Asia Pacific Polyurea Market Outlook to 2030

Region:Asia

Author(s):Shreya Garg

Product Code:KROD6414

December 2024

96

About the Report

Asia Pacific Polyurea Market Overview

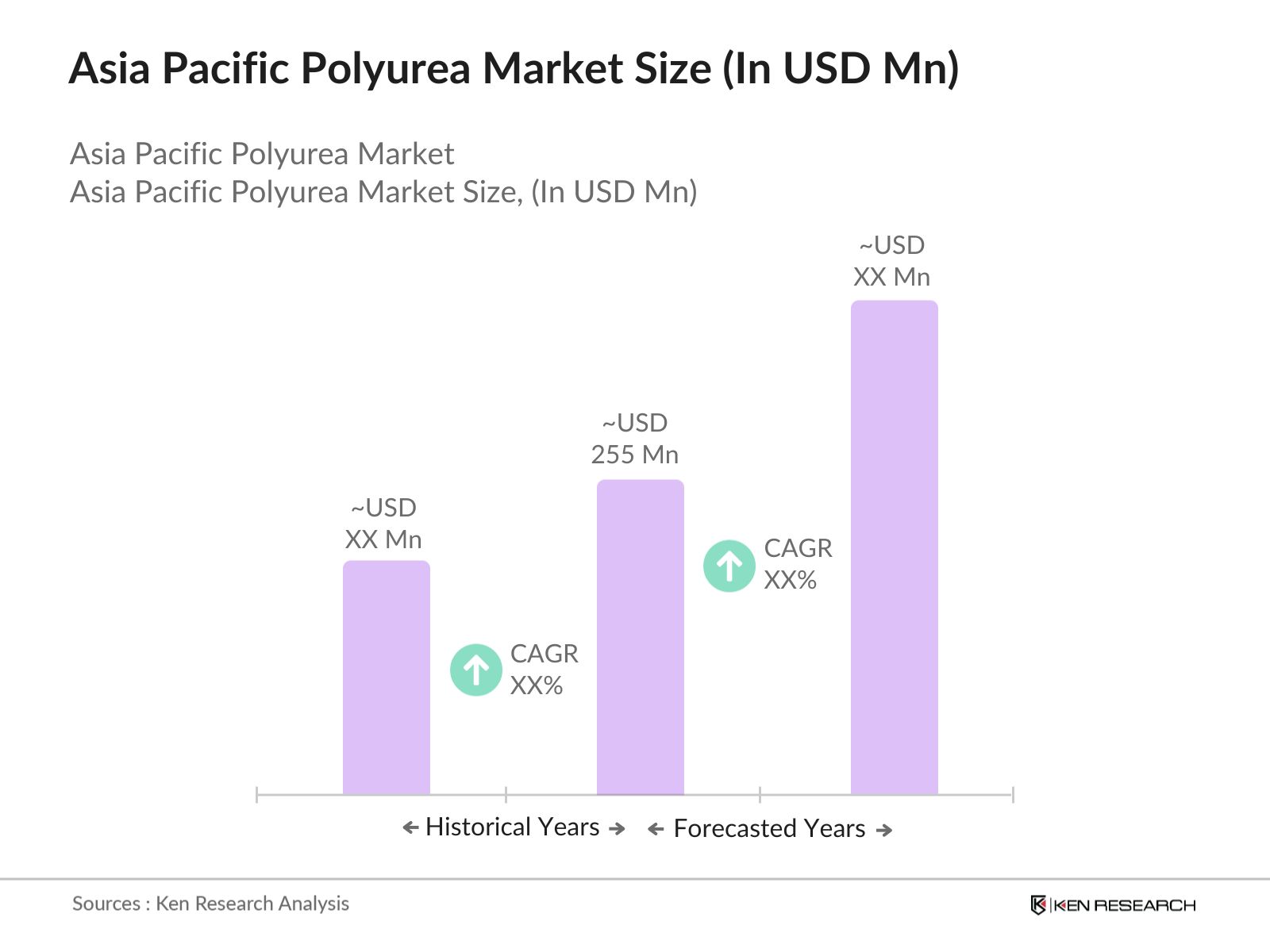

- The Asia Pacific Polyurea market is valued at USD 255 Million, based on a five-year historical analysis. This market's growth is primarily driven by the increasing demand for high-performance coatings across industrial, construction, and automotive sectors. The unique characteristics of polyurea, such as its superior durability, chemical resistance, and fast curing times, have made it the go-to material for industries requiring long-term protection. Infrastructure development and government investment in protective coatings for bridges, tunnels, and marine structures further propel this market's expansion.

- China and Japan dominate the Asia Pacific Polyurea market due to their robust industrial infrastructure and large-scale construction activities. China's extensive infrastructure projects, such as its Belt and Road Initiative, require durable protective coatings like polyurea for longevity and protection against environmental factors. Japan's stringent environmental regulations and a strong focus on sustainable, VOC-compliant coatings have also positioned it as a key market leader in the region. Both countries benefit from advanced manufacturing facilities and established distribution networks, further strengthening their dominance.

- Governments across the Asia Pacific are increasingly promoting sustainable construction practices, which include the use of environmentally friendly materials such as polyurea. In 2024, Japan implemented stricter building regulations that mandate the use of VOC-free coatings in construction projects to reduce environmental pollution. This regulatory push is expected to drive higher demand for polyurea coatings in residential and commercial construction, aligning with the region's broader sustainability goals.

Asia Pacific Polyurea Market Segmentation

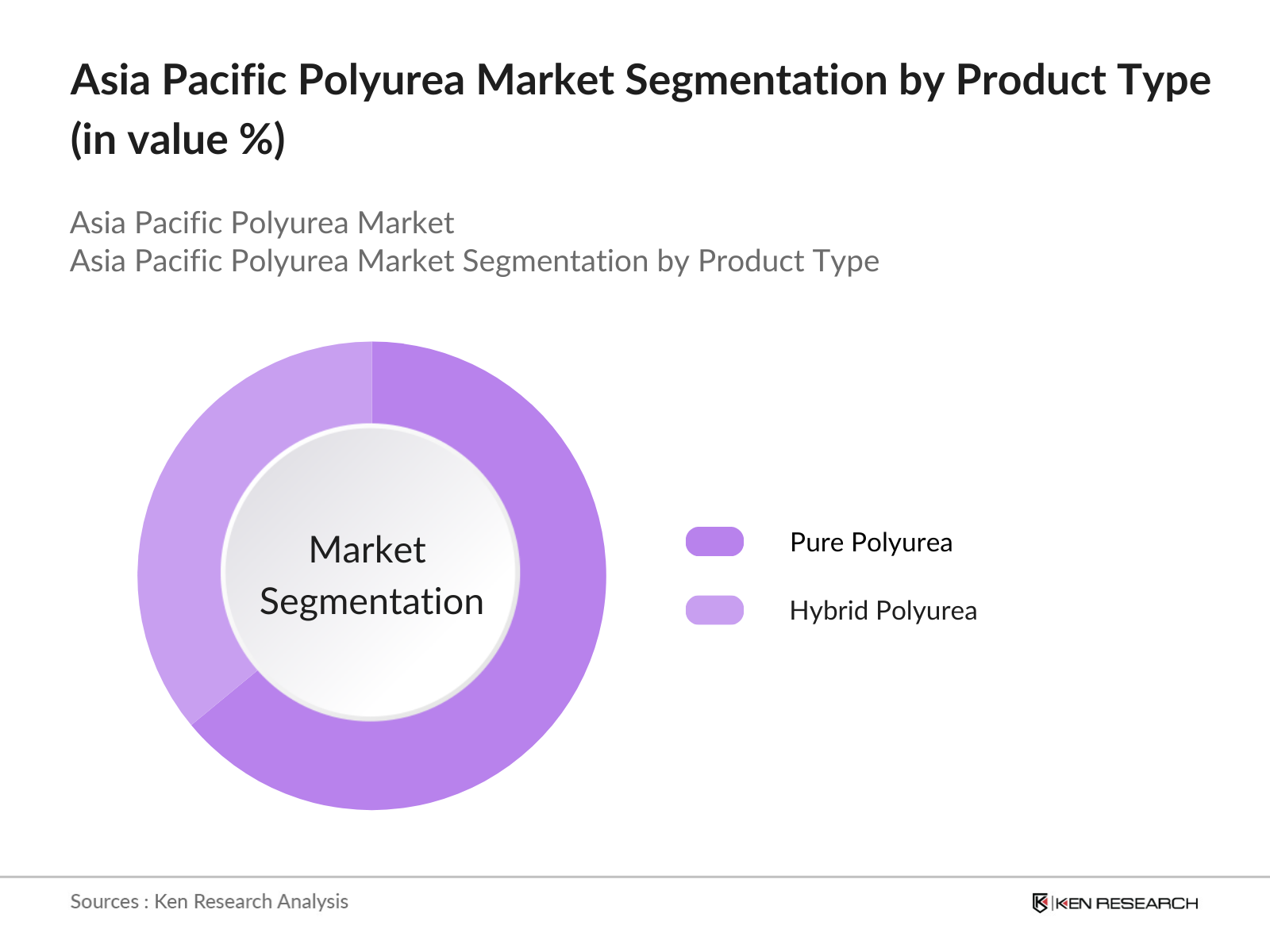

By Product Type: The Asia Pacific Polyurea market is segmented by product type into pure polyurea and hybrid polyurea.

Pure polyurea has gained a dominant market share within this segmentation, owing to its superior physical properties such as rapid curing, high tensile strength, and exceptional resistance to chemicals and abrasion. Industries such as oil and gas, infrastructure, and automotive rely heavily on pure polyurea due to its high-performance characteristics, which offer longer-lasting protection compared to hybrid polyurea.

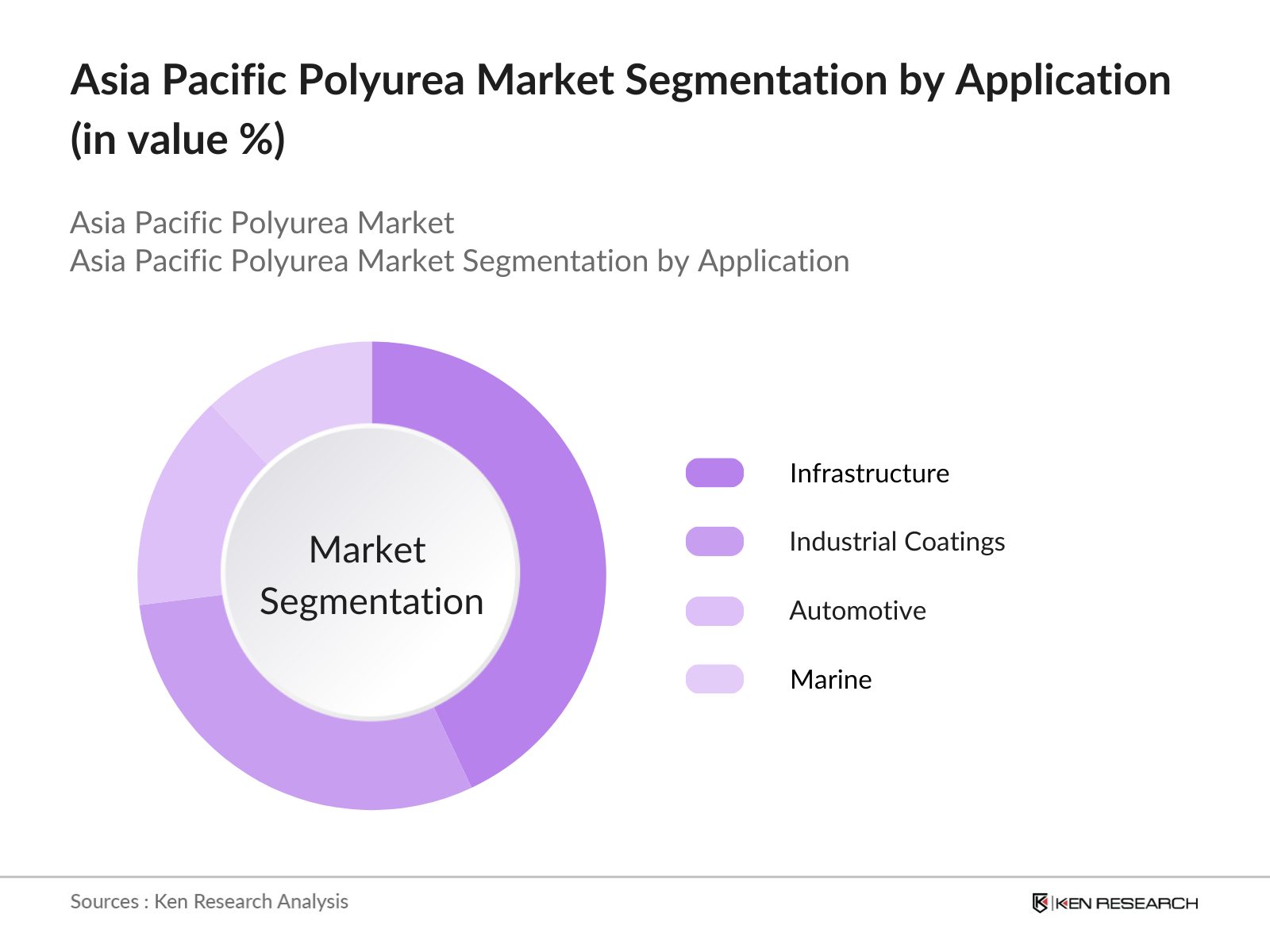

By Application: The market is also segmented by application into industrial coatings, infrastructure, automotive, and marine.

Infrastructure applications are dominating the market, especially in sectors like bridge and tunnel construction, where polyurea's durability and waterproofing properties are essential. The rapid urbanization and government-led infrastructure projects across countries such as China, India, and Australia are fueling the demand for polyurea coatings in construction, leading this application to capture the largest market share.

Asia Pacific Polyurea Market Competitive Landscape

The Asia Pacific Polyurea market is dominated by a few key players who hold a significant influence through their extensive product offerings, global reach, and technological advancements. Major players focus on continuous research and development to enhance product performance and increase their market share.

|

Company Name |

Establishment Year |

Headquarters |

R&D Expenditure |

Global Reach |

Product Portfolio |

Technology Focus |

Strategic Alliances |

Market Share |

|

Nukote Coating Systems Intl. |

1995 |

Houston, USA |

||||||

|

PPG Industries |

1883 |

Pittsburgh, USA |

||||||

|

Sherwin-Williams Co. |

1866 |

Cleveland, USA |

||||||

|

Huntsman Corporation |

1970 |

The Woodlands, USA |

||||||

|

BASF SE |

1865 |

Ludwigshafen, Germany |

Asia Pacific Polyurea Market Analysis

Growth Drivers

- Industrial Applications: The Asia Pacific region is witnessing significant growth in industries such as oil & gas and chemical containment, where polyurea is widely used due to its high durability and resistance to harsh chemicals. As of 2024, industrial activities in sectors like oil and gas are expected to expand by over $300 billion across the region, increasing the demand for polyurea coatings to protect storage tanks, pipelines, and other infrastructure. This rise in demand is driven by the need for robust materials that can withstand extreme conditions, enhancing the lifespan of equipment and reducing maintenance costs.

- Waterproofing and Corrosion Protection: In the infrastructure and marine sectors, polyurea is gaining traction for its superior waterproofing and corrosion-resistant properties. With the Asia Pacific region experiencing a $2 trillion investment in infrastructure development by 2024, particularly in China and India, polyurea coatings are being increasingly used to protect bridges, tunnels, and marine structures from water damage and corrosion. This has led to substantial growth in the adoption of polyurea for both public and private infrastructure projects, contributing to the long-term sustainability of these assets.

- Sustainability Concerns: The growing emphasis on environmental sustainability in the Asia Pacific is driving the demand for polyurea coatings that are free from volatile organic compounds (VOCs) and comply with green building standards. Government initiatives promoting eco-friendly construction materials are pushing builders and contractors toward VOC-free coatings. In 2024, with stringent green building regulations in major markets like Japan and Australia, the use of VOC-free polyurea coatings in the construction sector is expected to rise significantly. This aligns with the region's broader goals of reducing carbon emissions and fostering sustainable urban development.

Market Challenges

- Raw Material Availability: A significant challenge for the polyurea market in the Asia Pacific is the fluctuating availability of raw materials. Polyurea production relies heavily on chemicals like isocyanates, which are subject to supply chain disruptions and pricing volatility. In 2024, the regions chemical supply chain faced disruptions due to geopolitical tensions and trade restrictions, leading to shortages and increased costs for manufacturers. This has hindered the production capacity of polyurea manufacturers, making it difficult to meet rising demand in sectors like construction and industrial applications.

- Skilled Labor Shortages: The application of polyurea coatings requires highly skilled labor due to the technical complexity involved in spray techniques and surface preparation. However, the Asia Pacific region is experiencing a shortage of skilled workers in this domain, particularly in emerging economies like Vietnam and the Philippines. In 2024, the construction industry reported a shortfall of over 10 million skilled workers across the region, affecting the ability to execute polyurea-based projects efficiently and causing delays in infrastructure development timelines.

Asia Pacific Polyurea Market Future Outlook

The Asia Pacific Polyurea market is poised for significant growth over the next five years, driven by advancements in application technologies and the increasing adoption of eco-friendly coatings. Government infrastructure investments, particularly in developing countries, coupled with growing demand for durable, fast-curing materials in sectors like construction and automotive, will contribute to this market's expansion. Additionally, innovation in polyurea formulations that improve chemical resistance and environmental compliance will open up new opportunities in industrial coatings and defense applications.

Future Market Opportunities

- Expansion in Emerging Economies: The rapid industrialization and urbanization in emerging Asia Pacific economies like Indonesia, Vietnam, and Thailand present significant opportunities for polyurea manufacturers. With infrastructure investment expected to exceed $600 billion in Southeast Asia by 2025, demand for protective coatings in construction and industrial sectors is set to rise. These markets are also witnessing increased adoption of polyurea in sectors like automotive and defense, driven by government initiatives to modernize infrastructure and manufacturing capabilities.

- Growing Adoption in Automotive and Defense Industries: The automotive and defense industries are increasingly adopting polyurea coatings for their superior abrasion resistance and durability. In 2024, the Asia Pacific automotive industry, with projected revenues exceeding $1 trillion, saw a rise in the use of polyurea for underbody coatings, soundproofing, and corrosion protection in vehicles. Similarly, defense sectors across countries like India and South Korea are leveraging polyureas ballistic resistance properties for protective coatings in military vehicles and equipment, creating new growth avenues for polyurea manufacturers.

Scope of the Report

|

By Product Type |

Pure Polyurea Hybrid Polyurea |

|

By Application |

Industrial Coatings Infrastructure Automotive Marine |

|

By Raw Material |

Aromatic Isocyanates Aliphatic Isocyanates |

|

By Technology |

Hot Spray Polyurea Cold Spray Polyurea |

|

By Region |

China India Japan Australia Southeast Asia |

Products

Key Target Audience

Polyurea Coatings Manufacturers

Automotive OEMs

Infrastructure Developers

Marine and Shipbuilding Companies

Chemical Suppliers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Environmental Protection Agencies, Building and Construction Authorities)

Research and Development Institutions (focused on material science)

Companies

Major Players

Nukote Coating Systems International

PPG Industries

Sherwin-Williams Company

Huntsman Corporation

BASF SE

Rhino Linings Corporation

Covestro AG

Sika AG

Teknos Group

Versaflex Inc.

Table of Contents

1. Asia Pacific Polyurea Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Segmentation Overview

2. Asia Pacific Polyurea Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Polyurea Market Analysis

3.1. Growth Drivers (e.g., High Durability, Rapid Curing Time, and Environmental Regulations)

3.1.1. Industrial Applications (Oil & Gas, Chemical Containment)

3.1.2. Waterproofing and Corrosion Protection (Infrastructure and Marine Sectors)

3.1.3. Sustainability Concerns (VOC-Free Coatings and Compliance with Green Building Standards)

3.1.4. Innovation in Polyurea Formulations

3.2. Market Challenges (e.g., High Production Costs and Technical Barriers)

3.2.1. Raw Material Availability

3.2.2. Skilled Labor Shortages

3.2.3. Technical Complexity in Application

3.3. Opportunities (e.g., Increasing Infrastructure Investments and Emerging Markets)

3.3.1. Expansion in Emerging Economies

3.3.2. Growing Adoption in Automotive and Defense Industries

3.3.3. Technological Advancements in Spray Application Techniques

3.4. Trends (e.g., R&D in High-Performance Polyurea Systems)

3.4.1. Enhanced Chemical Resistance Coatings

3.4.2. Smart Polyurea Coatings for Temperature and Moisture Sensitivity

3.4.3. Rise in Use of Polyurea in Construction and Mining Sectors

3.5. Government Regulations

3.5.1. VOC Regulations and Green Certifications

3.5.2. National Coatings and Linings Standards

3.5.3. Import-Export Policies for Raw Materials

3.6. SWOT Analysis

3.7. Value Chain Analysis

3.8. Porters Five Forces Model (Threat of Substitutes, Bargaining Power of Buyers, etc.)

3.9. Competitive Landscape

4. Asia Pacific Polyurea Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Pure Polyurea

4.1.2. Hybrid Polyurea

4.2. By Application (In Value %)

4.2.1. Industrial Coatings (Protective Coatings, Linings)

4.2.2. Infrastructure (Bridges, Tunnels, Dams)

4.2.3. Automotive (Underbody Coatings, Truck Bed Liners)

4.2.4. Marine (Hull Coatings, Deck Protection)

4.3. By Raw Material (In Value %)

4.3.1. Aromatic Isocyanates

4.3.2. Aliphatic Isocyanates

4.4. By Technology (In Value %)

4.4.1. Hot Spray Polyurea Coating

4.4.2. Cold Spray Polyurea Coating

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. Southeast Asia (Vietnam, Indonesia, Thailand)

5. Asia Pacific Polyurea Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Nukote Coating Systems International

5.1.2. PPG Industries

5.1.3. Sherwin-Williams Company

5.1.4. Versaflex Inc.

5.1.5. Huntsman Corporation

5.1.6. BASF SE

5.1.7. Bayer AG

5.1.8. Rhino Linings Corporation

5.1.9. Specialty Products Inc.

5.1.10. Graco Inc.

5.1.11. Teknos Group

5.1.12. Sika AG

5.1.13. Covestro AG

5.1.14. Dorf Ketal Chemicals

5.1.15. VIP Coatings International

5.2. Cross Comparison Parameters (Inception Year, Market Presence, Number of Employees, Annual Revenue, Product Portfolio, Application Industries, Market Reach, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers & Acquisitions, Joint Ventures, New Product Launches)

5.5. Investment and Funding Analysis

5.6. Innovation and R&D Focus Areas

5.7. Mergers and Acquisitions

6. Asia Pacific Polyurea Market Regulatory Framework

6.1. Industry Standards and Certifications

6.2. Compliance with Environmental Regulations (VOC Restrictions, Green Building Codes)

6.3. Certification Requirements for Product Approvals

7. Asia Pacific Polyurea Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Polyurea Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Raw Material (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Polyurea Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Market Expansion Strategies

9.3. White Space Opportunities

9.4. Product Development and Innovation Strategies

Research Methodology

Step 1: Identification of Key Variables

This step includes defining critical factors affecting the polyurea market in the Asia Pacific, such as raw material availability, environmental regulations, and technology advancements. Extensive desk research and stakeholder interviews are conducted to identify these variables.

Step 2: Market Analysis and Construction

In this phase, data on past market performance is collected and analyzed. This includes evaluating the market size, key growth drivers, and application areas. Industry reports and databases are used to verify data accuracy.

Step 3: Hypothesis Validation and Expert Consultation

Market trends and hypotheses are validated through interviews with industry experts and polyurea manufacturers. Their insights help to refine the market projections and validate data accuracy.

Step 4: Research Synthesis and Final Output

The final phase consolidates all data into actionable insights, verified by cross-referencing various market reports and statistics. The report output includes detailed analysis and market forecasts.

Frequently Asked Questions

01. How big is the Asia Pacific Polyurea Market?

The Asia Pacific Polyurea Market is valued at USD 255 Million, driven by increasing demand from the infrastructure and automotive sectors, where polyurea's durability and protective qualities make it the preferred material for coatings.

02. What are the key challenges in the Asia Pacific Polyurea Market?

Key challenges include high production costs, limited skilled labor for application, and technical complexities in ensuring proper spray applications across varied industrial uses. Raw material volatility also poses a challenge to the industry.

03. Who are the major players in the Asia Pacific Polyurea Market?

Major players in the market include Nukote Coating Systems International, PPG Industries, Sherwin-Williams Company, Huntsman Corporation, and BASF SE. These companies lead due to their innovation in polyurea formulations and global reach.

04. What are the growth drivers for the Asia Pacific Polyurea Market?

Growth drivers include rising investments in infrastructure, demand for eco-friendly and durable coatings, and the expanding applications of polyurea in the automotive and industrial sectors.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.