Europe Automated External Defibrillator (AED) Market Outlook to 2030

Region:Europe

Author(s):Shreya Garg

Product Code:KROD1326

November 2024

86

About the Report

Europe Automated External Defibrillator (AED) Market Overview

The Europe Automated External Defibrillator (AED) market was valued at USD 350 million in 2023, driven by increased adoption in public spaces, hospitals, and workplaces. The growing prevalence of cardiovascular diseases, particularly sudden cardiac arrest (SCA), has been a major driver, as around 350,000 cardiac arrests occur in Europe annually. In addition, regulations mandating AED installation in various public spaces have further boosted market demand.

Key players dominating the European AED market include Philips Healthcare, ZOLL Medical Corporation, Cardiac Science, Nihon Kohden, and Schiller AG. These companies have led the market through product innovation, strong distribution networks, and strategic partnerships with public health organizations. Their focus on R&D has led to improvements in AED usability and accessibility, ensuring compliance with European medical standards.

In 2023, ZOLL Medical Corporation launched its new AED 3 model, which provides real-time feedback for optimal chest compression during resuscitation efforts. This innovation is expected to improve survival rates in cardiac arrest cases by offering responders critical real-time guidance. The launch highlights the ongoing trend of technological advancements in the AED market aimed at increasing survival rates in emergencies.

Germany has dominated the AED market in Europe in 2023. This dominance can be attributed to Germany's well-established healthcare infrastructure, stringent regulations regarding workplace safety, and robust public health campaigns promoting AED use. Additionally, the country’s rapid adoption of digital healthcare solutions has further supported AED deployment in hospitals, schools, and public spaces.

Europe Automated External Defibrillator (AED) Market Segmentation

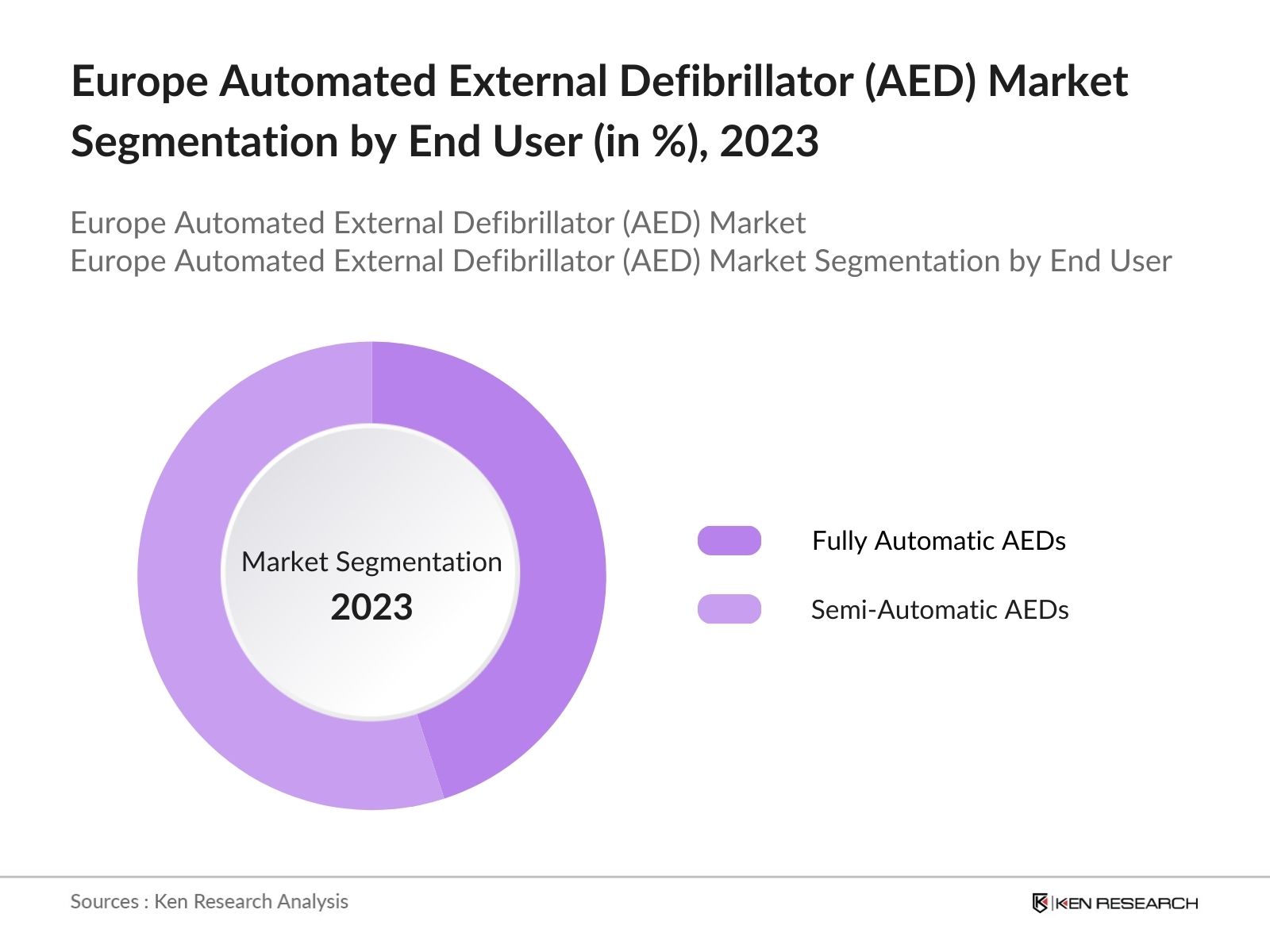

By Product Type: The market is segmented by product type into Fully Automatic AEDs and Semi-Automatic AEDs. In 2023, semi-automatic AEDs held the dominant market share due to their widespread use in hospitals and public institutions. Semi-automatic AEDs are preferred because they allow medical personnel more control over shock delivery, enhancing precision during critical moments.

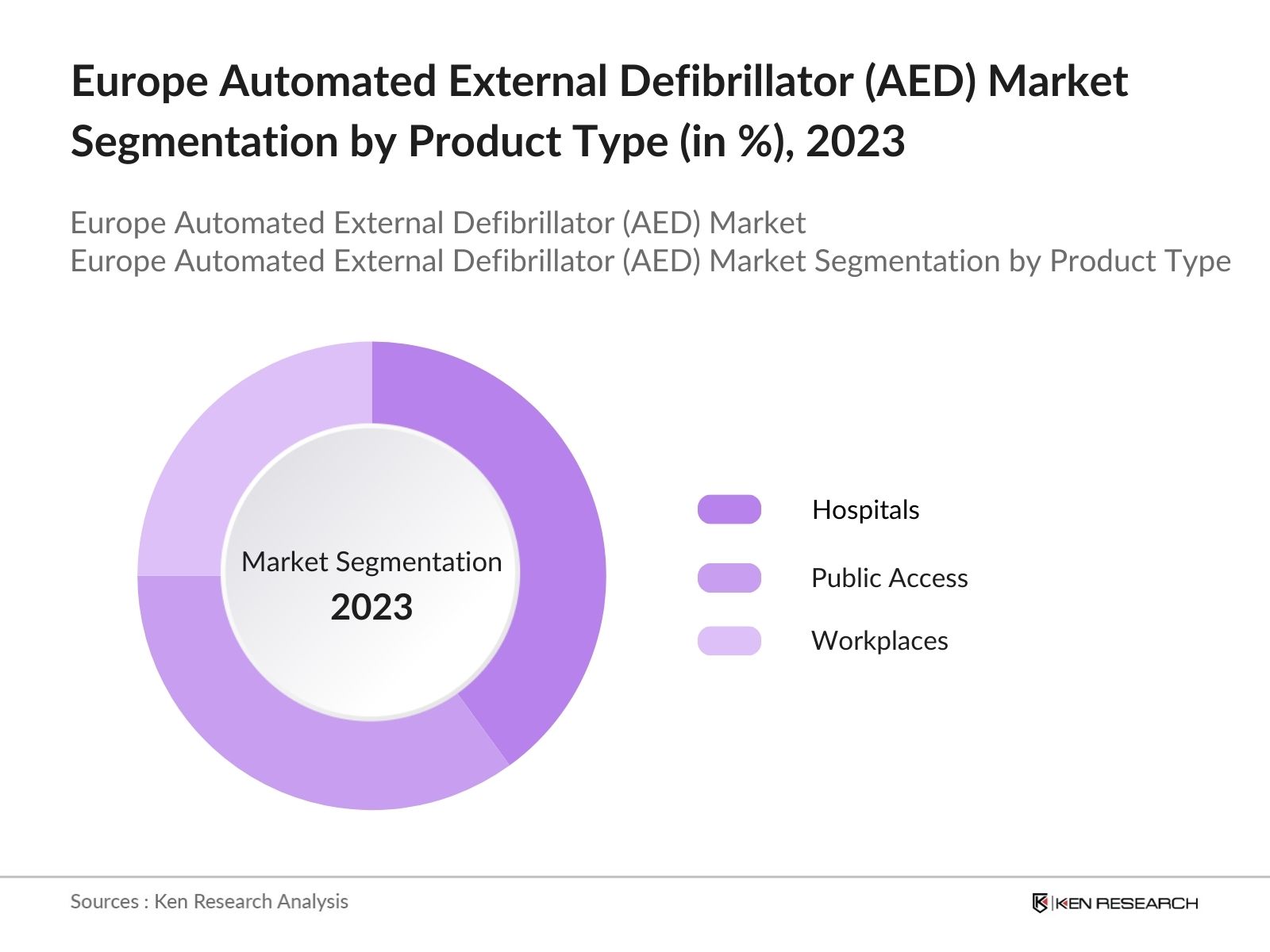

By End-User: The market is segmented by end-user into Hospitals, Public Access Settings, and Workplaces. In 2023, hospitals accounted for the largest market share, owing to the high demand for reliable emergency medical equipment. Hospitals utilize AEDs in both emergency rooms and for post-cardiac surgery care, making them essential in medical institutions.

By Region: The market is divided into Germany, France, United Kingdom, Sweden, Italy and Rest of Europe. In 2023, Germany holds the largest share of the market in Europe, driven by strong healthcare infrastructure, high government spending on public health, and widespread adoption of AEDs in workplaces and public areas. Germany's proactive public health campaigns and advanced medical technology landscape further cement its dominance in the market.

Europe Automated External Defibrillator (AED) Market Competitive Landscape

|

Company Name |

Establishment Year |

Headquarters |

|

Philips Healthcare |

1891 |

Netherlands |

|

ZOLL Medical Corp. |

1980 |

United States |

|

Cardiac Science |

1991 |

United States |

|

Nihon Kohden |

1951 |

Japan |

|

Schiller AG |

1974 |

Switzerland |

- ZOLL Medical Expands Distribution Network In 2023, ZOLL Medical expanded its AED distribution network across Europe by partnering with several large healthcare organizations. This partnership allowed ZOLL to distribute an additional 10,000 AEDs across high-risk areas, including airports, train stations, and sports stadiums. The expansion is expected to improve accessibility to AEDs in critical locations where cardiac arrest incidents are more likely to occur.

- Philips Launches New AED Model In 2024, Philips introduced a new AED model with enhanced connectivity features that allow real-time data transmission to emergency services. The new model has been widely adopted in hospitals and public spaces across Europe, with 8,000 units sold within the first quarter of 2024. This development aligns with the growing demand for connected medical devices that can provide immediate feedback to first responders during emergencies.

Europe Automated External Defibrillator (AED) Industry Analysis

Growth Drivers

- Increased Incidence of Cardiovascular Diseases The rise in cardiovascular diseases across Europe is a significant driver for AED adoption. In 2024, it is estimated that over 11 million people in Europe suffer from coronary heart disease, with nearly 350,000 sudden cardiac arrest cases reported annually. This rising prevalence has resulted in greater demand for life-saving AEDs in public spaces, hospitals, and workplaces to address cardiac emergencies immediately. Countries like France and Germany have increased their public healthcare expenditure to over $600 billion collectively, with a portion allocated to improving emergency response equipment, including AEDs.

- Government Investment in Public Health Infrastructure In 2023, the European Union announced an investment of $8 billion towards enhancing public health infrastructure, with a particular focus on life-saving technologies such as AEDs. This funding has been allocated to various countries to increase AED availability in key locations, including schools, transport hubs, and workplaces. For instance, the UK government introduced a scheme to deploy 1,000 AEDs in high-traffic public areas, supported by a budget of £2 million. This initiative is expected to improve survival rates from sudden cardiac arrest by offering faster access to defibrillation.

- Rising Awareness and Training Programs Training programs for AED usage have expanded significantly in 2024, supported by both government and non-governmental organizations. Over 500,000 individuals in Europe have received CPR and AED training through certified courses in 2023 alone, leading to a better-prepared public capable of handling cardiac emergencies. The European Resuscitation Council has worked closely with national health bodies to implement mandatory AED training in workplaces with over 50 employees, improving emergency preparedness across industries.

Challenges

- High Maintenance Costs The high cost of AED maintenance, including regular software updates and battery replacements, presents a challenge for public and private institutions. It is estimated that around many AEDs in Europe require servicing, with the average maintenance cost per device reaching $1,200 annually. These costs can be burdensome for smaller businesses or rural healthcare facilities, leading to underutilization or removal of AEDs from service due to budget constraints.

- Lack of Standardization in Public AED Programs Despite government regulations, the standardization of AED placement and training remains inconsistent across European countries. In 2023, data indicated that European countries have mandatory regulations for AED installation in high-risk areas, such as sports facilities and public transport hubs. This lack of standardization creates gaps in coverage and preparedness, especially in rural and low-income regions, where AED accessibility remains limited.

Government Initiatives

- EU Directive on AEDs in Public Spaces In 2023, the European Union passed a directive requiring the installation of AEDs in all public transport hubs, shopping malls, and sports facilities across member states. This directive is expected to result in the deployment of over 50,000 new AED units across Europe by 2025. The directive is part of a broader public health initiative aimed at improving response times to sudden cardiac arrest, particularly in high-traffic areas.

- French Rural Healthcare Program In 2024, the French government launched a $12 million initiative aimed at improving AED accessibility in rural healthcare facilities. The program aims to deploy 5,000 AEDs in remote regions where access to emergency medical services is limited. This initiative is expected to reduce response times and improve survival rates in areas where residents often have to travel long distances to reach a hospital.

- UK AED Education and Training Campaign The UK government, in collaboration with the British Heart Foundation, launched a national campaign in 2023 to increase awareness and training on AED usage. The campaign, backed by £5 million in funding, aims to educate 500,000 citizens by 2025 through free CPR and AED courses in community centers and schools. The initiative is designed to ensure that more individuals are equipped to respond to cardiac emergencies, especially in high-density urban areas.

- German Federal Grant for AED Integration In 2023, the German government announced a $20 million federal grant aimed at integrating AEDs into all healthcare facilities, including outpatient clinics and rehabilitation centers. The grant aims to ensure that all medical facilities are equipped with AEDs by 2025, reducing the dependency on emergency medical services during cardiac incidents. This initiative will also include annual training for healthcare professionals to maintain AED usage proficiency.

Europe Automated External Defibrillator (AED) Market Future Outlook

The Europe AED market is projected to grow exponentially, driven by further integration of AEDs in public settings and the adoption of wireless monitoring features. The expansion of telemedicine, combined with real-time feedback devices, will also shape the market’s future. Government initiatives targeting increased AED access in rural areas and educational campaigns for lay responders will play a crucial role in the market's growth over the next five years.

Future Trends

- Expansion of AED Installations in Rural Areas Governments across Europe will focus on improving AED accessibility in rural areas where healthcare facilities are scarce. It is estimated that over many new AED units will be installed in rural regions across France, Germany, and Italy. This initiative is expected to enhance emergency response times and reduce fatalities from sudden cardiac arrest in underserved areas.

- Integration of AEDs with Telemedicine The integration of AEDs with telemedicine platforms will be a key trend shaping the future of the market. AEDs in public spaces will be linked to emergency services through telemedicine platforms, enabling real-time monitoring and faster emergency dispatch. This technology will help bridge the gap between first responders and healthcare professionals, ensuring more efficient use of AEDs in critical situations.

Scope of the Report

|

By Product Type |

Fully Automatic AEDs Semi-Automatic AEDs |

|

By End User |

Hospitals Public Access Settings Workplaces |

|

By Region |

Germany France United Kingdom Sweden Italy Rest of Europe |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Healthcare Providers

Government Institutions

Emergency Medical Services (Municipal Governments

Fire and Police Departments)

Public Safety Organizations

Airports and Transportation Hubs

Corporate Wellness Programs

Schools and Universities

Sports Facilities

Municipal Governments

Fire and Police Departments

Insurance Companies

National Health Services

Investors and VC Firms

Banking and Financial Institutions

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Philips Healthcare

ZOLL Medical Corporation

Cardiac Science

Nihon Kohden

Schiller AG

Defibtech

Physio-Control

HeartSine Technologies

Laerdal Medical

Progetti Medical

Bexen Cardio

CU Medical Systems

Corpuls

MS Westfalia GmbH

Mediana

Table of Contents

1. Europe Automated External Defibrillator (AED) Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Europe Automated External Defibrillator (AED) Market Size (in USD Mn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Europe Automated External Defibrillator (AED) Market Analysis

3.1. Growth Drivers

3.1.1. Increased Incidence of Cardiovascular Diseases

3.1.2. Government Investments in Public Health Infrastructure

3.1.3. Rising Awareness and Training Programs

3.1.4. Innovation in AED Technology

3.2. Restraints

3.2.1. High Maintenance Costs

3.2.2. Lack of Standardization in Public AED Programs

3.2.3. Limited Awareness in Certain Regions

3.3. Opportunities

3.3.1. Government Initiatives to Improve AED Accessibility

3.3.2. Expansion of AED Usage in Rural Areas

3.3.3. Increasing Focus on AED Integration with Telemedicine

3.4. Trends

3.4.1. Adoption of AI-Integrated AEDs

3.4.2. Real-Time AED Feedback Systems

3.4.3. Expansion of Public AED Installations

3.5. Government Regulation

3.5.1. EU Directive on AED Installations

3.5.2. National Health Initiatives for AED Deployment

3.5.3. Public-Private Partnerships in Healthcare

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competition Ecosystem

4. Europe Automated External Defibrillator (AED) Market Segmentation, 2023

4.1. By Product Type (in Value)

4.1.1. Fully Automatic AEDs

4.1.2. Semi-Automatic AEDs

4.2. By End-User (in Value)

4.2.1. Hospitals

4.2.2. Public Access Settings

4.2.3. Workplaces

4.3. By Region (in Value)

4.3.1. North Europe

4.3.2. South Europe

4.3.3. East Europe

4.3.4. West Europe

5. Europe Automated External Defibrillator (AED) Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. Philips Healthcare

5.1.2. ZOLL Medical Corporation

5.1.3. Cardiac Science

5.1.4. Nihon Kohden

5.1.5. Schiller AG

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. Europe Automated External Defibrillator (AED) Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Public-Private Partnerships

6.4.2. Government Grants and Incentives

6.4.3. Corporate Investments in AED Technology

7. Europe Automated External Defibrillator (AED) Market Regulatory Framework

7.1. AED Placement and Usage Regulations

7.2. Compliance and Certification Requirements

7.3. Training Standards for AED Users

8. Europe Automated External Defibrillator (AED) Future Market Size (in USD Mn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. Europe Automated External Defibrillator (AED) Future Market Segmentation, 2028

9.1. By Product Type (in Value)

9.2. By End-User (in Value)

9.3. By Region (in Value)

10. Europe Automated External Defibrillator (AED) Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step:1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step:2 Market Building:

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Europe Automated External Defibrillator (AED) industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step:3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different Europe Automated External Defibrillator (AED) companies to validate statistics and seek operational and financial information from company representatives.

Step:4 Research output:

Our team will approach multiple construction companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such Automated External Defibrillator (AED) Market companies.

Frequently Asked Questions

01 How big is Europe Automated External Defibrillator (AED) Market?

The Europe Automated External Defibrillator (AED) Market market, valued at USD 350 million in 2023, is driven by government initiatives, the growing prevalence of cardiovascular diseases, and advancements in AED technology.

02 What are the challenges in Europe Automated External Defibrillator (AED) Market?

Challenges in the Europe Automated External Defibrillator (AED) Market include high maintenance costs, inconsistent AED standardization across countries, limited awareness in certain regions, and regulatory compliance issues affecting businesses and public institutions.

03 Who are the major players in the Europe Automated External Defibrillator (AED) Market?

Key players in the Europe Automated External Defibrillator (AED) Market include Philips Healthcare, ZOLL Medical Corporation, Cardiac Science, Nihon Kohden, and Schiller AG, who dominate the market due to strong R&D capabilities and extensive distribution networks.

04 What are the growth drivers of Europe Automated External Defibrillator (AED) Market?

The Europe Automated External Defibrillator (AED) Market is driven by increased incidence of cardiovascular diseases, government investments in public health infrastructure, growing awareness through training programs, and technological innovations in AED devices.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.