India Electric Scooter and Motorcycle Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD3680

December 2024

92

About the Report

India Electric Scooter and Motorcycle Market Overview

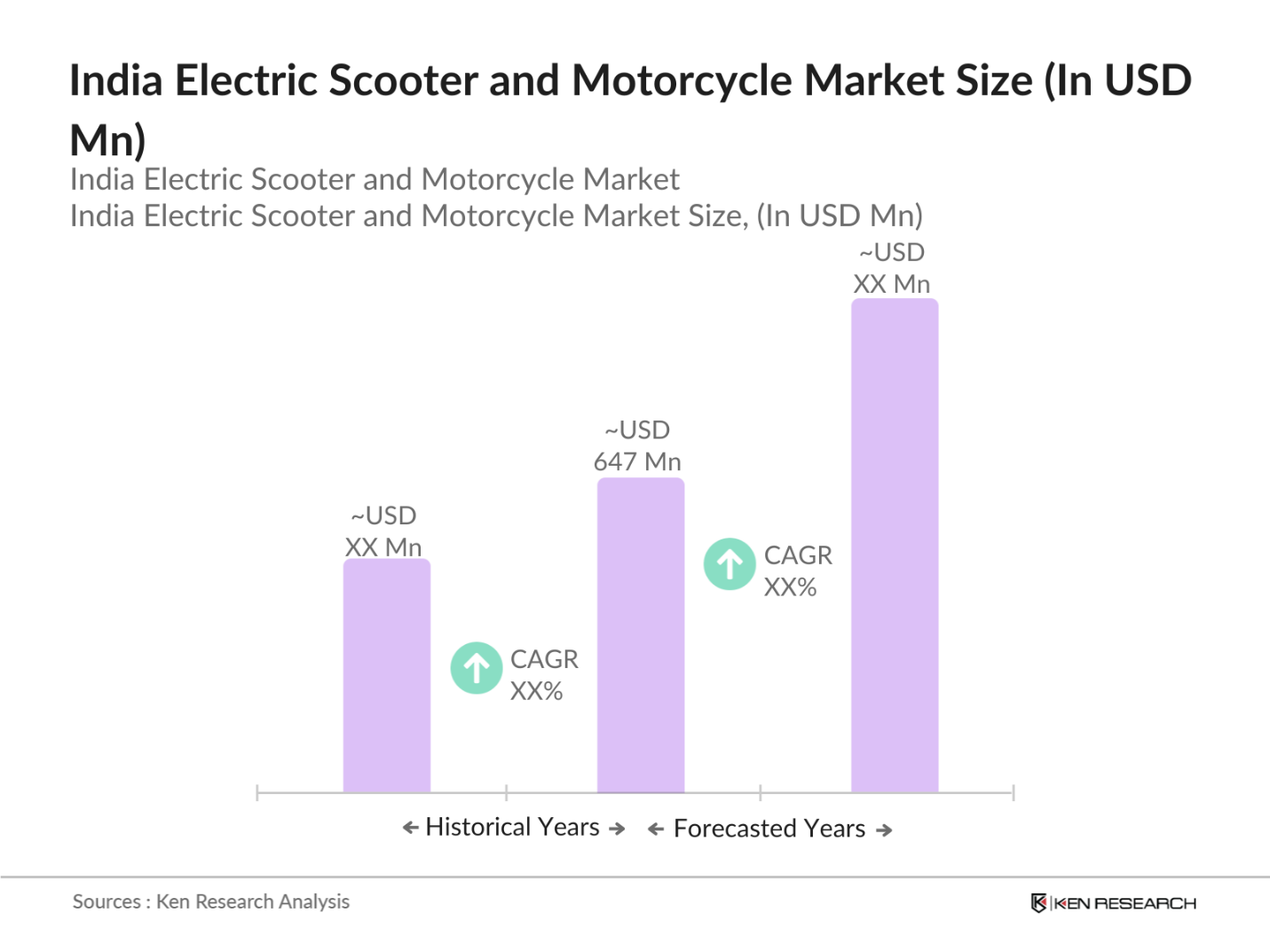

- The India Electric Scooter and Motorcycle market is valued at USD 647 million, based on a five-year historical analysis. The market is driven by a combination of factors, including rising fuel costs, increased consumer awareness about environmental sustainability, and the strong push from the Indian government for electric vehicles under schemes such as FAME II. Additionally, advancements in battery technology and infrastructure improvements, including the development of charging stations, are significantly contributing to the market's growth.

- The dominant regions in the India Electric Scooter and Motorcycle market are Maharashtra, Tamil Nadu, and Karnataka. These regions benefit from strong government policies, robust industrial infrastructure, and a high rate of urbanization. Additionally, cities like Bangalore, Pune, and Chennai are becoming hubs for electric two-wheeler manufacturers due to the presence of a skilled workforce and the availability of resources needed for EV production and assembly, making them prominent contributors to market dominance.

- The FAME initiative plays a pivotal role in regulating and promoting electric vehicle adoption in India. Launched in 2015, FAME-II significantly expanded incentives for electric vehicles, with the government allocating INR 10,000 crore towards this effort. As of 2022, the scheme has supported the sale of over 600,000 electric two-wheelers, reinforcing its effectiveness in driving market growth. The initiative aims to increase the availability of electric vehicles and develop a sustainable ecosystem, aligning with India's broader objectives of reducing carbon emissions and enhancing energy security.

India Electric Scooter and Motorcycle Market Segmentation

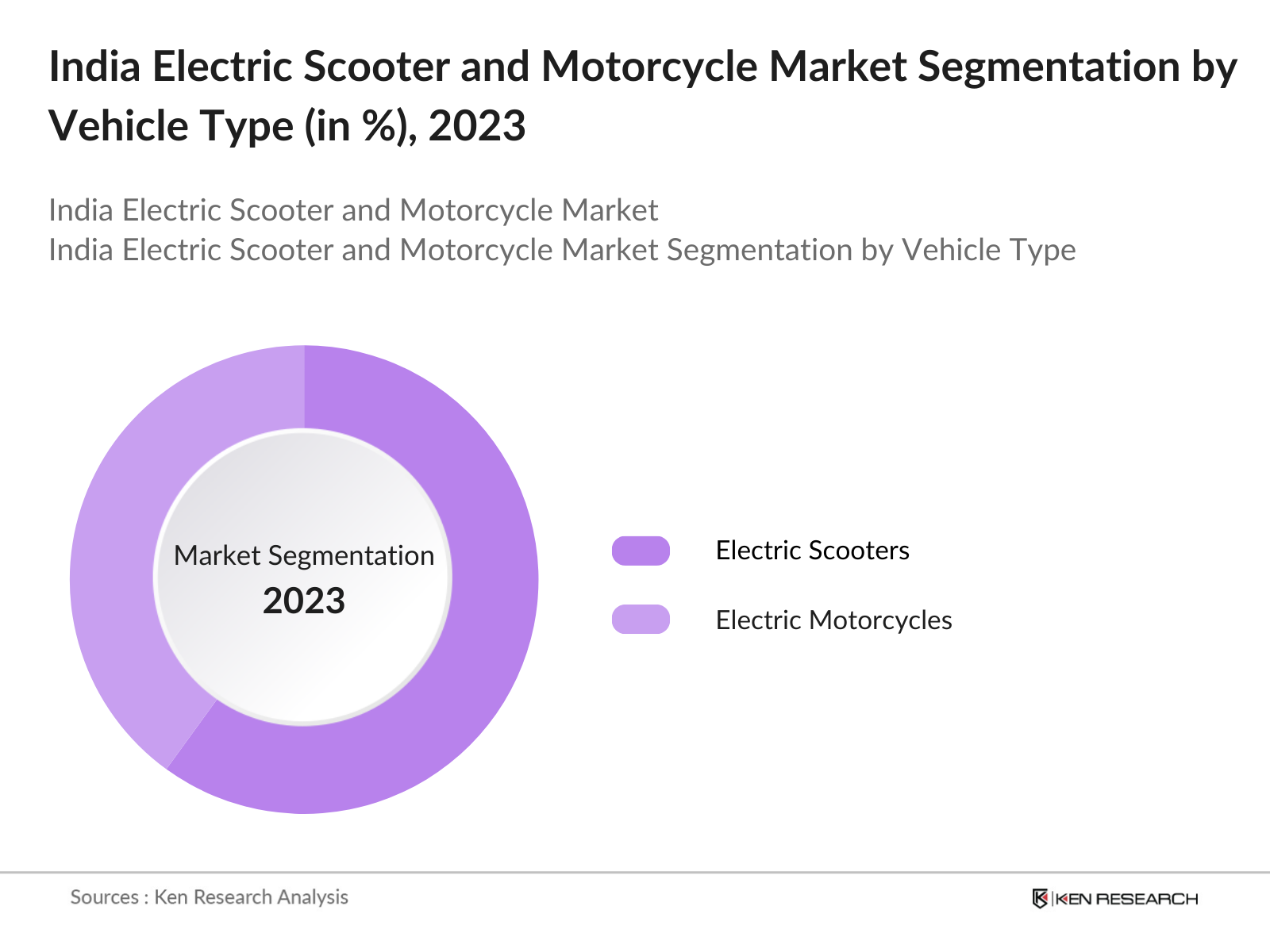

By Vehicle Type: The India Electric Scooter and Motorcycle market is segmented by vehicle type into electric scooters and electric motorcycles. Recently, electric scooters have captured a dominant share of the market, primarily due to their affordability and suitability for urban commuting. The compact size, lower maintenance costs, and ease of handling make electric scooters an attractive choice for consumers in densely populated cities. Companies such as Hero Electric and Okinawa have capitalized on this demand, offering a range of scooters with efficient battery systems, further solidifying their position in this segment.

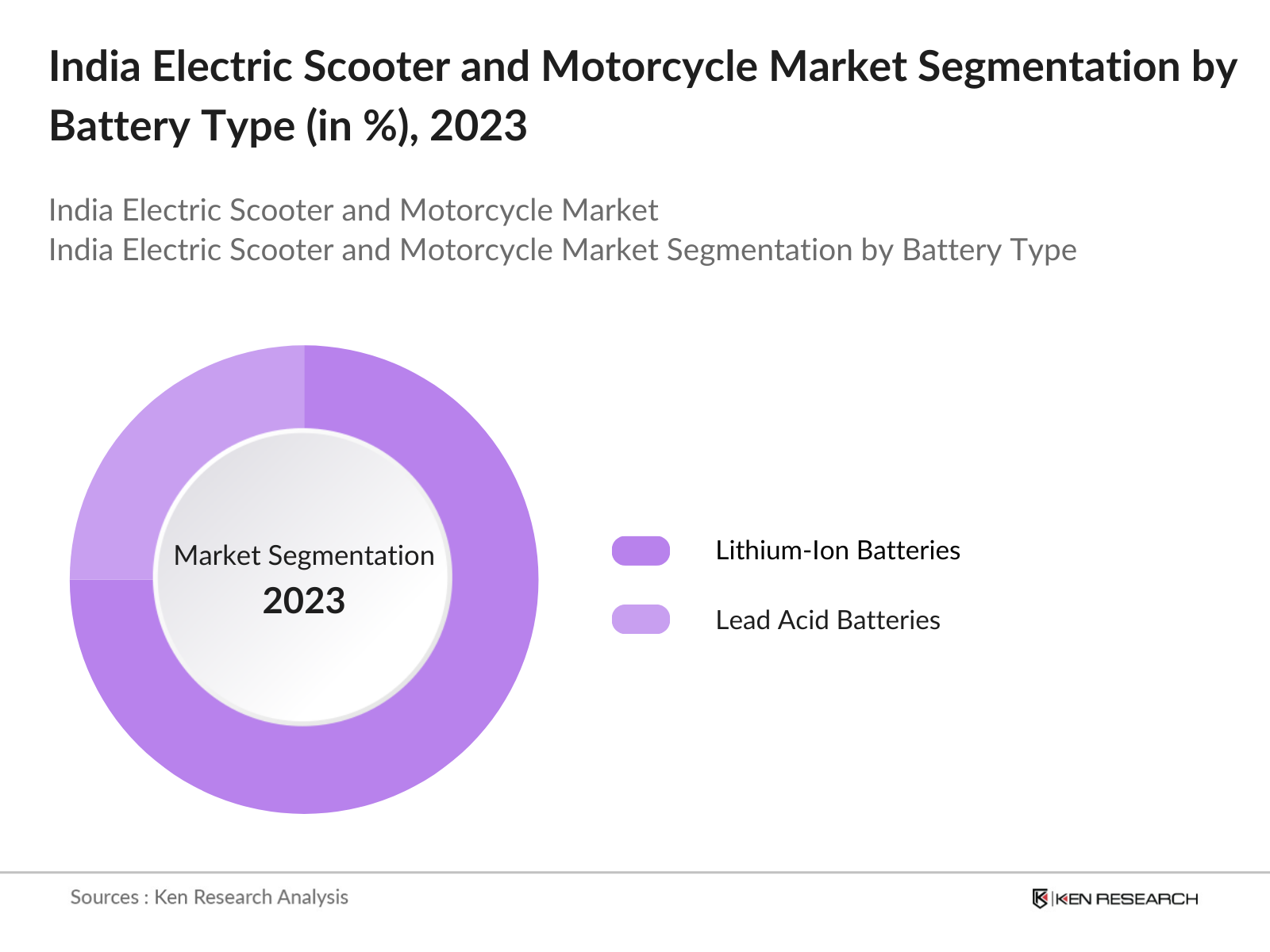

By Battery Type: The market is segmented by battery type into lithium-ion batteries and lead-acid batteries. Lithium-ion batteries dominate this segment due to their longer lifespan, higher energy density, and reduced charging time. These batteries, while more expensive, are favored by manufacturers and consumers alike for their superior performance and longer range. Their prevalence is largely driven by advancements in technology and declining costs, making them the preferred choice for electric two-wheelers in India.

India Electric Scooter and Motorcycle Market Competitive Landscape

The India Electric Scooter and Motorcycle market is characterized by both established players and emerging start-ups. Established companies like Hero Electric and TVS dominate the market, alongside newer players such as Ather Energy and Ola Electric, which have quickly gained a competitive edge through technological innovation and aggressive marketing strategies. The growing interest of global investors in the Indian EV ecosystem further boosts competition, fostering rapid development in this space.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (INR) |

Number of Models |

R&D Expenditure (%) |

No. of Employees |

Manufacturing Plants |

Distribution Network |

|

Hero Electric |

1956 |

New Delhi |

20 bn |

6 |

4% |

2000 |

3 |

Pan-India |

|

Ather Energy |

2013 |

Bengaluru |

10 bn |

3 |

15% |

1000 |

2 |

South & West India |

|

Ola Electric |

2017 |

Bengaluru |

30 bn |

2 |

12% |

5000 |

1 |

Pan-India |

|

TVS Motor Company |

1978 |

Chennai |

40 bn |

4 |

6% |

4000 |

3 |

Pan-India |

|

Bajaj Auto |

1945 |

Pune |

50 bn |

3 |

5% |

7000 |

5 |

Pan-India |

India Electric Scooter and Motorcycle Industry Analysis

Growth Drivers

- Rising Fuel Costs: Rising fuel costs are a primary driver for the adoption of electric scooters and motorcycles. In 2022, petrol prices soared to INR 105 per liter, marking an increase of approximately 30% since 2021. This dramatic rise in fuel expenses has prompted consumers to seek more economical alternatives. Furthermore, the Indian government aims to reduce oil imports by 10% by 2025, further emphasizing the need for electric mobility solutions. This trend is expected to continue driving consumer preference towards electric two-wheelers as a cost-effective transportation option.

- Government Incentives: Government incentives play a crucial role in promoting electric vehicle adoption. The FAME-II scheme has allocated INR 10,000 crore to support electric vehicle production and subsidies, with approximately 600,000 electric two-wheelers sold under this initiative by 2023. Additionally, various state governments, including Delhi and Maharashtra, have introduced their own subsidy programs, offering financial support of up to INR 30,000 per vehicle. These combined incentives significantly lower the effective cost of electric two-wheelers, enhancing their attractiveness among consumers and accelerating market growth.

- Urban Mobility Trends: Urban mobility trends are shifting towards electric two-wheelers, driven by the need for efficient and eco-friendly transportation solutions. As of 2022, over 40% of urban trips in India are less than 5 kilometers, indicating a strong market potential for electric scooters and motorcycles, which are ideal for short-distance commuting. Furthermore, cities like Bengaluru and Delhi are experiencing increased congestion, making electric two-wheelers a practical alternative. This alignment with urban mobility needs is likely to foster sustained demand for electric two-wheelers in metropolitan areas.

Market Challenges

- High Battery Costs: High battery costs remain a significant challenge for the electric scooter and motorcycle market. As of 2022, lithium-ion batteries accounted for nearly 40% of the total vehicle cost, with prices ranging from INR 30,000 to INR 50,000 per unit. This financial burden limits accessibility for price-sensitive consumers, hindering broader adoption. Furthermore, the recent fluctuations in raw material prices, particularly lithium and cobalt, have exacerbated these costs, making it imperative for manufacturers to explore more cost-effective battery technologies to enhance market penetration.

- Lack of Charging Infrastructure: The lack of charging infrastructure poses a significant hurdle for electric two-wheeler adoption. As of early 2023, India had only about 1,800 public charging stations, which is insufficient to support the growing number of electric vehicles. With the government targeting 10,000 charging stations by 2025, the current infrastructure gap hampers consumer confidence, especially regarding range anxiety. Addressing this issue is critical to fostering a conducive environment for electric two-wheelers, requiring collaborative efforts from both public and private sectors to build a robust charging network.

India Electric Scooter and Motorcycle Future Outlook

Over the next five years, the India Electric Scooter and Motorcycle market is expected to experience substantial growth driven by advancements in battery technology, increasing government support, and a rising consumer demand for eco-friendly transportation solutions. As the adoption of electric two-wheelers grows, especially in urban areas, market players will focus on expanding their product lines and building better charging infrastructure to cater to growing consumer needs. Furthermore, Indias push toward reducing carbon emissions and improving air quality will encourage more consumers to make the switch to electric vehicles.

Future Opportunities

- Innovations in Battery Technology : Innovations in battery technology, particularly solid-state batteries, present significant opportunities for the electric two-wheeler market. Solid-state batteries offer advantages such as higher energy density and improved safety over traditional lithium-ion batteries. As of 2023, companies like Ather Energy are investing in research to develop solid-state batteries that could potentially reduce costs and enhance range. This technological advancement could lead to a transformative shift in the market, making electric scooters and motorcycles more appealing to consumers and accelerating their adoption.

- Expansion in Tier-2 and Tier-3 Cities: The expansion of electric two-wheelers into Tier-2 and Tier-3 cities presents a lucrative growth opportunity. In 2022, these regions accounted for nearly 30% of overall two-wheeler sales, and with increasing awareness of electric vehicles, this share is expected to rise. Local manufacturers are beginning to introduce affordable models tailored for these markets, with features suited to regional needs. This expansion is critical for achieving the government's goal of increasing electric vehicle penetration across diverse urban landscapes, thus driving overall market growth. Source: Ministry of Heavy Industries and Public Enterprises.

Scope of the Report

|

By Vehicle Type |

Electric Scooters Electric Motorcycles |

|

By Battery Type |

Lithium-ion Batteries Lead Acid Batteries |

|

By Power Output |

<3 kW 3-5 kW >5 kW |

|

By Charging Type |

Fixed Charging Swappable Charging |

|

By Region |

Northern India Southern India Western India Eastern India |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Electric Two-Wheeler Companies

Battery Supplier Companies

Charging Infrastructure Companies

Automobile Dealership Networks and Companies

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Road Transport and Highways, NITI Aayog)

Ride-Sharing and Fleet Management Companies

Aftermarket Service Companies

Companies

Players Mentioned in the Report:

Hero Electric

Ather Energy

Ola Electric

TVS Motor Company

Bajaj Auto

Revolt Motors

Okinawa Autotech Pvt. Ltd.

Ampere Vehicles

Pure EV

Ultraviolette Automotive Pvt. Ltd.

Table of Contents

1. India Electric Scooter and Motorcycle Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Electric Scooter and Motorcycle Market Size (In INR Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Electric Scooter and Motorcycle Market Analysis

3.1. Growth Drivers

3.1.1. Rising Fuel Costs

3.1.2. Government Incentives (FAME-II, State Subsidies)

3.1.3. Urban Mobility Trends

3.1.4. Environmental Concerns (Emission Reduction Targets)

3.2. Market Challenges

3.2.1. High Battery Costs

3.2.2. Lack of Charging Infrastructure

3.2.3. Performance Limitations (Range Anxiety, Power Output)

3.3. Opportunities

3.3.1. Innovations in Battery Technology (Solid-State Batteries)

3.3.2. Expansion in Tier-2 and Tier-3 Cities

3.3.3. Fleet Electrification (Delivery and Ride-Sharing)

3.4. Trends

3.4.1. Adoption of Swappable Battery Systems

3.4.2. Integration with Smart Mobility Solutions

3.4.3. Increasing Role of Fintech in EV Financing

3.5. Government Regulation

3.5.1. Faster Adoption and Manufacturing of Electric Vehicles (FAME)

3.5.2. State-Level EV Policies (Delhi, Karnataka, Maharashtra)

3.5.3. GST Reductions and Duty Exemptions

3.6. SWOT Analysis

3.7. Stake Ecosystem (Suppliers, Manufacturers, Distributors, Financiers)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. India Electric Scooter and Motorcycle Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Electric Scooters

4.1.2. Electric Motorcycles

4.2. By Battery Type (In Value %)

4.2.1. Lithium-ion Batteries

4.2.2. Lead Acid Batteries

4.3. By Power Output (In Value %)

4.3.1. <3 kW

4.3.2. 3-5 kW

4.3.3. >5 kW

4.4. By Charging Type (In Value %)

4.4.1. Fixed Charging

4.4.2. Swappable Charging

4.5. By Region (In Value %)

4.5.1. Northern India

4.5.2. Southern India

4.5.3. Western India

4.5.4. Eastern India

5. India Electric Scooter and Motorcycle Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Hero Electric

5.1.2. Ather Energy

5.1.3. Ola Electric

5.1.4. Bajaj Auto Ltd.

5.1.5. TVS Motor Company

5.1.6. Revolt Motors

5.1.7. Okinawa Autotech Pvt. Ltd.

5.1.8. Ampere Vehicles

5.1.9. Pure EV

5.1.10. Ultraviolette Automotive Pvt. Ltd.

5.1.11. Mahindra Electric

5.1.12. Yulu Bikes

5.1.13. Tork Motors

5.1.14. Bounce Infinity

5.1.15. Kinetic Green Energy

5.2. Cross Comparison Parameters

5.2.1. No. of Employees

5.2.2. Headquarters

5.2.3. Inception Year

5.2.4. Revenue

5.2.5. Market Share

5.2.6. R&D Expenditure

5.2.7. Number of Models in Market

5.2.8. Distribution Network

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. India Electric Scooter and Motorcycle Market Regulatory Framework

6.1. EV Policy Framework

6.2. Certification and Compliance Requirements

6.3. Environmental and Safety Standards

7. India Electric Scooter and Motorcycle Future Market Size (In INR Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Electric Scooter and Motorcycle Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Battery Type (In Value %)

8.3. By Power Output (In Value %)

8.4. By Charging Type (In Value %)

8.5. By Region (In Value %)

9. India Electric Scooter and Motorcycle Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first phase involves identifying critical market variables such as demand trends, regulatory framework, and technological advancements in the India Electric Scooter and Motorcycle Market. This was done through comprehensive secondary research and industry insights, including proprietary databases and government reports.

Step 2: Market Analysis and Construction

Historical data for the electric two-wheeler market was compiled and analyzed to understand the growth trajectory. The analysis included vehicle penetration, price trends, and supply chain logistics, helping build a robust picture of market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Key market assumptions were validated by conducting interviews with industry experts and executives from leading companies. These interviews provided real-time feedback, allowing us to refine the market projections and validate key metrics.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing data from various sources and cross-verifying it with primary research findings to provide a comprehensive, accurate, and actionable analysis of the India Electric Scooter and Motorcycle Market.

Frequently Asked Questions

01. How big is the India Electric Scooter and Motorcycle Market?

The India Electric Scooter and Motorcycle Market is valued at USD 647 million, driven by rising fuel costs, government incentives, and the increasing demand for eco-friendly transportation options.

02. What are the challenges in the India Electric Scooter and Motorcycle Market?

Challenges include high battery costs, lack of sufficient charging infrastructure, and concerns over range anxiety, which have slowed the adoption of electric two-wheelers among the Indian population.

03. Who are the major players in the India Electric Scooter and Motorcycle Market?

Key players in the market include Hero Electric, Ather Energy, Ola Electric, Bajaj Auto, and TVS Motor Company, with Hero Electric and Ather Energy leading due to their innovative product offerings and government backing.

04. What are the growth drivers of the India Electric Scooter and Motorcycle Market?

Growth drivers include rising urbanization, increased consumer awareness of environmental issues, government policies like FAME II, and advancements in battery technology that improve vehicle efficiency.

05. How is the battery technology evolving in the India Electric Scooter and Motorcycle Market?

The market is seeing rapid advancements in lithium-ion battery technology, which offers greater efficiency, faster charging times, and longer range compared to traditional lead-acid batteries. These improvements are critical for the wider adoption of electric two-wheelers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.