Global OSS and BSS Market Outlook to 2030

Region:Global

Author(s):Vijay Kumar

Product Code:KROD1556

November 2024

98

About the Report

Global OSS and BSS Market Overview

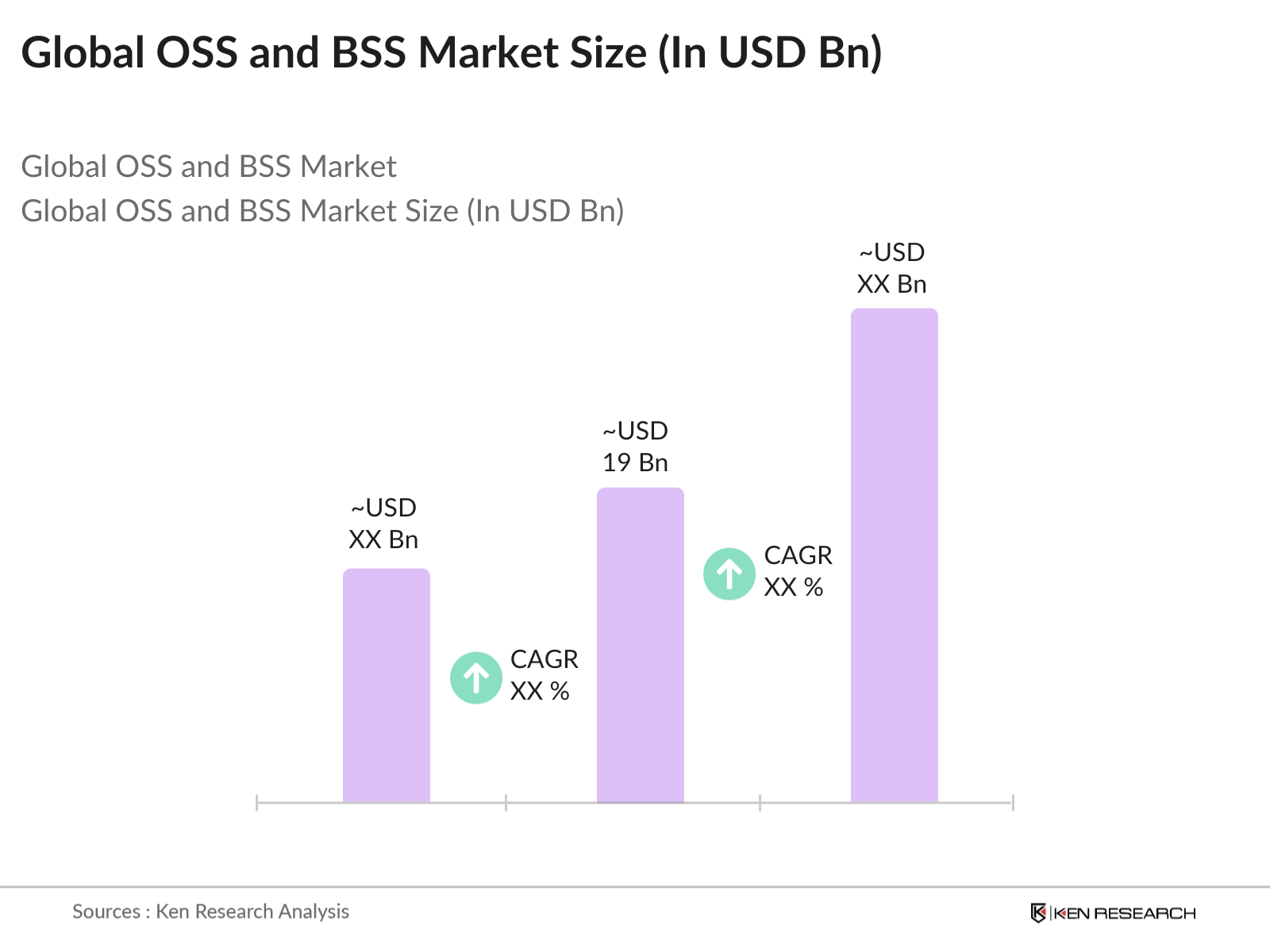

- The global Operations Support Systems (OSS) and Business Support Systems (BSS) market is valued at USD 19 billion, based on a five-year historical analysis. This substantial valuation is driven by the rapid expansion of the telecommunications sector, the increasing adoption of 5G technology, and the growing demand for real-time billing and customer management solutions. The integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) into OSS/BSS platforms has further propelled market growth.

- North America and Europe dominate the OSS and BSS market due to their advanced telecommunications infrastructure and early adoption of cutting-edge technologies. The presence of major telecommunications companies and continuous investments in network modernization contribute to their market leadership. Additionally, the Asia-Pacific region is experiencing significant growth, driven by the rapid expansion of mobile networks and increasing demand for customer-centric services.

- Telecom operators must adhere to international standards to ensure interoperability and service quality. The European Telecommunications Standards Institute (ETSI) plays a pivotal role in developing globally applicable standards. In 2023, ETSI released the first report on Reconfigurable Intelligent Surfaces communication and channel models, highlighting the ongoing evolution of telecom standards.

Global OSS and BSS Market Segmentation

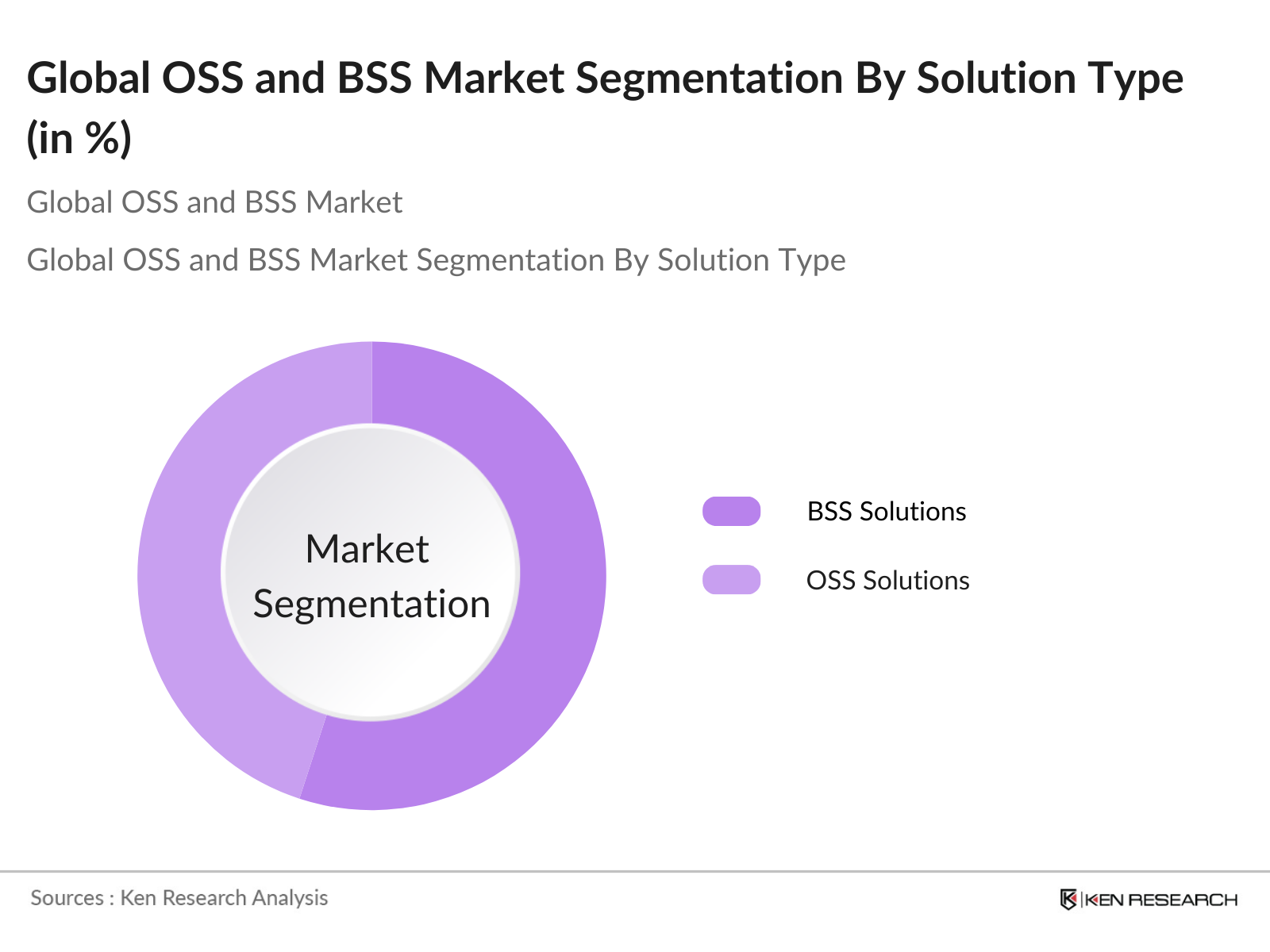

By Solution Type: The market is segmented by solution type into OSS solutions and BSS solutions. Recently, BSS solutions have a dominant market share under this segmentation. This dominance is attributed to the critical role BSS solutions play in billing, revenue management, and customer relationship management, which are essential for telecommunications companies to maintain profitability and customer satisfaction.

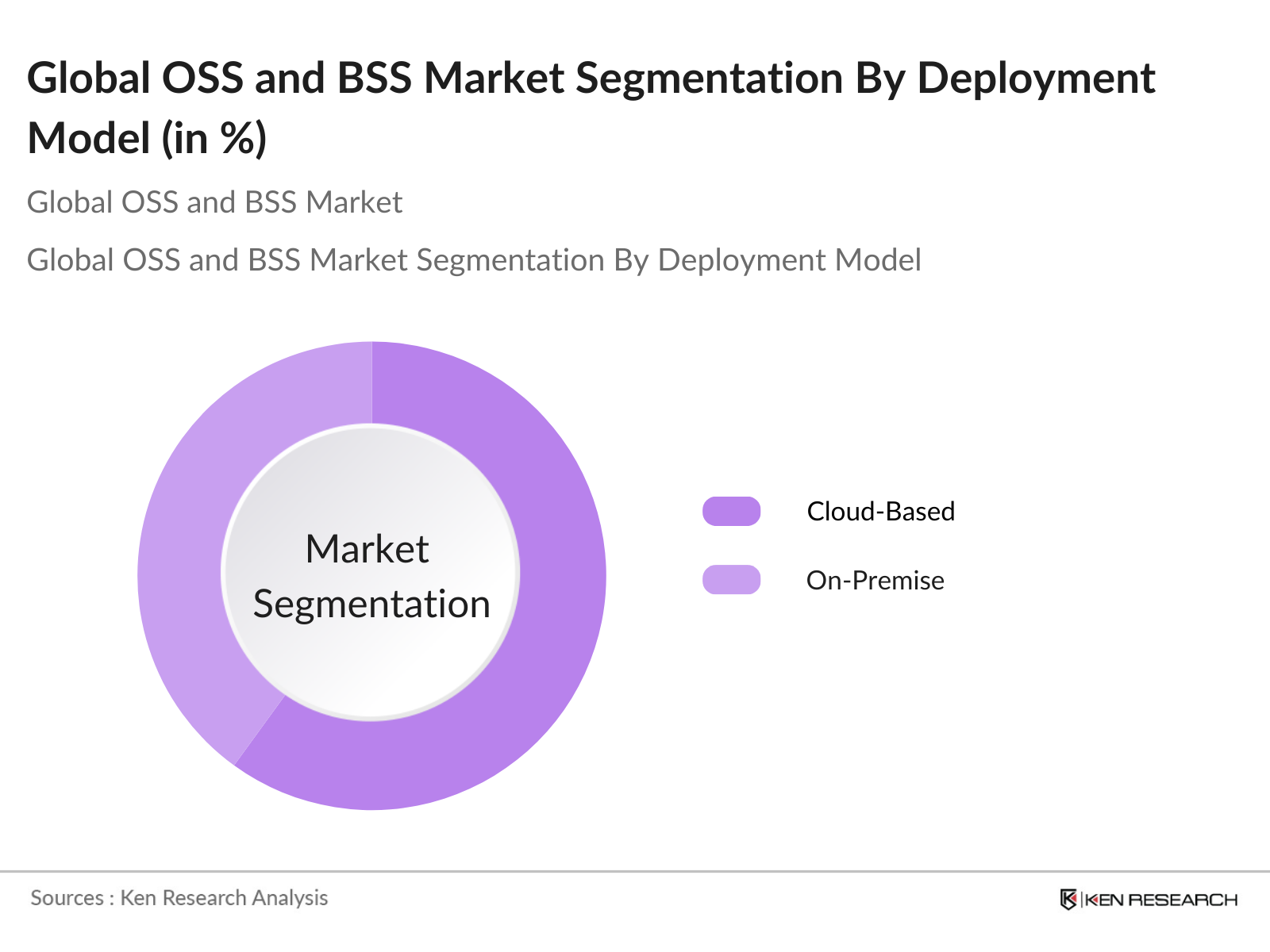

By Deployment Model: The market is segmented by deployment model into on-premise and cloud-based solutions. Cloud-based solutions are increasingly dominating the market share in this segment. This shift is driven by the flexibility, scalability, and cost-effectiveness that cloud deployments offer, enabling service providers to quickly adapt to changing market demands and reduce operational expenses.

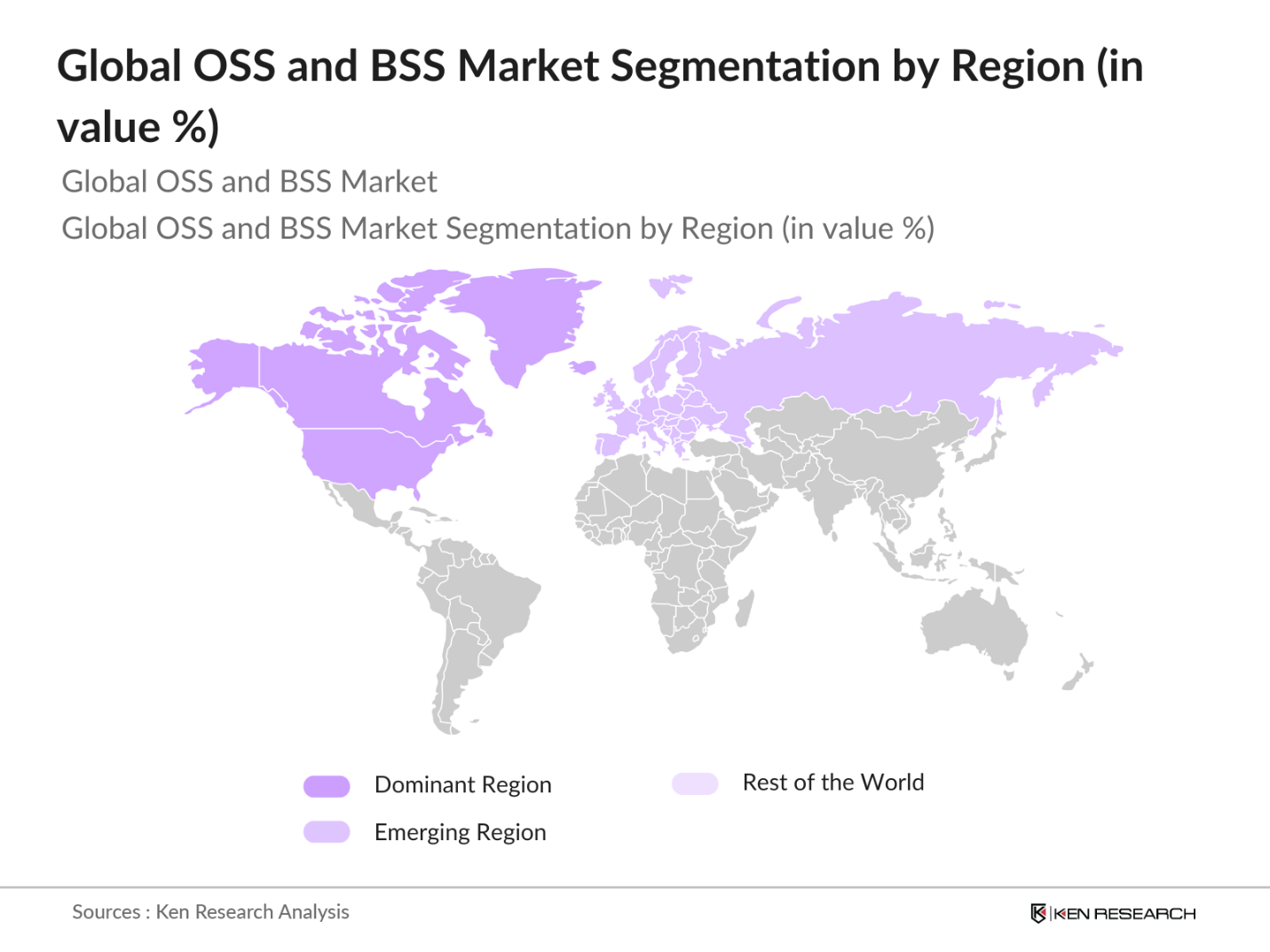

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. North America holds a dominant market share in this segmentation. This is due to the region's advanced telecommunications infrastructure, high adoption rate of new technologies, and significant investments in network modernization and customer experience enhancement.

Global OSS and BSS Market Competitive Landscape

The global OSS and BSS market is characterized by the presence of several key players who contribute significantly to market dynamics. These companies are engaged in continuous innovation, strategic partnerships, and mergers and acquisitions to strengthen their market positions.

Global OSS and BSS Industry Analysis

Growth Drivers

- Digital Transformation Initiatives: The global push towards digital transformation has significantly impacted the OSS (Operations Support Systems) and BSS (Business Support Systems) market. In 2023, the International Telecommunication Union (ITU) reported that over 5.3 billion people were using the internet, highlighting the increasing digital engagement worldwide. This surge necessitates advanced OSS/BSS solutions to manage complex networks and services. Additionally, the World Bank's 2023 data indicates that global mobile cellular subscriptions reached approximately 8.6 billion, underscoring the demand for efficient telecom infrastructure.

- Adoption of 5G Networks: The deployment of 5G networks is a significant driver for the OSS/BSS market. According to the Global Mobile Suppliers Association (GSA), as of June 2023, 176 operators in 72 countries had launched commercial 5G services. The GSMA forecasts that by 2025, 5G networks will cover one-third of the world's population, necessitating sophisticated OSS/BSS solutions to manage the increased network complexity and service diversity. This widespread adoption underscores the need for advanced systems to handle the intricacies of 5G technology.

- Demand for Real-Time Billing and Revenue Management: The telecommunications industry's shift towards real-time services has heightened the need for immediate billing and revenue management. A 2023 report by the International Telecommunication Union (ITU) highlighted that 60% of telecom operators have integrated real-time billing systems to enhance customer experience and operational efficiency. This trend reflects the industry's commitment to providing transparent and prompt billing processes, which are essential for maintaining customer trust and satisfaction.

Market Challenges

- Legacy System Integration: Integrating new OSS/BSS solutions with existing legacy systems presents a significant challenge. A 2023 survey by the TM Forum revealed that 65% of telecom operators identified legacy system integration as a major obstacle to digital transformation. These outdated systems often lack the flexibility to adapt to modern technologies, leading to increased operational costs and inefficiencies.

- Data Security and Privacy Concerns: The increasing digitization of services has raised concerns about data security and privacy. The International Telecommunication Union (ITU) reported in 2023 that cyber threats in the telecom sector had risen by 35% compared to the previous year. This surge underscores the need for robust security measures within OSS/BSS solutions to protect sensitive customer information and maintain regulatory compliance.

Global OSS and BSS Market Future Outlook

Over the next five years, the global OSS and BSS market is expected to experience significant growth, driven by continuous advancements in telecommunications technology, the proliferation of 5G networks, and the increasing demand for enhanced customer experience management. The integration of AI and ML into OSS/BSS platforms is anticipated to further optimize network operations and customer interactions. Additionally, the shift towards cloud-based solutions is likely to continue, offering scalability and flexibility to service providers.

Market Opportunities

- Cloud-Based OSS/BSS Solutions: The shift towards cloud computing offers significant opportunities for the OSS/BSS market. The International Data Corporation (IDC) reported that in 2023, 70% of telecom operators had adopted cloud-based OSS/BSS solutions to enhance scalability and reduce operational costs. This trend reflects the industry's move towards more flexible and efficient systems.

- Expansion in Emerging Markets: Emerging markets present substantial growth opportunities for OSS/BSS providers. The World Bank's 2023 data shows that mobile penetration in Sub-Saharan Africa reached 46%, indicating significant room for growth. As telecom infrastructure expands in these regions, the demand for advanced OSS/BSS solutions is expected to rise, facilitating better service delivery and customer management.

Scope of the Report

|

Solution Type |

OSS Solutions |

|

Deployment Model |

On-Premise |

|

Organization Size |

Small and Medium Enterprises (SMEs) |

|

End-User Industry |

IT and Telecommunications |

|

Region |

North America |

Products

Key Target Audience

Telecommunications Service Providers

IT and Technology Solution Providers

Cloud Service Providers

Government and Regulatory Bodies (e.g., Federal Communications Commission)

Financial Institutions and Banks

Investments and Venture Capitalist Firms

Network Equipment Manufacturers

Customer Relationship Management (CRM) Solution Providers

Companies

Players Mentioned in the Report

Accenture PLC

Amdocs

Capgemini SE

CSG Systems International, Inc.

Hewlett Packard Enterprise Development LP

Huawei Technologies Co., Ltd.

IBM Corporation

Infosys Limited

Netcracker Technology Corporation

Nokia Corporation

Table of Contents

1. Global OSS and BSS Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global OSS and BSS Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global OSS and BSS Market Analysis

3.1. Growth Drivers

3.1.1. Digital Transformation Initiatives

3.1.2. Adoption of 5G Networks

3.1.3. Demand for Real-Time Billing and Revenue Management

3.1.4. Integration of AI and Machine Learning

3.2. Market Challenges

3.2.1. Legacy System Integration

3.2.2. Data Security and Privacy Concerns

3.2.3. High Implementation Costs

3.3. Opportunities

3.3.1. Cloud-Based OSS/BSS Solutions

3.3.2. Expansion in Emerging Markets

3.3.3. IoT and M2M Communication

3.4. Trends

3.4.1. Shift Towards Subscription-Based Models

3.4.2. Emphasis on Customer Experience Management

3.4.3. Service Orchestration and Automation

3.5. Regulatory Landscape

3.5.1. Compliance with Telecom Standards

3.5.2. Data Protection Regulations

3.5.3. Impact of Net Neutrality Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. Global OSS and BSS Market Segmentation

4.1. By Solution Type (In Value %)

4.1.1. OSS Solutions

4.1.1.1. Service Assurance

4.1.1.2. Network Management

4.1.1.3. Inventory Management

4.1.2. BSS Solutions

4.1.2.1. Billing and Revenue Management

4.1.2.2. Service Fulfillment

4.1.2.3. Customer and Product Management

4.2. By Deployment Model (In Value %)

4.2.1. On-Premise

4.2.2. Cloud-Based

4.3. By Organization Size (In Value %)

4.3.1. Small and Medium Enterprises (SMEs)

4.3.2. Large Enterprises

4.4. By End-User Industry (In Value %)

4.4.1. IT and Telecommunications

4.4.2. Banking, Financial Services, and Insurance (BFSI)

4.4.3. Media and Entertainment

4.4.4. Retail and E-Commerce

4.4.5. Others

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East and Africa

5. Global OSS and BSS Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Accenture PLC

5.1.2. Amdocs

5.1.3. Capgemini SE

5.1.4. CSG Systems International, Inc.

5.1.5. Hewlett Packard Enterprise Development LP

5.1.6. Huawei Technologies Co., Ltd.

5.1.7. IBM Corporation

5.1.8. Infosys Limited

5.1.9. Netcracker Technology Corporation

5.1.10. Nokia Corporation

5.1.11. Oracle Corporation

5.1.12. Tata Consultancy Services Limited

5.1.13. Ericsson

5.1.14. Cisco Systems, Inc.

5.1.15. Comarch SA

5.2. Cross Comparison Parameters (Revenue, Number of Employees, Headquarters, Inception Year, Market Share, Product Portfolio, Regional Presence, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6. Global OSS and BSS Market Regulatory Framework

6.1. Compliance Standards

6.2. Data Protection and Privacy Laws

6.3. Telecom Regulatory Policies

6.4. Impact of International Trade Agreements

7. Global OSS and BSS Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global OSS and BSS Future Market Segmentation

8.1. By Solution Type (In Value %)

8.2. By Deployment Model (In Value %)

8.3. By Organization Size (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9. Global OSS and BSS Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Segmentation and Cohort Analysis

9.3. Strategic Marketing Initiatives

9.4. Identification of White Space Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the global OSS and BSS market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the global OSS and BSS market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates. This comprehensive analysis provides a foundational understanding of market trends and growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

In this step, market hypotheses are developed and subsequently validated through expert interviews, including computer-assisted telephone interviews (CATIs) with industry leaders and professionals across the OSS and BSS ecosystem. These consultations yield valuable operational insights and strategic viewpoints from industry insiders, helping to refine market forecasts and corroborate gathered data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with key players and telecommunications service providers to gain detailed insights into product offerings, emerging trends, and technological advancements. This information is synthesized with data from previous steps, ensuring a comprehensive, accurate, and validated analysis of the global OSS and BSS market.

Frequently Asked Questions

1. How big is the global OSS and BSS market?

The global Operations Support Systems (OSS) and Business Support Systems (BSS) market is valued at USD 19 billion, based on a five-year historical analysis. This substantial valuation is driven by the rapid expansion of the telecommunications sector, the increasing adoption of 5G technology, and the growing demand for real-time billing and customer management solutions.

2. What are the challenges in the global OSS and BSS market?

Key challenges include integrating legacy systems, addressing cybersecurity and data privacy concerns, and managing high implementation costs, which can inhibit market expansion.

3. Who are the major players in the global OSS and BSS market?

Leading companies include Accenture, Huawei, Amdocs, Oracle, and Nokia. Their established networks and continuous technological advancements contribute to their strong market positions.

4. What are the growth drivers for the global OSS and BSS market?

Major growth drivers include the adoption of 5G, increasing demand for real-time billing, and advancements in AI-driven network operations and customer relationship management solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.