Asia Pacific M-Commerce Market Outlook to 2028

Region:Asia

Author(s):Paribhasha Tiwari

Product Code:KROD10477

November 2024

81

About the Report

Asia Pacific M-Commerce Market Overview

- The Asia Pacific M-Commerce market, driven by the widespread adoption of mobile devices and robust internet infrastructure, is valued at USD 415 billion based on a historical analysis. This growth is attributed to the increase in mobile penetration across the region and the rise of digital payment platforms. Government initiatives to promote digital economies and cashless transactions further enhance the growth of M-Commerce in Asia Pacific.

- Key cities and countries dominating the M-Commerce market in the Asia Pacific include China, India, and Japan. These nations have seen significant investments in mobile technology, creating a favorable environment for M-Commerce growth. Chinas dominance is driven by its tech giants like Alibaba and Tencent, which have built comprehensive ecosystems that integrate mobile shopping, payments, and financial services, leading to a seamless consumer experience. India and Japan benefit from a growing middle class, increased smartphone penetration, and improvements in digital payment infrastructure.

- Governments in Asia Pacific are increasingly focused on digital economy frameworks that drive m-commerce growth. For example, China's "14th Five-Year Plan" promotes digital economy development, with over USD 30 billion earmarked for digital infrastructure upgrades by 2025. Similarly, the ASEAN Digital Masterplan 2025 is expected to facilitate cross-border e-commerce by improving internet connectivity across member states. These frameworks aim to boost m-commerce by promoting secure, accessible mobile payment platforms and developing a robust digital ecosystem.

Asia Pacific M-Commerce Market Segmentation

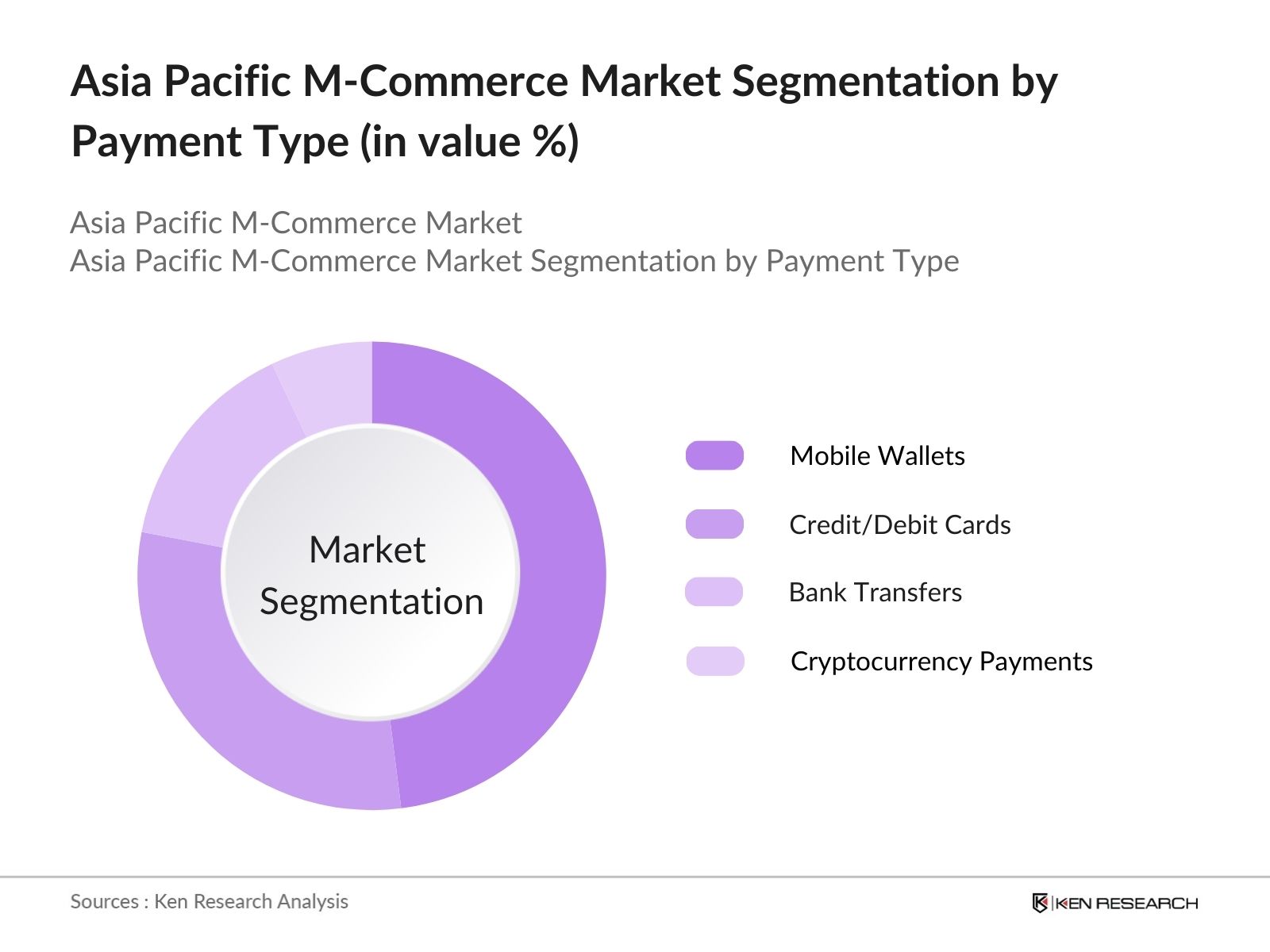

By Payment Type: The Asia Pacific M-Commerce market is segmented by payment type into Mobile Wallets, Credit/Debit Cards, Bank Transfers, and Cryptocurrency Payments. Recently, mobile wallets have gained the largest market share in the region due to their convenience, ease of use, and growing consumer preference for contactless payments. Platforms like WeChat Pay and Alipay in China and Paytm in India have developed strong ecosystems, integrating shopping, bill payments, and financial services, making mobile wallets a dominant force.

By Application: The market is also segmented by application into Retail and E-Commerce, Travel and Hospitality, Food Delivery, and Financial Services. Retail and E-Commerce hold the largest market share in the application segment, primarily due to the rapid growth of online shopping platforms. Companies like Alibaba, Flipkart, and Rakuten have made significant investments in improving user experience through mobile apps, seamless payment gateways, and personalized recommendations, making M-Commerce a vital channel for e-commerce sales.

Asia Pacific M-Commerce Market Competitive Landscape

The Asia Pacific M-Commerce market is highly competitive, with both local players and global tech giants vying for market share. The competitive landscape is dominated by companies that have successfully integrated various services into their platforms, offering consumers a one-stop-shop for M-Commerce.

Asia Pacific M-Commerce Market Analysis

Growth Drivers

- Mobile Internet Penetration (Mobile Device Adoption, Internet Infrastructure) The increasing penetration of mobile internet in Asia Pacific has seen over 1.8 billion mobile internet users across the region by 2024, significantly driving m-commerce adoption. Countries like India, China, and Indonesia are leading in mobile device usage, supported by the expansion of 4G and 5G infrastructure. Governments have invested heavily in internet infrastructure; for example, the Indian government has allocated USD 10 billion for broadband expansion to rural areas, which will boost m-commerce in underserved regions. The rapid adoption of smartphones, especially in Southeast Asia, further supports the m-commerce boom, with a projected addition of 100 million new mobile subscribers by 2025.

- Digital Payment Advancements (E-Wallet Usage, Payment Gateway Integrations) The Asia Pacific region is experiencing an explosive increase in the use of e-wallets, with countries like China already reporting 1.4 billion transactions daily through mobile payments in 2024. Mobile payment platforms such as Alipay, WeChat Pay, and Paytm are integrating advanced payment gateway solutions that simplify cross-border transactions. The rise of QR code payments in markets like Vietnam, Malaysia, and the Philippines is contributing to the rapid growth of digital payments, supporting the regional m-commerce market. Additionally, collaborations between fintech firms and traditional banks are improving the reliability and speed of mobile transactions.

- Government Initiatives (Digital Economy Frameworks, Cashless Society Policies) Governments across the Asia Pacific region are rolling out policies aimed at creating a digital economy. For example, Singapores "Smart Nation" initiative and Indias "Digital India" have created favorable environments for m-commerce expansion. These initiatives focus on reducing cash-based transactions, with India witnessing a dramatic reduction in cash transactions, declining by 200 million transactions daily in favor of mobile-based payments. Meanwhile, Indonesias roadmap to a cashless society, supported by the countrys central bank, aims to increase mobile transactions to 500 million daily by 2025.

Market Challenges

- Data Privacy Concerns (Cybersecurity Risks, GDPR Implementation) With over 3 billion mobile users in Asia Pacific by 2024, data privacy remains a major concern. Governments are responding with stringent data protection laws, such as Chinas Personal Information Protection Law and South Koreas Act on Protection of Personal Information. However, compliance with laws like GDPR for cross-border businesses in APAC is posing significant challenges. Additionally, Asia Pacific reported 10 million cybersecurity breaches involving mobile devices in 2023, which has eroded consumer trust and is seen as a key hurdle for m-commerce expansion.

- Transaction Security (Fraudulent Transactions, Encryption Issues) Asia Pacific's mobile commerce market is highly susceptible to fraudulent transactions, with approximately 1 million daily fraud attempts reported in 2024. Countries such as India and the Philippines face significant challenges in securing mobile transactions due to inadequate encryption protocols. Mobile payment fraud, including identity theft and phishing, has led to the need for stronger authentication measures. Governments and payment platforms are now focusing on blockchain-based solutions to mitigate these risks, but the implementation costs are still high.

Asia Pacific M-Commerce Market Future Outlook

The Asia Pacific M-Commerce market is expected to witness significant growth over the next five years, driven by advancements in mobile technology, the increasing penetration of smartphones, and the shift toward a cashless economy. Governments across the region continue to implement policies promoting digital transactions and financial inclusion, which will accelerate M-Commerce adoption. Furthermore, emerging technologies such as 5G and AI will further enhance user experience and drive M-Commerce growth.

Market Opportunities

- AI-Powered Personalized Shopping (AI-Driven Product Recommendations, Chatbots) Artificial intelligence is playing a pivotal role in reshaping m-commerce in Asia Pacific, with AI-driven product recommendations accounting for nearly 30% of all purchases on mobile platforms in 2024. Chatbots are becoming more sophisticated, handling over 1 billion customer queries monthly across m-commerce platforms like Shopee and JD.com. AI adoption is helping e-commerce players enhance user experiences by offering personalized shopping experiences, improving customer retention rates. Further advancements in AI are expected to revolutionize customer interactions and streamline shopping, driving growth in the m-commerce sector.

- Blockchain for Transaction Security (Decentralized Payments, Digital Identity Verification) Blockchain technology is emerging as a solution to address transaction security concerns in Asia Pacific. By 2025, it is anticipated that over 10% of m-commerce transactions in the region will be processed using blockchain-enabled platforms, ensuring transparency and security. Decentralized payment systems are being piloted in countries like Singapore and Hong Kong, where financial regulators are testing blockchain for cross-border mobile transactions. Blockchains ability to facilitate secure, real-time payments without intermediaries makes it a significant opportunity for enhancing transaction security in the m-commerce landscape.

Scope of the Report

|

By Payment Type |

Mobile Wallets Credit/Debit Cards Bank Transfers Cryptocurrency Payments |

|

By Application |

Retail and E-Commerce Travel and Hospitality Food Delivery Financial Services |

|

By Transaction Type |

Person-to-Merchant (P2M) Peer-to-Peer (P2P) In-App Transactions Direct Carrier Billing |

|

By Technology |

Near-Field Communication (NFC) QR Codes SMS-Based Payments USSD Payments |

|

By Region |

China India Japan Southeast Asia Australia and New Zealand |

Products

Key Target Audience

- M-Commerce Platform Developers

- Mobile Network Operators

- Digital Payment Providers

- Retail and E-Commerce Companies

- Investors and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Information Technology, Ministry of Finance)

- Financial Institutions

- Mobile Device Manufacturers

Companies

Players Mentioned in the Report:

- Alibaba Group

- Tencent Holdings Ltd.

- Paytm

- Grab Holdings

- Ant Financial

- Samsung Pay

- Apple Pay

- Google Pay

- JD.com

- Gojek

Table of Contents

1. Asia Pacific M-Commerce Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Asia Pacific M-Commerce Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Asia Pacific M-Commerce Market Analysis

3.1 Growth Drivers

3.1.1 Mobile Internet Penetration (Mobile Device Adoption, Internet Infrastructure)

3.1.2 Digital Payment Advancements (E-Wallet Usage, Payment Gateway Integrations)

3.1.3 Government Initiatives (Digital Economy Frameworks, Cashless Society Policies)

3.1.4 Increasing E-commerce Adoption (Shifts in Consumer Behavior, Marketplaces)

3.2 Market Challenges

3.2.1 Data Privacy Concerns (Cybersecurity Risks, GDPR Implementation)

3.2.2 Transaction Security (Fraudulent Transactions, Encryption Issues)

3.2.3 Logistics and Supply Chain Issues (Cross-Border Shipping, Last-Mile Delivery)

3.2.4 Consumer Trust in Mobile Payments (Fear of Fraud, Platform Reliability)

3.3 Opportunities

3.3.1 AI-Powered Personalized Shopping (AI-Driven Product Recommendations, Chatbots)

3.3.2 Blockchain for Transaction Security (Decentralized Payments, Digital Identity Verification)

3.3.3 Expansion into Rural Areas (Untapped Markets, Rural Internet Expansion)

3.3.4 Augmented Reality Shopping (AR Try-On Features, Virtual Stores)

3.4 Trends

3.4.1 5G-Enabled M-Commerce Growth (High-Speed Transactions, Real-Time Interactions)

3.4.2 Social Commerce Integration (In-App Purchases, Social Media Platforms)

3.4.3 Subscription-Based Models (Mobile-Based Subscription Commerce, Digital Streaming)

3.4.4 Voice Commerce (Voice-Activated Shopping, Smart Assistants)

3.5 Government Regulations

3.5.1 Data Protection Laws (GDPR, Local Privacy Laws)

3.5.2 Financial Regulatory Requirements (AML, KYC Compliance)

3.5.3 E-Commerce Licensing (Country-Specific E-Commerce Regulations)

3.5.4 Cross-Border Payment Policies (Payment Compliance, Foreign Exchange Restrictions)

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. Asia Pacific M-Commerce Market Segmentation

4.1 By Payment Type (In Value %)

4.1.1 Mobile Wallets

4.1.2 Credit/Debit Cards

4.1.3 Bank Transfers

4.1.4 Cryptocurrency Payments

4.2 By Application (In Value %)

4.2.1 Retail and E-Commerce

4.2.2 Travel and Hospitality

4.2.3 Food Delivery

4.2.4 Financial Services

4.3 By Transaction Type (In Value %)

4.3.1 Person-to-Merchant (P2M)

4.3.2 Peer-to-Peer (P2P)

4.3.3 In-App Transactions

4.3.4 Direct Carrier Billing

4.4 By Technology (In Value %)

4.4.1 Near-Field Communication (NFC)

4.4.2 Quick Response (QR) Codes

4.4.3 SMS-Based Payments

4.4.4 USSD Payments

4.5 By Region (In Value %)

4.5.1 China

4.5.2 India

4.5.3 Japan

4.5.4 Southeast Asia

4.5.5 Australia and New Zealand

5. Asia Pacific M-Commerce Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Alibaba Group

5.1.2 Tencent Holdings Ltd.

5.1.3 Paytm

5.1.4 Grab Holdings

5.1.5 Ant Financial

5.1.6 Samsung Pay

5.1.7 Apple Pay

5.1.8 Google Pay

5.1.9 JD.com

5.1.10 Gojek

5.1.11 Shopee

5.1.12 Lazada

5.1.13 Rakuten

5.1.14 WeChat Pay

5.1.15 Zip Pay

5.2 Cross Comparison Parameters

5.2.1 Mobile Payment Penetration

5.2.2 Transaction Volume

5.2.3 No. of Active Users

5.2.4 Revenue from M-Commerce

5.2.5 Market Share in M-Commerce

5.2.6 Partnerships with E-Commerce Platforms

5.2.7 Average Transaction Size

5.2.8 User Growth Rate

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Asia Pacific M-Commerce Market Regulatory Framework

6.1 Data Protection Standards

6.2 Compliance Requirements

6.3 Certification Processes

7. Asia Pacific M-Commerce Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Asia Pacific M-Commerce Future Market Segmentation

8.1 By Payment Type (In Value %)

8.2 By Application (In Value %)

8.3 By Transaction Type (In Value %)

8.4 By Technology (In Value %)

8.5 By Region (In Value %)

9. Asia Pacific M-Commerce Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial stage involved identifying key stakeholders in the Asia Pacific M-Commerce market, including platform developers, mobile network operators, and financial institutions. Through extensive desk research, secondary data was gathered from trusted proprietary databases and industry reports.

Step 2: Market Analysis and Construction

In this phase, historical data from the Asia Pacific M-Commerce market was analyzed to assess the penetration of mobile payments and the growth of e-commerce applications. Service quality metrics were evaluated to provide a reliable estimate of market revenue.

Step 3: Hypothesis Validation and Expert Consultation

Interviews were conducted with industry experts through computer-assisted telephone interviews (CATIs) to validate our hypotheses and gain insights into M-Commerce trends, technological advancements, and market challenges.

Step 4: Research Synthesis and Final Output

Data collected from experts was cross-referenced with industry reports, resulting in a final comprehensive analysis of the Asia Pacific M-Commerce market, focusing on future growth drivers and key market players.

Frequently Asked Questions

01. How big is the Asia Pacific M-Commerce Market?

The Asia Pacific M-Commerce market is valued at USD 415 billion, with mobile wallets accounting for a significant share of the transaction volume. This valuation is based on extensive historical data and the growing importance of digital payments.

02. What are the challenges in the Asia Pacific M-Commerce Market?

Key challenges in the Asia Pacific M-Commerce market include data privacy concerns, cybersecurity risks, and consumer trust in mobile payments. Additionally, regulatory hurdles related to cross-border payments pose a significant challenge for M-Commerce expansion.

03. Who are the major players in the Asia Pacific M-Commerce Market?

The Asia Pacific M-Commerce market is dominated by tech giants such as Alibaba, Tencent, and Paytm, which have established strong ecosystems integrating digital payments, shopping, and financial services, making them key players in this sector.

04. What are the growth drivers of the Asia Pacific M-Commerce Market?

The primary growth drivers in the Asia Pacific M-Commerce market include the rise of mobile internet penetration, advancements in digital payment infrastructure, and government policies promoting cashless economies across the Asia Pacific region.

Why Buy From Us?

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.