Regulations)

3.4.2. Growth in Luxury SUV Segment (Luxury SUV Market Share, Consumer Preference Shift)

3.4.3. Increased Customization and Personalization (Bespoke Features Demand)

3.5. Government Regulations

3.5.1. Emission Control Norms (Euro 6, Local Emission Standards)

3.5.2. Import Tariffs and Duties (Trade Agreements, Luxury Tax Policies)

3.5.3. Incentives for Electric Vehicles (Government Subsidies, EV Incentive Schemes)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia-Pacific Luxury Car Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Sedans

4.1.2. SUVs

4.1.3. Coupes

4.1.4. Convertibles

4.1.5. Electric Luxury Cars

4.2. By Fuel Type (In Value %)

4.2.1. Gasoline

4.2.2. Diesel

4.2.3. Hybrid

4.2.4. Electric

4.3. By End User (In Value %)

4.3.1. Individual Buyers

4.3.2. Corporate Buyers

4.3.3. Rental and Leasing Services

4.4. By Sales Channel (In Value %)

4.4.1. Direct Sales (Showroom Sales, Manufacturer-Owned Stores)

4.4.2. Online Sales (E-Commerce Growth in Luxury Segment)

4.4.3. Authorized Dealers (Authorized Dealer Network Expansion)

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Australia

5. Asia-Pacific Luxury Car Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Mercedes-Benz

5.1.2. BMW

5.1.3. Audi AG

5.1.4. Tesla Motors

5.1.5. Lexus

5.1.6. Porsche AG

5.1.7. Bentley Motors

5.1.8. Rolls-Royce Motor Cars

5.1.9. Ferrari N.V.

5.1.10. Lamborghini S.p.A.

5.1.11. Jaguar Land Rover

5.1.12. Volvo Cars

5.1.13. Maserati

5.1.14. Aston Martin

5.1.15. McLaren Automotive

5.2. Cross Comparison Parameters

5.2.1. Revenue (USD Billion)

5.2.2. Number of Employees

5.2.3. Manufacturing Capacity

5.2.4. Headquarters Location

5.2.5. Number of Models Released Annually

5.2.6. Electric Vehicle Sales

5.2.7. Global Market Share

5.2.8. Customer Satisfaction Index

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. Asia-Pacific Luxury Car Market Regulatory Framework

6.1. Emission Standards Compliance

6.2. Luxury Car Import Regulations

6.3. Electric Vehicle Incentives

6.4. Safety Standards and Crash Testing Regulations

7. Asia-Pacific Luxury Car Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia-Pacific Luxury Car Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Fuel Type (In Value %)

8.3. By End User (In Value %)

8.4. By Sales Channel (In Value %)

8.5. By Region (In Value %)

9. Asia-Pacific Luxury Car Market Analysts Recommendations

9.1. Total Addressable Market (TAM) Analysis

9.2. Serviceable Available Market (SAM) Analysis

9.3. White Space Opportunities

9.4. Key Marketing Initiatives

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase of the research involves identifying critical variables influencing the Asia-Pacific luxury car market, including consumer behavior trends, vehicle sales, and government regulations. Extensive desk research and proprietary databases are utilized to define the key variables.

Step 2: Market Analysis and Construction

In this phase, we compile historical sales data, analyze market penetration rates, and evaluate trends in electric and hybrid luxury vehicles. Data from industry reports and market transactions are used to construct market models, ensuring a comprehensive understanding of market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market growth and shifts in consumer preferences are developed. These hypotheses are then validated through consultations with industry experts via phone interviews, providing practical insights into operational strategies, sales channels, and consumer demands.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing all gathered data and verifying it with key luxury car manufacturers to ensure accurate segmentation, sales figures, and market dynamics. This step ensures the reliability of the market forecast and segmentation.

Frequently Asked Questions

01. How big is the Asia-Pacific Luxury Car Market?

The Asia-Pacific Luxury Car Market is valued at USD 709 billion. The market is driven by the rising demand for high-end vehicles, especially in China and Japan, where the affluent population is growing rapidly.

02. What are the challenges in the Asia-Pacific Luxury Car Market?

The Asia-Pacific Luxury Car Market faces challenges such as high import tariffs, strict environmental regulations, and the high cost of ownership. Moreover, competition from local electric vehicle manufacturers is intensifying, particularly in China.

03. Who are the major players in the Asia-Pacific Luxury Car Market?

Key players in the Asia-Pacific Luxury Car Market include Mercedes-Benz, BMW, Audi, Tesla Motors, and Lexus. These companies dominate due to their strong brand presence, innovative technology, and expansive dealership networks.

04. What are the growth drivers of the Asia-Pacific Luxury Car Market?

The Asia-Pacific Luxury Car Market is driven by increasing disposable incomes, the rise of electric luxury cars, and consumer demand for premium vehicles with advanced technologies. Additionally, government incentives promoting electric vehicles are boosting sales.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.