Global Liquefied Petroleum Gas (LPG) Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD11292

November 2024

91

About the Report

Global Liquefied Petroleum Gas (LPG) Market Overview

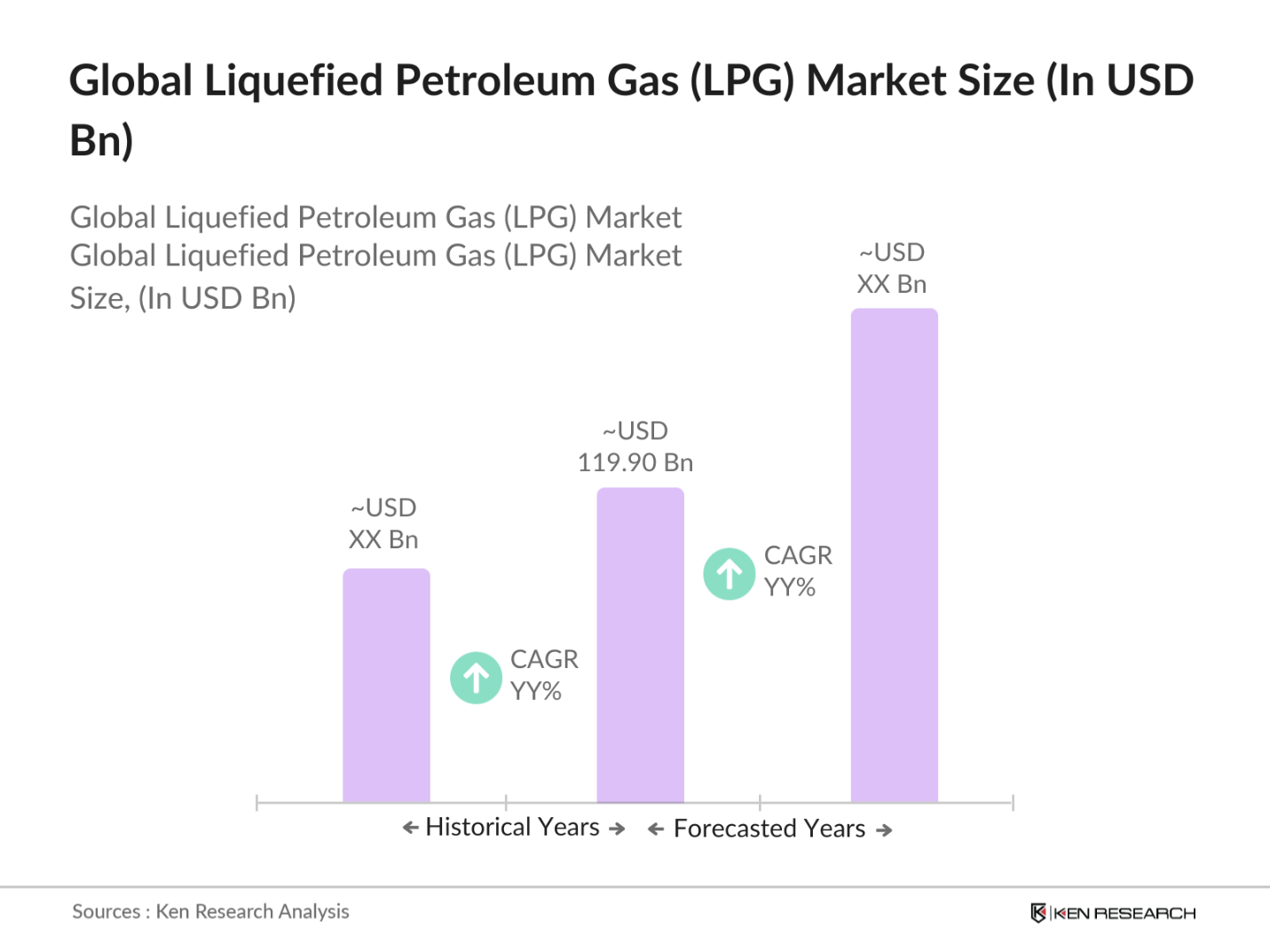

- The global Liquefied Petroleum Gas (LPG) market is valued at USD 119.90billion, driven primarily by the increasing demand for cleaner energy sources. LPG's versatility as a fuel for heating, cooking, and industrial processes, along with its relatively lower carbon emissions compared to traditional fossil fuels, has propelled its adoption across various sectors. Rising urbanization, especially in developing regions, and government initiatives to promote clean energy, have significantly contributed to the market's expansion.

- Asia-Pacific dominates the LPG market, primarily due to rapid urbanization and industrialization in countries such as China, India, and Japan. The regions growing population, along with government subsidies and the push toward replacing traditional solid fuels with LPG in rural areas, has bolstered the market's dominance. Additionally, the strong presence of petrochemical industries in the region, which use LPG as a feedstock for plastics production, further cements Asia-Pacifics leadership in the market.

- Brazil has implemented a national LPG subsidy program that focuses on making LPG affordable and accessible to low-income families. Under this program, the government provides financial assistance to eligible households, enabling them to purchase LPG cylinders at reduced rates. By 2023, this initiative had reached over 14 million Brazilian households, significantly increasing LPG penetration in rural and underserved areas. The program is part of Brazils broader efforts to transition away from traditional fuels, such as firewood and charcoal, improving public health and reducing deforestation.

Global Liquefied Petroleum Gas (LPG) Market Segmentation

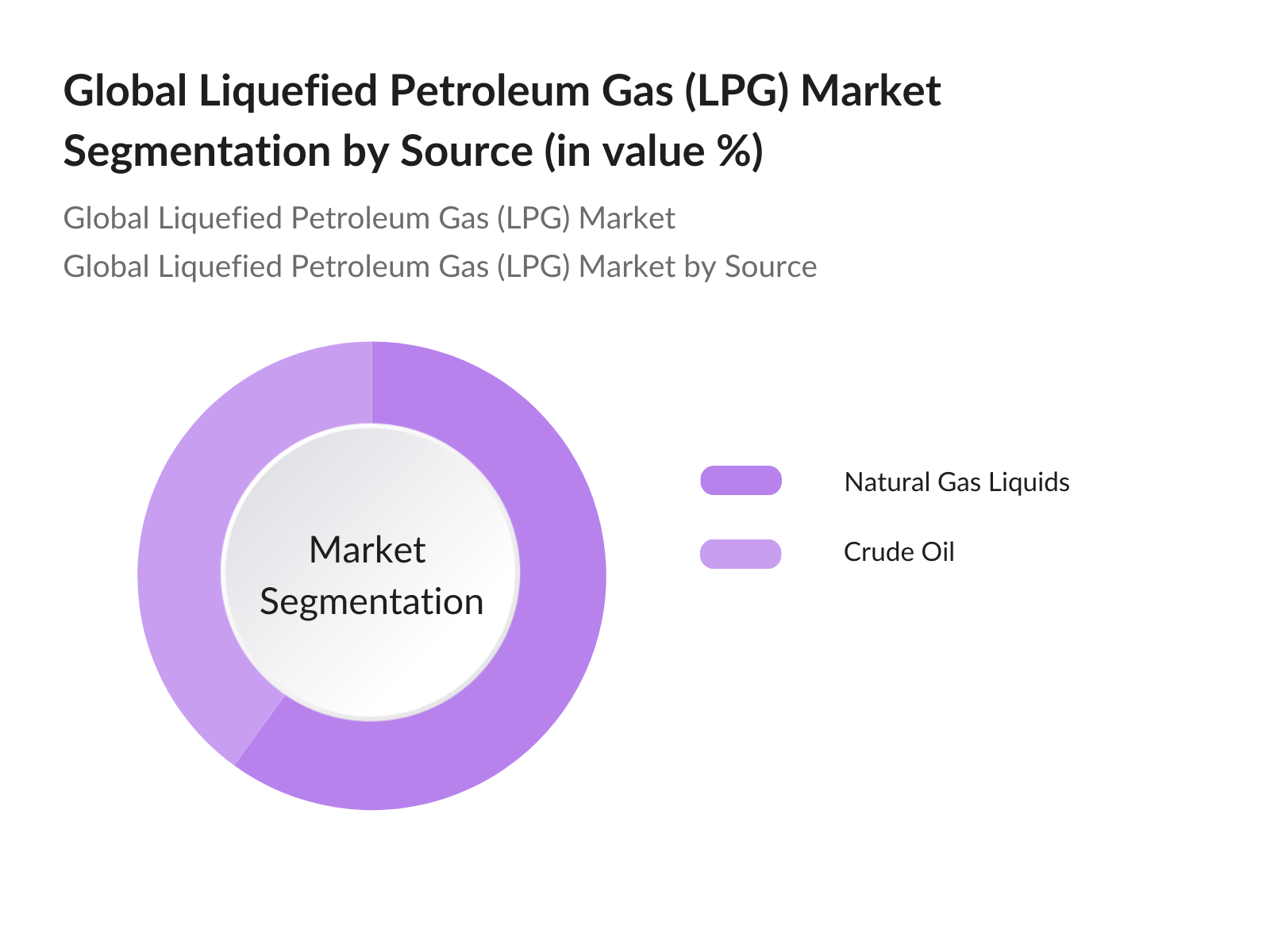

By Source: The LPG market is segmented by source into Crude Oil and Natural Gas Liquids (NGL). NGL holds a dominant market share due to the lower cost of extraction compared to crude oil processing. NGLs are primarily produced during natural gas processing, making them a more efficient source of LPG. As natural gas production increases globally, especially in regions like North America and the Middle East, the supply of NGL-derived LPG has expanded, leading to its dominance in the market.

By Region: The LPG market is geographically segmented into Asia-Pacific, North America, Europe, South America, and Middle East & Africa. Asia-Pacific dominates the market due to the region's growing population, rapid urbanization, and significant government support for cleaner energy alternatives like LPG. The region also benefits from a well-developed distribution infrastructure, making LPG accessible even in remote areas.

Global Liquefied Petroleum Gas (LPG) Market Competitive Landscape

The LPG market is dominated by both global energy giants and regional players, each leveraging their extensive distribution networks and technological advancements to maintain a stronghold in the market. Key companies such as BP Plc, Exxon Mobil, Saudi Aramco, and Reliance Industries hold a significant share of the market due to their diversified operations and strategic initiatives. This consolidation highlights the dominant influence these major players exert in the global market.

|

Company |

Establishment Year |

Headquarters |

Market Revenue |

LPG Production |

Strategic Partnerships |

Geographical Presence |

R&D Investments |

Technological Innovation |

|

BP Plc |

1908 |

London, UK |

High |

|||||

|

Exxon Mobil Corporation |

1999 |

Texas, USA |

High |

|||||

|

Saudi Aramco |

1933 |

Dhahran, Saudi Arabia |

High |

|||||

|

Reliance Industries Ltd. |

1973 |

Mumbai, India |

High |

|||||

|

Sinopec (China Petroleum) |

2000 |

Beijing, China |

High |

Global Liquefied Petroleum Gas (LPG) Market Analysis

Market Growth Drivers:

- Shift to Cleaner Fuels: The global transition towards cleaner energy sources, particularly in developing nations, is a significant driver for the LPG market. As of 2022, approximately 2.8 billion people worldwide still rely on solid fuels like wood and coal for cooking, leading to severe indoor air pollution. Governments, especially in countries like India and Indonesia, are actively promoting LPG as a cleaner alternative. For instance, Indias Pradhan Mantri Ujjwala Yojana program has provided over 95 million households with subsidized LPG connections to reduce reliance on polluting solid fuels and improve public health.

- Expanding Urbanization: Rapid urbanization is fueling the demand for LPG in emerging markets. By 2025, India is projected to add 500 million new urban residents, further boosting the demand for energy sources like LPG in residential and commercial sectors. Urban areas typically lack access to traditional fuels like biomass, making LPG a convenient and efficient energy option. Countries across Africa and Southeast Asia are also experiencing similar trends, where rising urban populations have increased the need for cleaner, more reliable cooking and heating fuels such as LPG.

- Supporting LPG Adoption: Many governments are implementing policies and initiatives to support the transition to cleaner fuels like LPG, driving market growth. In countries such as Brazil and Nigeria, government subsidies and incentives have made LPG more affordable and accessible for lower-income households. Brazils national LPG subsidy program, for instance, has increased LPG penetration in rural and low-income areas, reducing reliance on hazardous solid fuels. Similarly, in Nigeria, the governments National LPG Expansion Plan aims to increase domestic LPG consumption to over 5 million metric tons annually, supporting the shift to cleaner energy sources.

Market Challenges:

- Infrastructure Constraints in Developing Regions: Infrastructure constraints significantly hinder LPG market growth, particularly in developing countries where the distribution network for LPG is underdeveloped. In sub-Saharan Africa, many rural areas lack the necessary infrastructure, such as pipelines and storage facilities, to ensure a steady supply of LPG. According to the International Energy Agency (IEA), a vast number of households in the region do not have access to LPG due to insufficient supply chain development. This situation impedes the transition to cleaner fuels and forces households to continue relying on traditional fuels, posing health risks and environmental challenges.

- Storage and Distribution Bottlenecks: The lack of sufficient LPG storage and distribution infrastructure remains a critical issue globally. In many parts of Asia and Latin America, while demand for LPG is rising, storage facilities are unable to keep pace, causing bottlenecks in supply. In countries like Bangladesh and Peru, existing storage infrastructure is outdated or too small to meet the growing demand, which often results in supply shortages during peak usage times. This inadequacy in the storage infrastructure affects both the supply chain's reliability and the market's ability to scale up and meet future demand.

Global Liquefied Petroleum Gas (LPG) Market Future Outlook

The LPG market is expected to show consistent growth over the next five years, driven by expanding applications across residential, industrial, and transport sectors. The global shift toward cleaner energy alternatives, combined with technological advancements in LPG production and distribution, will continue to fuel demand. Governments across the world are also likely to further incentivize LPG adoption, particularly in regions where pollution control and energy accessibility are critical concerns.

Market Opportunities:

- Technological Advancements in LPG Refining and Separation: New technological advancements in LPG production, specifically in refining and gas separation techniques, are boosting supply efficiency and reducing environmental impact. Countries like Saudi Arabia are leading the charge by developing state-of-the-art refining processes that improve the separation of LPG from natural gas and crude oil. In 2023, Saudi Arabia introduced refining technologies that have increased its LPG production capacity by 2.5 million metric tons annually. These innovations not only enhance output but also reduce emissions, making the production process more sustainable and cost-effective.

- Digitalization in LPG Supply Chain and Distribution Management: Digitalization of the LPG supply chain is a growing trend, with companies leveraging smart technologies to optimize logistics, distribution, and inventory management. Sensors and IoT-enabled devices are increasingly being integrated into LPG storage and distribution networks to monitor gas levels, streamline delivery routes, and predict demand more accurately. In Southeast Asia, digital platforms are now used by distributors to manage the LPG supply chain, reducing inefficiencies and improving customer satisfaction. These innovations are crucial in ensuring timely deliveries and minimizing the risks of shortages, especially in high-demand regions.

Scope of the Report

|

By Source |

Crude Oil Natural Gas Liquids |

|

By Application |

Residential Industrial Commercial Transport Others |

|

By Distribution |

Retail Institutional |

|

By End-User |

Petrochemical Chemical Agriculture Automotive Commercial Heating |

|

By Region |

APAC North America Europe South America Middle East & Africa |

Products

Key Target Audience

LPG Distributors

LPG Cylinder Manufacturers

Residential and Commercial Fuel Suppliers

Automotive Industry Stakeholders

Industrial Heating Solution Providers

Petrochemical Manufacturers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., U.S. Environmental Protection Agency, India's Ministry of Petroleum and Natural Gas)

Companies

Players Mention in the Report

BP Plc

Exxon Mobil Corporation

Chevron Corporation

Saudi Aramco

Reliance Industries Ltd.

China Petroleum & Chemical Corporation (Sinopec)

SHV Energy

Indian Oil Corporation Ltd.

TotalEnergies SE

Valero Energy Corporation

Repsol S.A.

Kuwait Petroleum Corporation

Bharat Petroleum Corporation Ltd.

OQ SAOC

Idemitsu Kosan Co. Ltd.

Table of Contents

01. Global LPG Market

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Industry Overview and Market Trends

1.4. Key Insights and Strategic Analysis

02. Global LPG Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth (In Volume and Value)

2.3. Demand Forecast & Key Market Developments

03. Global LPG Market Dynamics

3.1. Growth Drivers (e.g., Shift to Cleaner Fuels, Expanding Urbanization)

3.2. Market Challenges (e.g., Infrastructure Constraints, Volatile Pricing)

3.3. Opportunities (e.g., Autogas Adoption, Marine Fuel Applications)

3.4. Trends (e.g., Virtual Pipeline Technology, Technological Advancements in Production)

3.5. Supply Chain Analysis (Processing, Refining, and Distribution)

3.6. Porter's Five Forces Analysis (Bargaining Power of Suppliers, Competitive Rivalry)

04. Global LPG Market Segmentation

4.1. By Source (Crude Oil, Natural Gas Liquids)

4.2. By Application (Residential, Industrial, Commercial, Petrochemical, Transport, Others)

4.3. By Region (APAC, North America, Europe, South America, Middle East & Africa)

4.4. By Distribution Channel (Retail, Institutional)

05. Global LPG Market Competitive Landscape

5.1. Profiles of Major Companies (In-depth analysis including financials, market position, etc.)

5.1.1. BP Plc

5.1.2. Exxon Mobil Corporation

5.1.3. Chevron Corporation

5.1.4. Saudi Aramco

5.1.5. Reliance Industries Ltd.

5.1.6. China Petroleum & Chemical Corporation (Sinopec)

5.1.7. SHV Energy

5.1.8. Indian Oil Corporation Ltd.

5.1.9. TotalEnergies SE

5.1.10. Valero Energy Corporation

5.1.11. Repsol S.A.

5.1.12. Kuwait Petroleum Corporation

5.1.13. Bharat Petroleum Corporation Ltd.

5.1.14. OQ SAOC

5.1.15. Idemitsu Kosan Co. Ltd.

5.2. Market Share Analysis (Market Share by Segment and Region)

5.3. Strategic Initiatives (Mergers, Acquisitions, Collaborations, and Joint Ventures)

5.4. Investment and Funding Analysis

06. Cross Comparison Parameters

6.1. No. of Employees

6.2. Market Revenue (Value)

6.3. Market Share (Volume)

6.4. Geographical Presence (By Region)

6.5. Technological Innovations (In Production and Distribution)

6.6. Strategic Partnerships (Mergers & Collaborations)

6.7. R&D Expenditure

6.8. Product Portfolio and Expansion

07. Global LPG Regulatory Framework

7.1. Global Emission Standards

7.2. Environmental Regulations (Government Support for Clean Fuels)

7.3. LPG Safety Standards (Transportation and Storage)

08. Global LPG Future Market Size

8.1. Future Market Projections (In USD and Volume)

8.2. Key Factors Driving Future Growth

09. Global LPG Future Market Segmentation

9.1. By Source

9.2. By Application

9.3. By Region

10. Global LPG Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Market Entry Strategies

10.3. Potential White Space Opportunities

10.4. Marketing Initiatives for Target Sectors

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This phase focuses on mapping key variables within the LPG market. Extensive desk research from proprietary databases is conducted to identify significant market drivers, stakeholders, and competitive dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data on LPG production, distribution, and consumption is compiled. The data is analyzed to identify market penetration trends and performance of key sub-segments.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses are developed and validated through direct interviews with industry experts. These consultations provide insights into operational dynamics and the financial performance of LPG suppliers.

Step 4: Research Synthesis and Final Output

The final phase includes the synthesis of all gathered data into actionable insights. Market forecasts and segmentation are validated through primary research, ensuring a comprehensive analysis of the LPG market.

Frequently Asked Questions

01. How big is the global LPG market?

The global LPG market is valued at USD 119.90 billion, driven by rising demand for cleaner fuels and increasing industrial applications(

02. What are the challenges in the global LPG market?

Challenges include volatile pricing, infrastructure constraints, and the need for significant investments in distribution systems, particularly in remote areas

03. Who are the major players in the LPG market?

Key players in the LPG market include BP Plc, Exxon Mobil Corporation, Saudi Aramco, Reliance Industries Ltd., and Sinopec, each with extensive operations globally

04. What drives the growth of the global LPG market?

The market is driven by a combination of factors, including the global shift toward cleaner energy sources, technological advancements in LPG production, and government incentives to replace traditional fuels

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.