India Technology Hardware Market Outlook to 2028

Region:Asia

Author(s):Sudhanshu Maheshwari

Product Code:KROD6363

March 2025

80-100

About the Report

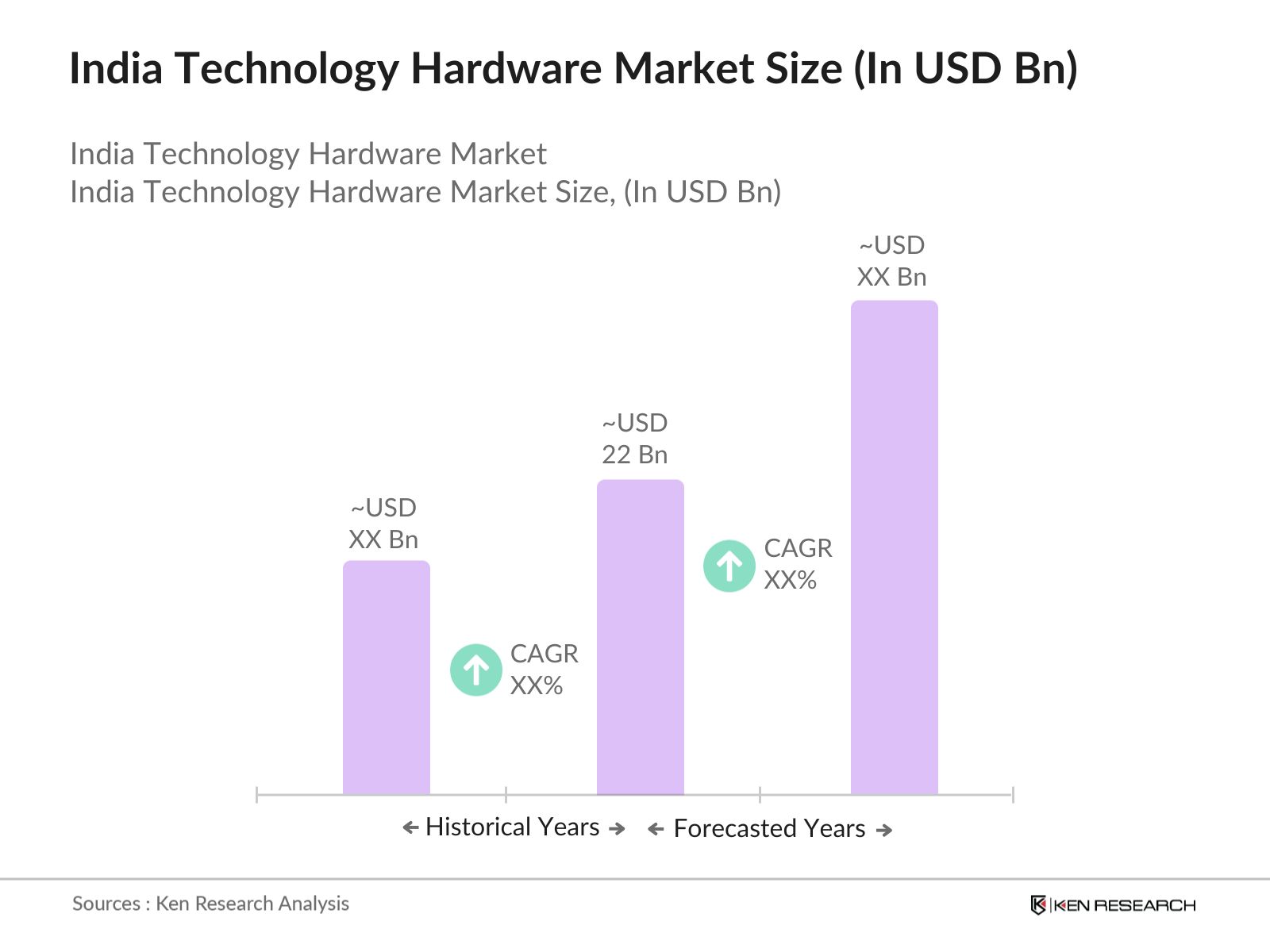

India Technology Hardware Market Overview

- The India technology hardware market is valued at USD 22 billion based on a five-year historical analysis. The growth has been driven by increasing digitization across industries, government-led initiatives like the Production-Linked Incentive (PLI) scheme, and a rise in consumer electronics demand post-pandemic. According to the Ministry of Electronics and Information Technology (MeitY) and IBEF, the electronics manufacturing sector grew significantly with domestic manufacturing contributing a substantial share. The proliferation of smartphones, enterprise servers, laptops, networking equipment, and IoT devices across sectors has underpinned this market growth.

- The cities dominating the Indian technology hardware market include Bengaluru, Hyderabad, Noida, and Chennai. Bengaluru is recognized as India's Silicon Valley, housing several global and domestic OEMs, R&D centers, and component manufacturers. Hyderabad has become a hub for semiconductor design and embedded system companies. Chennai and Noida are key due to their robust electronics manufacturing clusters and logistical advantages, supporting large-scale exports and domestic demand fulfillment.

- Indias Production-Linked Incentive (PLI) Scheme (2024) provides incentives of up to INR 17,000 crore to boost local production of laptops, tablets, servers, and computer hardware. Revised customs tariffs (HS Code 8471) increase duties on imported finished goods and lower input component tariffs to enhance local manufacturing. Updated BIS certification and Digital India initiatives requiring public procurement of domestically produced hardware further support India's IT hardware manufacturing ecosystem.

India Technology Hardware Market Segmentation

- By Device Type: Indias technology hardware market is segmented by device type into consumer devices, enterprise devices, networking hardware, peripherals, and embedded & IoT devices. Recently, consumer devices have a dominant market share in India under the segmentation device type. This is due to the surge in smartphone penetration, rising demand for laptops for remote work and education, and increased affordability driven by domestic production under schemes like PLI. Brands like Xiaomi, HP, Lenovo, and Samsung have capitalized on online and offline retail expansion, making consumer electronics more accessible across Tier I, II, and III cities.

- By Application: Indias technology hardware market is segmented by application into IT & ITeS, BFSI, manufacturing & industrial automation, education & edtech, and government & defense. Among these, IT & ITeS holds a dominant market share. This is due to Indias strong position as a global IT hub, the presence of major IT service providers, and the heavy use of enterprise hardware such as data servers, firewalls, and networking equipment. Furthermore, the increase in cloud services and demand for edge computing has driven server and data center hardware demand in this segment, with key investments from both Indian and global players.

India Technology Hardware Market Competitive Landscape

The India technology hardware market is dominated by a mix of domestic champions and global OEMs such as HP, Dell, Lenovo, Dixon Technologies, and Foxconn India. This consolidation highlights the significant influence of these key companies in driving pricing, innovation, and manufacturing localization strategies. Several players have shifted assembly lines to India due to geopolitical supply chain shifts and government subsidies, increasing their local footprint and competitiveness.

India Technology Hardware Market Analysis

Growth Drivers

- Surge in Domestic Electronics Production: In 2024, India's electronics manufacturing exceeded 5.2 billion units, including computers and telecom devices, driven by the PLI scheme for IT hardware. Large-scale assembly operations emerged in Uttar Pradesh, Tamil Nadu, and Karnataka. Over 50 industrial parks were supported through the Electronics Manufacturing Clusters program. Domestic assembly of PCBs and peripherals rose 30%, generating more than 750,000 direct manufacturing-linked jobs nationwide, boosting backward integration.

- Rising Demand for Consumer Tech Devices: India's growing digital consumer base fuels demand for tech hardware. With 24 million births recorded in 2024, the need for educational tablets and laptops for digital literacy is expanding. Over 325 million school-age children and increased digitization in rural education have sharply increased hardware demand. The Universal Service Obligation Fund equipped 310,000 digital classrooms, significantly driving procurement of computers and networking equipment across India.

- Electronics Export Momentum Strengthens: Indias electronics exports expanded notably in 2024, shipping over 1.8 million units of PCs and tablets to Southeast Asia, Africa, and Latin America. Component exports, including motherboards and memory modules, exceeded 290,000 metric tonnes. Local packaging units exported 17,400 tonnes of ICs and chips, highlighting India's emerging capabilities in semiconductor backend processing. This growth underscores India's strengthened manufacturing position in global IT hardware markets.

Market Challenges

- Heavy Reliance on Imported Semiconductors: India remains heavily dependent on semiconductor imports. According to the Ministry of Commerce, in 2024, India imported over 68,500 tones of integrated circuits (ICs), with major sources being Taiwan, South Korea, and China. Despite the Semiconductor Mission launched in 2022, fab capacity remains at infancy stages. The absence of localized silicon wafer production has resulted in extended lead times and high forex outflows. Further, nearly 90% of processors and memory chips used in Indian-assembled desktops and laptops are still imported, making the sector vulnerable to global supply chain shocks and price volatility in raw silicon materials.

- Limited High-Precision Component Ecosystem: India's domestic capability to produce high-end components such as printed circuit boards (PCBs), system-on-chips (SoCs), and DRAM modules remains limited. As of 2024, data from MeitY indicates India manufactures less than 12% of PCBs used in locally assembled laptops and desktops. Imports of high-frequency processors and power management chips have crossed 44,300 tonnes, sourced mainly from Japan and the US. This overdependence stifles cost competitiveness and delays production cycles. Additionally, quality precision tooling infrastructure remains underdeveloped in many tier-2 cities, limiting MSMEs from entering the high-spec component manufacturing space.

India Technology Hardware Market Future Outlook

Over the next 5 years, the India technology hardware market is expected to show significant growth driven by continuous government support, advancements in hardware technology, and the localization of electronic manufacturing. Rising digital infrastructure investments, expansion of 5G networks, and the adoption of smart devices across urban and semi-urban areas will further catalyze growth. Moreover, Indias push for semiconductor self-reliance and data localization is likely to open new opportunities in component manufacturing and high-end computing devices.

Market Opportunities

- Infrastructure Digitization Driving Hardware Demand: India's push for digital infrastructure has created rising demand for computing devices and storage hardware. As per the Ministry of Electronics and IT, over 690,000 government offices have adopted digital workflows requiring computer systems, external drives, and servers. The ongoing BharatNet Phase-II program covers 186,000 village panchayats, with networking hardware and routers installed. Additionally, the Smart Cities Mission has seen installation of 58,000 surveillance nodes and command centers that require data servers, network switches, and computing peripherals. These deployments are triggering a demand wave for hardware logistics, support services, and assembly units domestically.

- Rising Demand for Enterprise IT Hardware: Rising corporate and institutional digitization is expected to significantly boost IT hardware demand in India. With active companies projected to surpass 1.85 million, sectors like BFSI, IT, and logistics will increasingly upgrade enterprise servers, desktops, and networking infrastructure. India's data center capacity, already exceeding 880 MW, will further expand, creating sustained opportunities for local manufacturers in producing servers, storage solutions, and secure routers to meet growing corporate needs.

Scope of the Report

|

By Device Type |

Consumer Devices |

|

By Application |

IT & ITeS |

|

By End-User |

Enterprise |

|

By Distribution Channel |

Online Retail |

|

By Region |

North |

Products

Key Target Audience

- Consumer Electronics OEMs

- Enterprise Hardware Distributors

- IT & ITeS Solution Providers

- Embedded System Manufacturers

- Telecommunications Infrastructure Companies

- Investors and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Electronics & Information Technology, DPIIT)

- Industrial Automation and Manufacturing Technology Firms

Companies

Players Mentioned in the Report

- HP India

- Dell Technologies

- Lenovo India

- Dixon Technologies

- Foxconn India

Table of Contents

1. India Technology Hardware Market Overview

1.1. Definition and Scope (Consumer Electronics, Industrial Hardware, Enterprise Devices, Embedded Systems, Network Equipment)

1.2. Market Taxonomy (Component Type, Application, End-User, Distribution Channel, Region)

1.3. Market Growth Rate (CAGR, QoQ, YoY)

1.4. Market Segmentation Overview (Devices, End-User Industry, Technology Level, Sales Channel, Regional Split)

2. India Technology Hardware Market Size (INR Cr & USD Mn)

2.1. Historical Market Size (Device Category-Wise: Laptops, Servers, Networking Devices, etc.)

2.2. Year-On-Year Growth Analysis (Device-Level YoY Growth, Channel-Specific Growth, OEM Growth)

2.3. Key Market Developments and Milestones (Product Launches, JV Announcements, Domestic Manufacturing Initiatives)

3. India Technology Hardware Market Analysis

3.1. Growth Drivers

3.1.1. Surge in Domestic Electronics Production

3.1.2. Rising Demand for Consumer Tech Devices

3.1.3. Electronics Export Momentum Strengthens

3.1.4. Rising Demand for Data Centers

3.1.5. Smartphone and Consumer Electronics Penetration

3.2. Restraints

3.2.1. Heavy Reliance on Imported Semiconductors

3.2.2. Limited High-Precision Component Ecosystem

3.2.3. Price Sensitivity in Mass Market Segments

3.3. Opportunities

3.3.1. Infrastructure Digitization Driving Hardware Demand

3.3.2. Rising Demand for Enterprise IT Hardware

3.3.3. Government Procurement for Public Sector Digitalization

3.4. Trends

3.4.1. Increasing Integration of AI/ML in Devices

3.4.2. Demand for Energy-Efficient Hardware

3.4.3. Embedded Systems in Smart Appliances

3.4.4. Expansion of Aftermarket and Refurbished Devices

3.5. Regulatory Environment

3.5.1. PLI Scheme for IT Hardware

3.5.2. Customs Duties and Import Tariffs

3.5.3. BIS Certification for Electronic Devices

3.5.4. E-Waste Management Rules

3.6. SWOT Analysis (Specific to Indian Tech Hardware Ecosystem)

3.7. Stakeholder Ecosystem (OEMs, ODMs, Retailers, Logistics, System Integrators)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Threat of Substitution, Competitive Rivalry, Barriers to Entry)

3.9. Competition Ecosystem (Component Suppliers, System Integrators, B2B vs B2C Players)

4. India Technology Hardware Market Segmentation

4.1. By Device Type (In Value %)

4.1.1. Consumer Devices

4.1.2. Enterprise Devices

4.1.3. Networking Hardware

4.1.4. Peripherals

4.1.5. Embedded & IoT Devices

4.2. By Application (In Value %)

4.2.1. IT & ITeS

4.2.2. BFSI

4.2.3. Manufacturing & Industrial Automation

4.2.4. Education & EdTech

4.2.5. Government & Defense

4.3. By End-User (In Value %)

4.3.1. Enterprise

4.3.2. SMBs

4.3.3. Consumers

4.3.4. Government

4.3.5. OEMs & ODMs

4.4. By Distribution Channel (In Value %)

4.4.1. Online Retail

4.4.2. Offline Retail

4.4.3. Direct Sales

4.4.4. Value Added Resellers (VARs)

4.4.5. Distribution Networks

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. West

4.5.4. East

5. India Technology Hardware Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. HP India

5.1.2. Dell Technologies

5.1.3. Lenovo India

5.1.4. Acer India

5.1.5. ASUS India

5.1.6. HCL Infosystems

5.1.7. Samsung Electronics

5.1.8. Apple India

5.1.9. Cisco Systems

5.1.10. Xiaomi

5.1.11. Foxconn India

5.1.12. VVDN Technologies

5.1.13. Dixon Technologies

5.1.14. Wistron India

5.1.15. Bharat Electronics Ltd (BEL)

5.2. Cross Comparison Parameters

(Inception Year, Headquarters Location, Product Portfolio Breadth, Employee Strength India, R&D Spend %, PLI Participation, Manufacturing Facilities Presence, Market Share %)

5.3. Market Share Analysis (By Device Type, By Channel, By OEM)

5.4. Strategic Initiatives (Local Sourcing, Assembly Lines, Service Expansion)

5.5. Mergers and Acquisitions (Cross-Border and Domestic)

5.6. Investor Analysis (Private Equity & Corporate VC)

5.7. Venture Capital Funding (Hardware Startups & Deep Tech)

5.8. Government Grants (PLI, ESDM Scheme Beneficiaries)

5.9. Private Equity Investments (Buyouts, Expansion Rounds)

6. India Technology Hardware Market Regulatory Framework

6.1. Compliance & Import Regulations

6.2. BIS & E-Waste Regulations

6.3. Make in India Incentives

6.4. Localization Mandates for Strategic Sectors

7. India Technology Hardware Future Market Size (INR Cr & USD Mn)

7.1. Forecasted Market Size (Segment-wise CAGR, Growth Opportunities by Device Type)

7.2. Factors Driving Future Growth (Component Localization, IoT Penetration, Tier II/III City Growth)

8. India Technology Hardware Future Market Segmentation

8.1. By Device Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. India Technology Hardware Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (By Category & End-User)

9.2. Customer Cohort Analysis (Enterprise Segments, B2C Purchase Behavior)

9.3. Strategic Marketing Insights (Retail vs Online Growth Pathways)

9.4. White Space Opportunity Mapping (Component Manufacturing, Domestic R&D)

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India Technology Hardware Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the India Technology Hardware Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple hardware manufacturers and import/export officials to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive and validated analysis.

Frequently Asked Questions

01. How big is India Technology Hardware Market?

The India Technology Hardware market, valued at USD 22 billion, is driven by government-backed manufacturing programs, expansion of data infrastructure, and rising demand from education and enterprise sectors.

02. What are the challenges in India Technology Hardware Market?

India Technology Hardware Market Challenges include overreliance on semiconductor imports, lack of high-precision component production, and regulatory compliance costs affecting SMEs entry into the market.

03. Who are the major players in the India Technology Hardware Market?

Key players in the India Technology Hardware Market include Dixon Technologies, HP Inc., Dell Technologies, VVDN Technologies, and Acer India. Their dominance is attributed to strong production capacity, global supply chain integration, and PLI scheme alignment.

04. What are the growth drivers of India Technology Hardware Market?

Key growth drivers of India Technology Hardware Market include increased domestic electronics production, rising digital demand from enterprises, government digitization initiatives, and favorable incentive schemes under PLI 2.0.

05. What are the opportunities in India Technology Hardware Market?

India Technology Hardware Market opportunities lie in rural digitization, export-driven hardware manufacturing, localized data centers, and enterprise IT infrastructure expansion in Tier-2 and Tier-3 cities.

Why Buy From Us?

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.