India Women Wear Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD5976

December 2024

83

About the Report

India Women Wear Market Overview

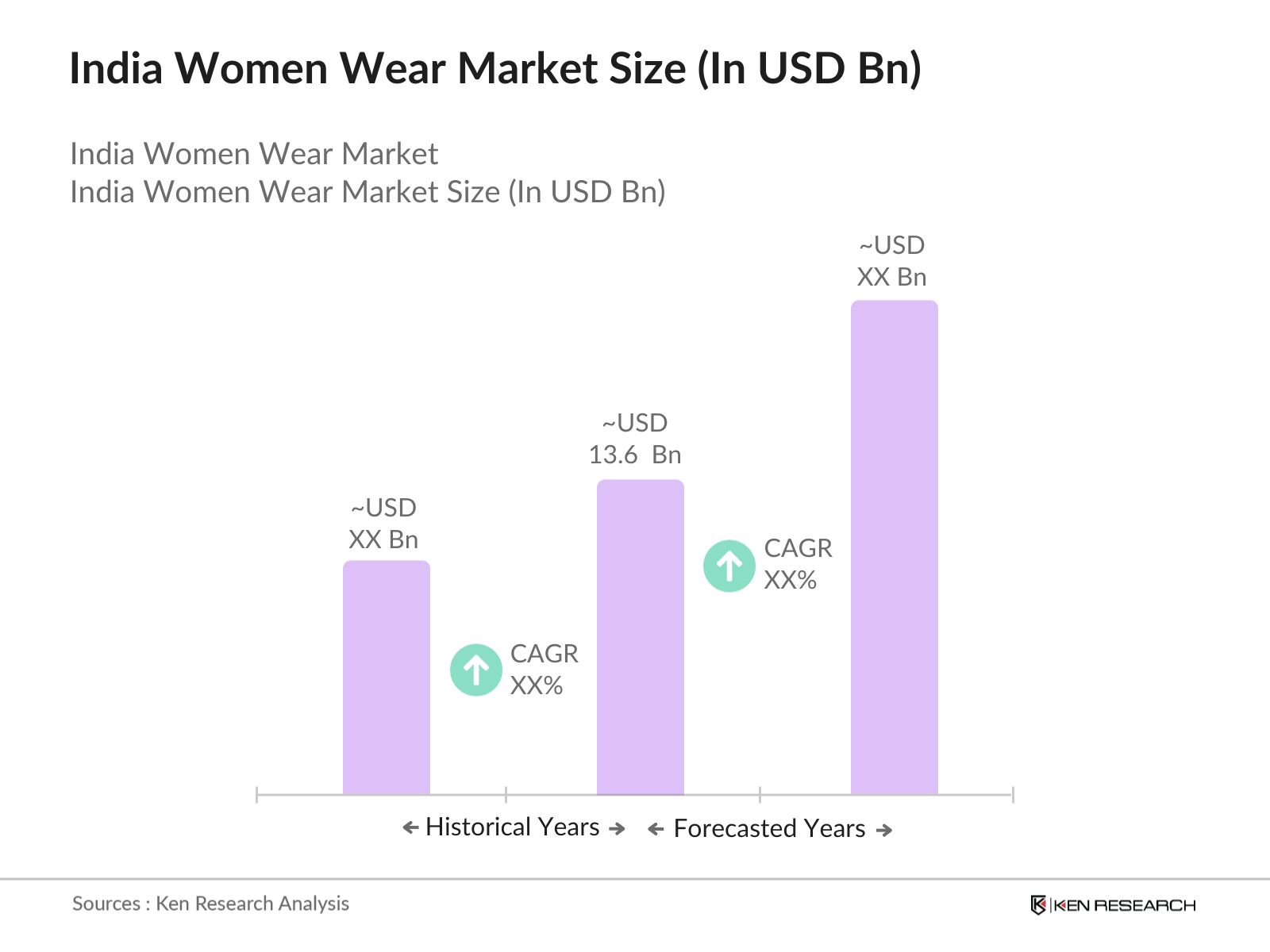

- The India women wear market is valued at USD 13.6 billion, based on a comprehensive five-year historical analysis. This market is driven by several key factors, including rising disposable incomes, increasing urbanization, and a growing awareness of fashion among the Indian female population. Additionally, the expanding middle class and growing e-commerce platforms have contributed to the increase in demand for womens wear across both urban and rural areas. The shift towards modern retail formats, such as online shopping and fast fashion, has also played a pivotal role in the markets rapid growth.

- In the India women wear market, the dominance of metropolitan cities like Mumbai, Delhi, and Bengaluru is attributed to their higher income levels, robust retail infrastructure, and greater exposure to global fashion trends. These cities serve as fashion hubs, where consumers demand a wider range of product offerings, from ethnic wear to western styles. Furthermore, Tier 2 and Tier 3 cities are increasingly becoming contributors to the market, as rising aspirations and enhanced purchasing power in these regions drive demand for branded women wear.

- The implementation of the Goods and Services Tax (GST) in 2017 impacted the apparel industry, including womens wear. The 12% GST rate applicable to garments priced above 1,000 affected consumer purchasing patterns. However, the Ministry of Finance reported in 2023 that tax collections from the apparel sector saw a year-on-year growth of 8%, indicating recovery and adaptation within the market, despite the initial challenges posed by GST.

India Women Wear Market Segmentation

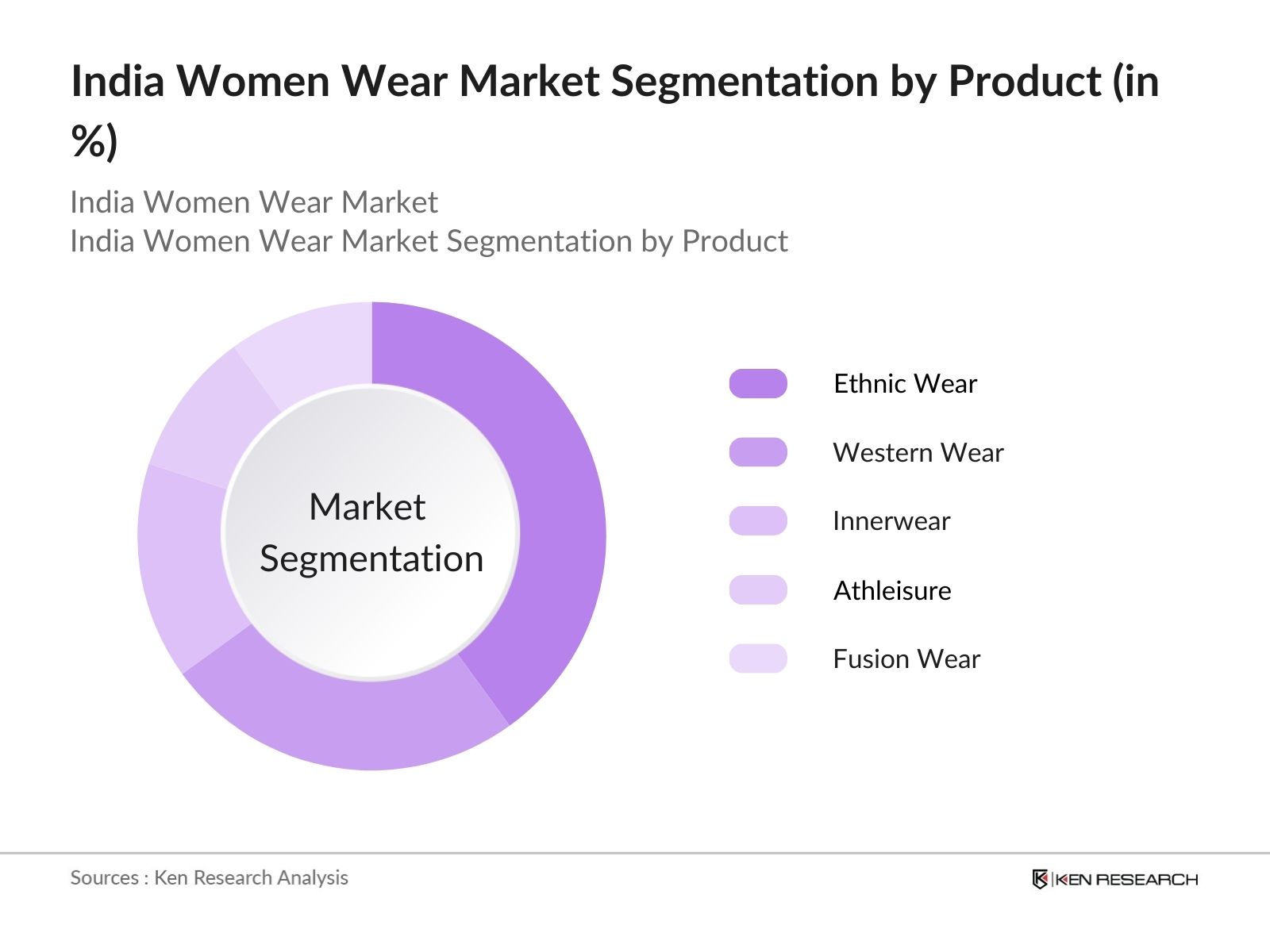

- By Product Type: The India women wear market is segmented by product type into ethnic wear, western wear, innerwear, athleisure, and fusion wear. Among these, ethnic wear has a dominant market share in India, mainly due to its cultural significance and widespread acceptance for both casual and festive occasions. Women in India continue to favour ethnic clothing for weddings, festivals, and other social gatherings, making this sub-segment a key player in the product type category. Additionally, ethnic wear brands such as Fabindia and Biba have developed a strong presence through their diversified offerings, blending traditional designs with contemporary fashion elements.

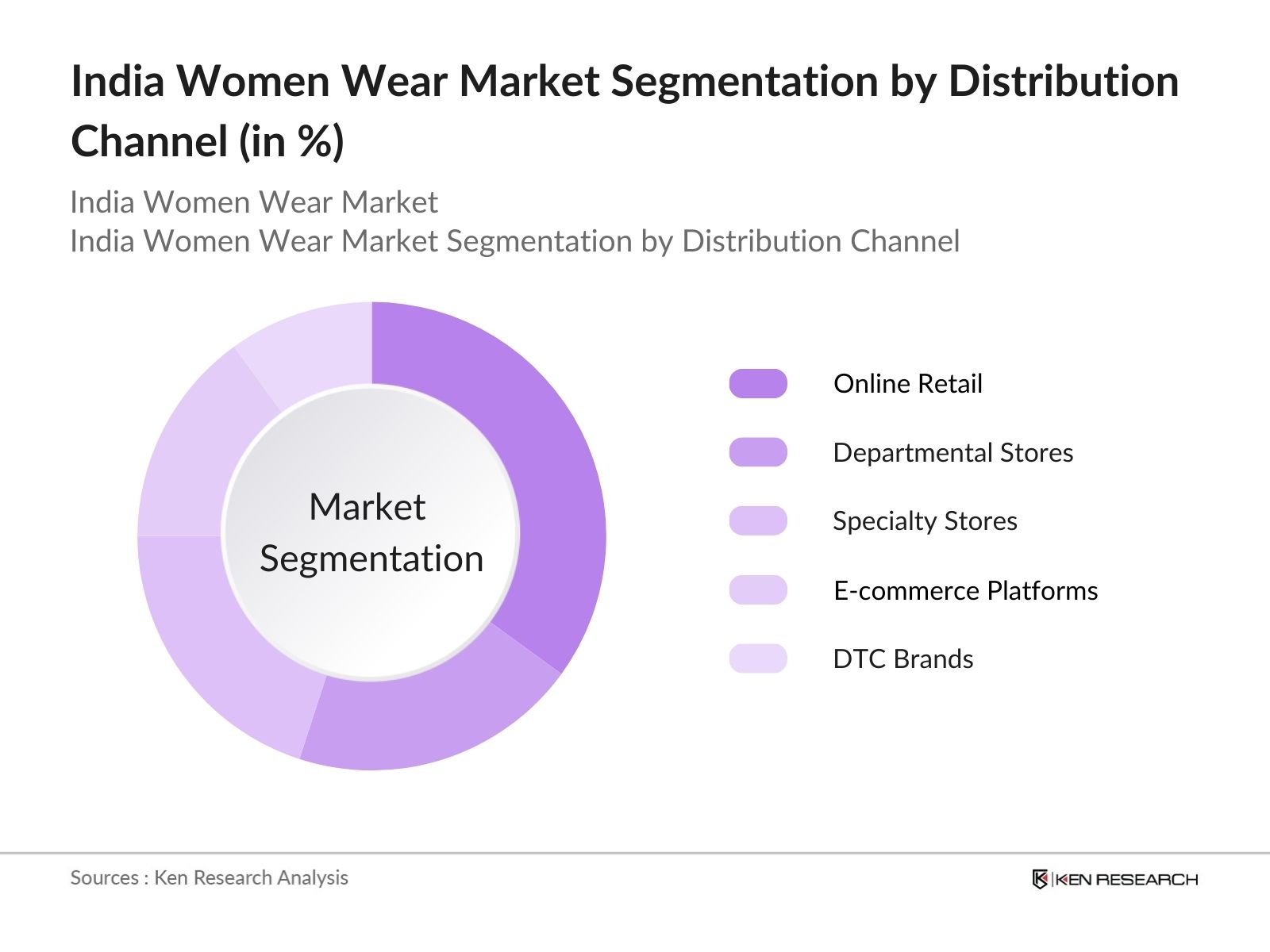

- By Distribution Channel: Indias women wear market is also segmented by distribution channels into online retail, departmental stores, specialty stores, e-commerce platforms, and direct-to-consumer (DTC) brands. Online retail has gained a market share in recent years, primarily driven by the convenience and wide variety of products available to consumers. The growth of online platforms like Myntra, Amazon, and Flipkart, coupled with the rising penetration of smartphones and the internet, has made online retail a dominant force in the market. Furthermore, online platforms offer attractive discounts, easy returns, and access to the latest fashion trends, making them a preferred shopping destination for women across different age groups.

India Women Wear Market Competitive Landscape

The India women wear market is dominated by both domestic and international brands. The competition is intense, with companies adopting strategies like expanding product portfolios, introducing sustainable fashion lines, and leveraging celebrity endorsements to strengthen their market position. Brands such as Aditya Birla Fashion and Retail Ltd, Reliance Retail, and Fabindia hold a share due to their extensive distribution networks and strong brand equity. International brands like Zara and H&M are also key players, benefiting from their fast fashion business models and premium brand positioning.

|

Company |

Establishment Year |

Headquarters |

Revenue (INR Cr) |

Retail Presence |

Online Penetration |

Sustainability Initiatives |

Collaborations |

Brand Equity |

|

Aditya Birla Fashion and Retail Ltd |

1997 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

Reliance Retail |

2006 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

Fabindia |

1960 |

New Delhi |

- |

- |

- |

- |

- |

- |

|

H&M India |

2015 |

Stockholm, Sweden |

- |

- |

- |

- |

- |

- |

|

Zara India |

2010 |

Spain |

- |

- |

- |

- |

- |

- |

India Women Wear Market Analysis

India Women Wear Market Growth Drivers

- Rising Disposable Income: India's per capita disposable income has seen a steady rise, contributing to the growth of the womens wear market. According to the Ministry of Statistics and Programme Implementation, the per capita income in India in 2023 stood at 172,000 ($2,077), up from 150,000 ($1,810) in 2021. This increase in disposable income has led to higher consumer spending on non-essential items such as fashion apparel. As more households move into the middle and upper-middle-class brackets, the demand for premium and branded women's clothing has surged, indicating a robust potential for market growth.

- Growing Fashion Awareness: Fashion awareness in India has increased due to globalization and easy access to digital platforms. A report from the Reserve Bank of India highlights that internet penetration in India reached 850 million users in 2023, making fashion trends from across the world accessible to a broader audience. Additionally, exposure to international brands and influencers through social media has contributed to the increasing adoption of global fashion trends by Indian women, especially in urban areas, further driving demand for womens wear in the country.

- Influence of Western Culture: The influence of Western culture on Indian fashion has accelerated the demand for womens western wear, such as dresses, skirts, and formal office attire. Data from the Indian Ministry of Commerce and Industry shows that the import of western fashion items surged by 15% in 2022, reflecting a growing consumer base for western-style clothing. This cultural shift, particularly among millennials and Gen Z, is helping boost demand for modern womens wear categories and is contributing to the market's expansion.

India Women Wear Market Challenges

- Fragmented Supply Chain: Indias textile and garment sector, including the womens wear market, is marked by a fragmented supply chain. A study by the Ministry of Textiles reveals that over 70% of garment manufacturers in India operate in the unorganized sector. This lack of cohesion leads to inefficiencies in production, longer lead times, and challenges in quality control. Small and medium-sized manufacturers often face difficulties in maintaining consistent supply and keeping up with fashion trends, which can hamper growth in the formal retail market.

- High Competition from Unorganized Sector: The unorganized sector holds a dominant position in the Indian apparel industry, accounting for nearly 85% of the total market share in 2023, according to the Ministry of Commerce. This presents a major challenge for branded and organized retailers in the womens wear market. Lower operational costs allow unorganized players to offer cheaper alternatives, which can undermine the growth potential of established brands that operate in the organized sector.

India Women Wear Market Future Outlook

Over the next five years, the India women wear market is expected to grow due to a combination of factors such as the increasing influence of social media, the rising trend of sustainable fashion, and continuous advancements in textile technologies. E-commerce will continue to drive growth, with Tier 2 and Tier 3 cities becoming the primary targets for retailers looking to expand their footprint. In addition, innovations in fabric technologies, such as the use of eco-friendly materials and smart textiles, will create new avenues for growth, especially in the athleisure and fusion wear segments.

India Women Wear Market Opportunities

- Growth in Online Platforms: Indias e-commerce market has seen a dramatic rise in users, with over 400 million online shoppers in 2023, according to the Telecom Regulatory Authority of India (TRAI). The growing number of women shoppers in the online space provides a lucrative opportunity for brands to expand their customer base. Online platforms offer access to tier-2 and tier-3 cities where physical retail is limited, enabling brands to reach a wider audience and cater to the rising demand for womens fashion.

- Expansion of Private Labels: Private label brands are gaining traction in Indias womens wear market. Major retailers such as Reliance and Tata are increasingly focusing on launching their in-house brands, which offer competitive pricing and exclusive designs. According to the Ministry of Corporate Affairs, private labels accounted for 12% of organized fashion retail sales in 2023. This expansion not only provides a cost-effective alternative for consumers but also allows retailers to exercise greater control over their supply chains and profit margins.

Scope of the Report

|

Product Type |

Ethnic Wear Western Wear Innerwear Athleisure Fusion Wear |

|

Distribution Channel |

Online Retail Departmental Stores Specialty Stores E-commerce Platforms DTC Brands |

|

Fabric Type |

Cotton Silk Denim Synthetic Blended Fabrics |

|

Age Group |

Teens Adults Middle-Aged Seniors |

|

Region |

North India South India West India East India |

Products

Key Target Audience

Retail Chains

Apparel Manufacturers

Textile Suppliers

Fashion Designers and Boutiques

E-commerce Platforms

Banks and Financial Institutions

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Textiles, Fashion Design Council of India)

Logistics and Distribution Companies

Companies

Players Mentioned in Report

Aditya Birla Fashion and Retail Ltd

Reliance Retail

Fabindia

H&M India

Zara India

Shoppers Stop

W for Women

Biba Apparels

Pantaloons

Global Desi

Table of Contents

1. India Women Wear Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Women Wear Market Size (In INR Cr)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Women Wear Market Analysis

3.1. Growth Drivers

3.1.1. Rising Disposable Income

3.1.2. Growing Fashion Awareness

3.1.3. Influence of Western Culture

3.1.4. Increase in E-Commerce Penetration

3.2. Market Challenges

3.2.1. Fragmented Supply Chain

3.2.2. High Competition from Unorganized Sector

3.2.3. Rising Input Costs (Fabric, Labor)

3.2.4. Changing Consumer Preferences

3.3. Opportunities

3.3.1. Growth in Online Platforms

3.3.2. Expansion of Private Labels

3.3.3. Collaboration with Fashion Designers

3.3.4. Focus on Sustainable Fashion

3.4. Trends

3.4.1. Increased Demand for Athleisure

3.4.2. Adoption of Indian Ethnic Fusion Wear

3.4.3. Growth in Plus-Size Clothing

3.4.4. Rise in Use of Eco-friendly Materials

3.5. Government Regulations

3.5.1. Textile Policy Regulations

3.5.2. FDI Policies in Fashion Retail

3.5.3. Goods and Services Tax (GST) Impact

3.5.4. Incentives for Local Manufacturing

3.6. SWOT Analysis

3.7. Value Chain Analysis

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. India Women Wear Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Ethnic Wear

4.1.2. Western Wear

4.1.3. Innerwear

4.1.4. Athleisure

4.1.5. Fusion Wear

4.2. By Distribution Channel (In Value %)

4.2.1. Online Retail

4.2.2. Departmental Stores

4.2.3. Specialty Stores

4.2.4. E-commerce Platforms

4.2.5. Direct to Consumer (DTC) Brands

4.3. By Fabric Type (In Value %)

4.3.1. Cotton

4.3.2. Silk

4.3.3. Denim

4.3.4. Synthetic

4.3.5. Blended Fabrics

4.4. By Age Group (In Value %)

4.4.1. Teens

4.4.2. Adults

4.4.3. Middle-Aged

4.4.4. Seniors

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. West India

4.5.4. East India

5. India Women Wear Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Aditya Birla Fashion and Retail Ltd

5.1.2. Reliance Retail

5.1.3. Fabindia

5.1.4. Shoppers Stop

5.1.5. H&M India

5.1.6. Pantaloons

5.1.7. Biba Apparels

5.1.8. Zara India

5.1.9. W for Women

5.1.10. Global Desi

5.1.11. Marks & Spencer

5.1.12. Ritu Kumar

5.1.13. AND Designs India Ltd

5.1.14. Uniqlo India

5.1.15. Levi's India

5.2. Cross Comparison Parameters (Revenue, Retail Presence, Online Penetration, Product Range, Price Positioning, Sustainability Initiatives, Collaborations, Brand Equity)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. India Women Wear Market Regulatory Framework

6.1. Textile and Apparel Manufacturing Regulations

6.2. Environmental Compliance for Textiles

6.3. Certification Processes (e.g., Organic, Sustainable Clothing)

6.4. Import and Export Regulations

7. India Women Wear Future Market Size (In INR Cr)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Women Wear Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Fabric Type (In Value %)

8.4. By Age Group (In Value %)

8.5. By Region (In Value %)

9. India Women Wear Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior Insights

9.3. Go-to-Market Strategy

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In the initial phase, we conducted a thorough review of the India women wear market's value chain. This process involved gathering data from both primary and secondary sources, including government publications, industry reports, and proprietary databases. The key variables identified include consumer preferences, distribution channels, and market competition.

Step 2: Market Analysis and Construction

The next step focused on analyzing historical data related to market penetration, the ratio of retail outlets to online sales, and overall revenue generation. This phase was crucial in understanding the past market behavior and setting the foundation for accurate future projections.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses were developed based on the initial analysis and were validated through consultations with industry experts via phone interviews. These insights were critical in refining the market forecasts and validating the key growth drivers identified in the earlier stages.

Step 4: Research Synthesis and Final Output

Finally, a detailed synthesis of the data was performed, which included consultations with women wear manufacturers and retailers. This ensured the final output was accurate and reflective of real-time market conditions, making it a reliable resource for business professionals.

Frequently Asked Questions

How big is India Women Wear Market?

The India women wear market is valued at USD 13.6 billion, driven by the rising demand for ethnic and western wear among Indian women. This growth is further supported by increasing disposable incomes and a burgeoning middle class.

What are the challenges in India Women Wear Market?

Key challenges in the India women wear market include high competition from unorganized players, fluctuating raw material prices, and the rising costs of labor and manufacturing. Moreover, evolving consumer preferences demand quick adaptation by brands.

Who are the major players in the India Women Wear Market?

Prominent players in the India women wear market include Aditya Birla Fashion and Retail Ltd, Reliance Retail, Fabindia, H&M India, and Zara India. These companies dominate the market due to their extensive distribution networks and strong brand presence.

What are the growth drivers of India Women Wear Market?

The India women wear market is primarily driven by factors such as the rise of online shopping, increasing disposable incomes, and the influence of social media on fashion trends. Additionally, the demand for ethnic fusion wear is on the rise.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.