India FMCG Market Outlook to 2030

Region:Asia

Author(s):Shreya Garg

Product Code:KROD8136

December 2024

97

About the Report

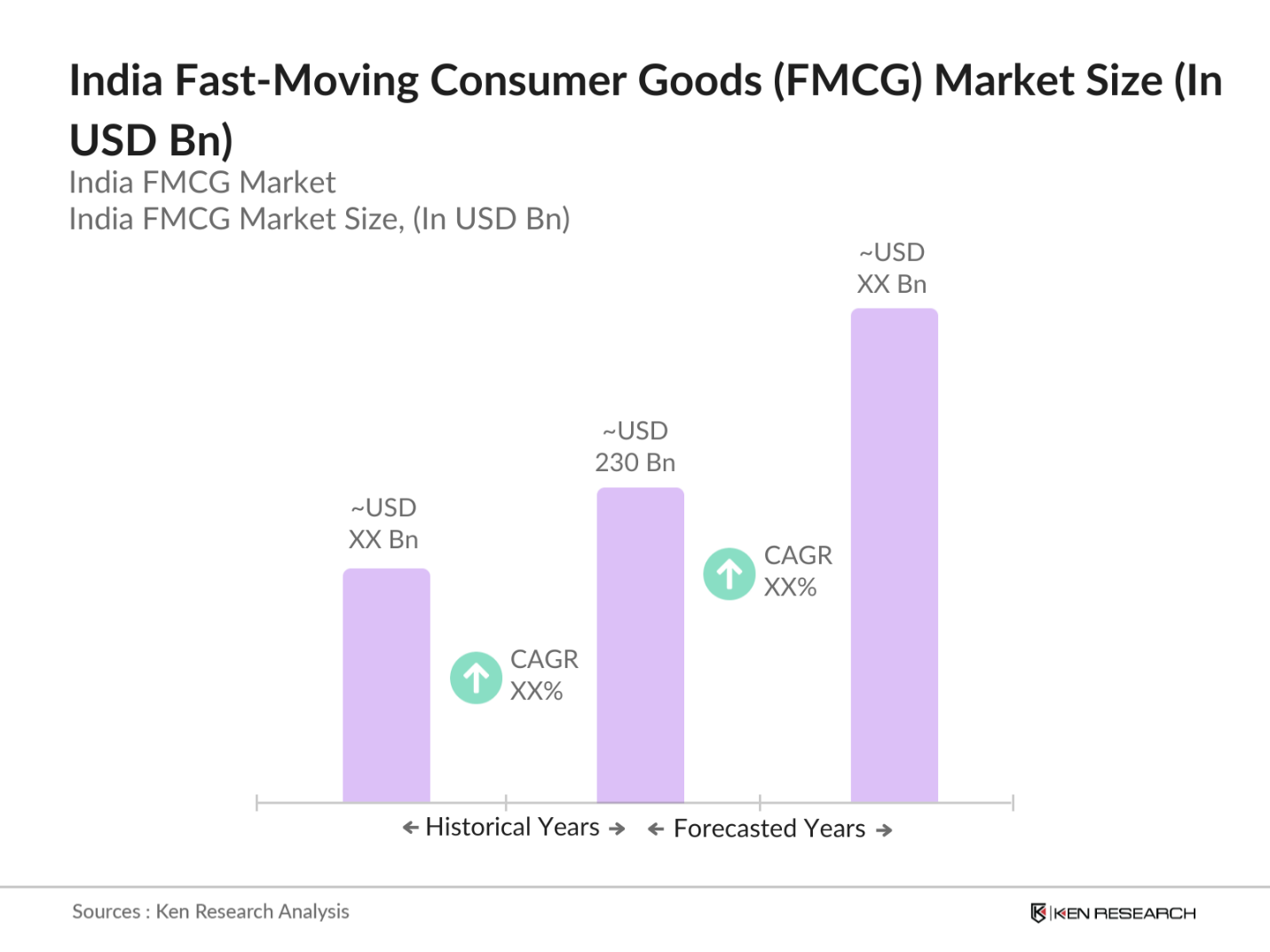

India FMCG Market Overview

- The India FMCG market is valued at USD 230 billion, based on a five-year historical analysis. This markets robust growth is propelled by rising disposable incomes, a growing middle class, and a shift in consumer preferences toward convenience and quality. Increasing urbanization and deeper market penetration into rural areas have further bolstered demand across product categories, such as personal care and packaged food. Additionally, the rise in online retail channels is transforming the distribution landscape, making FMCG products more accessible to a wider consumer base.

- In India, major cities such as Mumbai, Delhi, and Bangalore are the primary drivers in the FMCG sector due to their higher purchasing power, diverse consumer base, and greater exposure to modern retail and e-commerce channels. Rural areas, particularly in states like Uttar Pradesh and Maharashtra, have also seen an uptick in demand as FMCG companies increase their outreach through localized distribution strategies and product offerings tailored to rural preferences. This regional diversity contributes to a broad spectrum of demand, making both urban and rural markets critical to the industry's growth trajectory.

- The Food Safety and Standards Authority of India (FSSAI) enforces strict food safety regulations, impacting FMCG companies. Compliance with FSSAI guidelines is mandatory, affecting product labeling, ingredient disclosure, and quality control. According to FSSAI, over 150,000 food samples were tested in 2023, reflecting the high regulatory focus on food safety. Non-compliance penalties motivate companies to adhere to these standards, which ensure consumer trust in FMCG products.

India FMCG Market Segmentation

By Product Type: The market is segmented by product type into personal care, food & beverages, home care, health & hygiene, and over the counter (OTC) products. Recently, personal care products dominate this segment due to increased consumer interest in grooming and wellness. With a heightened awareness of skincare and hygiene, and brands emphasizing premiumization, this category has witnessed significant traction. Companies like Hindustan Unilever and Dabur have fortified their brand presence by offering a diverse range of products catering to various consumer needs.

By Sales Channel: The market in India is segmented by sales channel into modern retail, traditional retail, e-commerce, and direct sales. Traditional retail holds a dominant position in this segment, largely due to the extensive network of kirana (small grocery) stores, which are highly accessible and trusted by consumers, particularly in semi-urban and rural areas. Modern retail and e-commerce are quickly gaining ground, driven by urban consumers who seek convenience and a wide range of choices online. This shift is also propelled by increased internet penetration and growing comfort with digital transactions.

India FMCG Market Competitive Landscape

The India FMCG market is led by prominent players with both local and international roots. Companies such as Hindustan Unilever, ITC Limited, and Nestl India dominate due to their extensive distribution networks, diverse product portfolios, and strong brand equity. This competitive structure has resulted in high market consolidation, with leading brands continuously innovating to address evolving consumer demands.

India FMCG Industry Analysis

Growth Drivers

- Urbanization & Changing Lifestyles: Indias urban population has reached approximately 480 million in 2024, driven by rural-to-urban migration and expanding urban areas. This urbanization is altering consumer preferences, pushing demand for convenient FMCG products suited to fast-paced lifestyles. According to the United Nations, Indias urban share of the population is expected to continue growing, intensifying demand for ready-to-eat foods, personal care items, and other quick-consumption products in urban centers. This urban shift influences retail expansion, with organized retail contributing significantly to the FMCG sectors growth, helping drive GDP per capita beyond $2,500 as per the World Bank.

- Increase in Disposable Income: India's gross national income per capita reached $2,310 in 2023, according to the World Bank, reflecting an increase in disposable incomes across households. This rising disposable income has enabled greater consumer spending on premium FMCG products, particularly within urban and semi-urban areas. The boost in purchasing power is a major contributor to FMCG growth, especially in segments like beauty, personal care, and household products. This trend, coupled with a projected increase in consumer spending, underscores a robust market for value-added goods, impacting the FMCG market's structure.

- E-commerce Expansion: Indias e-commerce industry saw sales figures surpassing 1.2 billion transactions in 2023, according to Ministry of Electronics & IT. With expanded digital access, over 700 million Indians are now internet users, facilitating e-commerces rapid integration into the FMCG market. Consumer behavior has shifted online for purchases of essentials and personal care products, with companies like Amazon and Flipkart boosting FMCG distribution. As the government enhances digital infrastructure, online FMCG channels are poised to serve urban and rural consumers alike.

Market Challenges

- Regulatory Compliance and GST Impact: Compliance with the Goods and Services Tax (GST) is essential for FMCG companies, impacting logistics and pricing. The GST rate structure for FMCG goods has affected pricing dynamics, especially for processed food items. According to Indias Ministry of Finance, the FMCG sector is challenged by varied GST rates (5%, 12%, and 18%) on different product categories, impacting profit margins for FMCG companies. The intricate regulatory compliance process adds to operational costs, influencing pricing for end consumers.

- Intense Market Competition: Indias FMCG market hosts numerous domestic and international players, with brands competing across categories like food, beverages, and personal care. Intense competition in the market challenges new entrants and increases customer acquisition costs. Data from Indias Department for Promotion of Industry and Internal Trade reveals the establishment of more than 20,000 new FMCG companies since 2022, which has led to aggressive price wars, promotional discounts, and heightened consumer expectations.

India FMCG Market Future Outlook

The India FMCG market is projected to sustain its upward trajectory due to demographic shifts, increased rural penetration, and consumer inclination toward value-added products. The proliferation of digital channels, alongside government initiatives to boost rural consumption, will continue to foster market expansion. With a focus on sustainable practices and health-oriented products, the market is well-positioned to cater to the evolving preferences of the Indian consumer.

Future Market Opportunities

- Growth in Health & Wellness Segments: Consumer interest in health and wellness products is surging, with a growing demand for nutritious foods, organic personal care products, and immunity-boosting items. According to the Ministry of Health and Family Welfare, the focus on health has driven up the demand for fortified foods and products catering to specific health needs. FMCG companies are expanding offerings in this space to meet the health-conscious consumer market, representing a lucrative growth area in the sector.

- Private Label Expansion: Retailers in India have increasingly introduced private label FMCG products, capitalizing on cost-conscious consumers and offering competitive pricing. Data from the Ministry of Commerce highlights that private labels have grown by 15% in sales volume in major retail chains, driven by economic pricing and tailored products for specific consumer needs. This shift reflects consumer preference for affordable quality products, especially in food, home care, and personal care categories, presenting a substantial opportunity for retailers.

Scope of the Report

|

By Product Type |

Personal Care Food & Beverages Home Care Health & Hygiene OTC Products |

|

By Sales Channel |

Modern Retail Traditional Retail E-commerce Direct Sales |

|

By Demographic |

Urban Semi-Urban Rural |

|

By Distribution Mode |

Direct Distribution Distributors Third-Party Logistics |

|

By Region |

North South East West |

Products

Key Target Audience

FMCG Retailers and Distributors

E-commerce Platforms

Modern Trade Chains

FMCG Manufacturers and Suppliers

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (FSSAI, Ministry of Consumer Affairs)

Packaging and Logistics Providers

Digital Marketing and Advertising Firms

Companies

Major Players

Hindustan Unilever

ITC Limited

Nestl India

Dabur India

Godrej Consumer Products

Procter & Gamble India

Marico Limited

Colgate-Palmolive India

Emami Limited

Patanjali Ayurved

Britannia Industries

Reckitt Benckiser India

PepsiCo India Holdings

Johnson & Johnson India

Amul (Gujarat Co-operative Milk Marketing Federation)

Table of Contents

India FMCG Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics (Growth Rate, Drivers, Challenges)

1.4. Market Segmentation Overview

India FMCG Market Size (In INR Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Developments and Industry Milestones

India FMCG Market Analysis

3.1. Growth Drivers

3.1.1. Urbanization & Changing Lifestyles

3.1.2. Increase in Disposable Income

3.1.3. E-commerce Expansion

3.1.4. Rural Market Penetration

3.2. Market Challenges

3.2.1. Regulatory Compliance and GST Impact

3.2.2. Intense Market Competition

3.2.3. Rising Raw Material Costs

3.3. Opportunities

3.3.1. Growth in Health & Wellness Segments

3.3.2. Private Label Expansion

3.3.3. Demand for Natural and Organic Products

3.4. Market Trends

3.4.1. Sustainability Initiatives (Eco-Friendly Packaging)

3.4.2. Digital Marketing and Influencer Impact

3.4.3. Direct-to-Consumer (DTC) Models

3.5. Government Regulations

3.5.1. FSSAI Guidelines

3.5.2. Labeling and Packaging Standards

3.5.3. Foreign Direct Investment (FDI) Policies

3.6. SWOT Analysis

3.7. Value Chain and Distribution Network

3.8. Porters Five Forces

3.9. Competition Ecosystem

India FMCG Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Personal Care

4.1.2. Food & Beverages

4.1.3. Home Care

4.1.4. Health & Hygiene

4.1.5. Over-the-Counter (OTC) Products

4.2. By Sales Channel (In Value %)

4.2.1. Modern Retail (Supermarkets, Hypermarkets)

4.2.2. Traditional Retail (Kiranas, Local Shops)

4.2.3. E-commerce Platforms

4.2.4. Direct Sales

4.3. By Demographic (In Value %)

4.3.1. Urban

4.3.2. Semi-Urban

4.3.3. Rural

4.4. By Distribution Mode (In Value %)

4.4.1. Direct Distribution

4.4.2. Distributors and Wholesalers

4.4.3. Third-Party Logistics

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

India FMCG Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Hindustan Unilever

5.1.2. ITC Limited

5.1.3. Nestle India

5.1.4. Procter & Gamble India

5.1.5. Dabur India

5.1.6. Godrej Consumer Products

5.1.7. Marico Limited

5.1.8. Emami Limited

5.1.9. Britannia Industries

5.1.10. Patanjali Ayurved

5.1.11. Colgate-Palmolive India

5.1.12. Johnson & Johnson India

5.1.13. Reckitt Benckiser India

5.1.14. Amul (Gujarat Co-operative Milk Marketing Federation)

5.1.15. PepsiCo India Holdings

5.2 Cross Comparison Parameters (Market Share, Revenue, Distribution Reach, Product Portfolio, Brand Equity, Digital Presence, Sustainability Initiatives, Innovation Index)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers & Acquisitions

5.6. Investment & Funding Analysis

5.7. Venture Capital & Private Equity Investments

5.8. Government Incentives & Subsidies

India FMCG Market Regulatory Framework

6.1. FSSAI Regulations and Amendments

6.2. Environmental Compliance (Plastic Usage & Waste Management)

6.3. Advertising Standards & Consumer Protection

6.4. Employment & Labor Laws

India FMCG Future Market Size (In INR Bn)

7.1. Future Market Size Projections

7.2. Key Factors Influencing Future Growth

India FMCG Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Sales Channel (In Value %)

8.3. By Demographic (In Value %)

8.4. By Distribution Mode (In Value %)

8.5. By Region (In Value %)

India FMCG Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior Analysis

9.3. Market Entry & Expansion Strategies

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map that encompasses all major stakeholders in the India FMCG Market. This step relies on extensive desk research to gather comprehensive industry-level data, focusing on factors such as distribution channels, consumer preferences, and key growth drivers.

Step 2: Market Analysis and Construction

In this phase, historical data on the India FMCG Market is compiled and analyzed. This includes examining the market structure, evaluating key product segments, and understanding consumer behavior dynamics to construct a reliable growth narrative and accurate revenue estimation.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews (CATIs) with industry experts. These consultations yield valuable insights from practitioners, which serve to verify and enrich the data analysis with practical insights.

Step 4: Research Synthesis and Final Output

The final stage involves synthesizing data obtained from direct engagement with FMCG manufacturers and distributors. This stage is essential for refining the analysis and ensuring a comprehensive and validated representation of the India FMCG markets dynamics and opportunities.

Frequently Asked Questions

01. How big is the India FMCG Market?

The India FMCG market is valued at USD 230 billion, driven by an expanding middle class, increased disposable incomes, and the growth of e-commerce channels.

02. What are the challenges in the India FMCG Market?

Challenges in the India FMCG market include intense competition, regulatory compliance issues, and rising raw material costs, which can impact profit margins and operational efficiencies for companies.

03. Who are the major players in the India FMCG Market?

Key players in the India FMCG market include Hindustan Unilever, ITC Limited, Nestl India, and Dabur India. These companies hold substantial influence due to their strong brand presence and extensive distribution networks.

04. What are the growth drivers of the India FMCG Market?

Growth in the India FMCG market is driven by factors such as urbanization, digital transformation, and increased consumer preference for convenience products. Additionally, rural market penetration remains a key driver for industry expansion.

05. What is the impact of digital channels on the India FMCG Market?

The rise of digital channels has expanded the reach of FMCG products, especially in urban areas, by making them accessible online, which aligns with the changing shopping behaviors of tech-savvy consumers in the India FMCG market.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.