UAE Furniture Market Outlook to 2029

Region:Middle East

Author(s):Kartik and Nishika

Product Code:KR1489

April 2025

80-100

About the Report

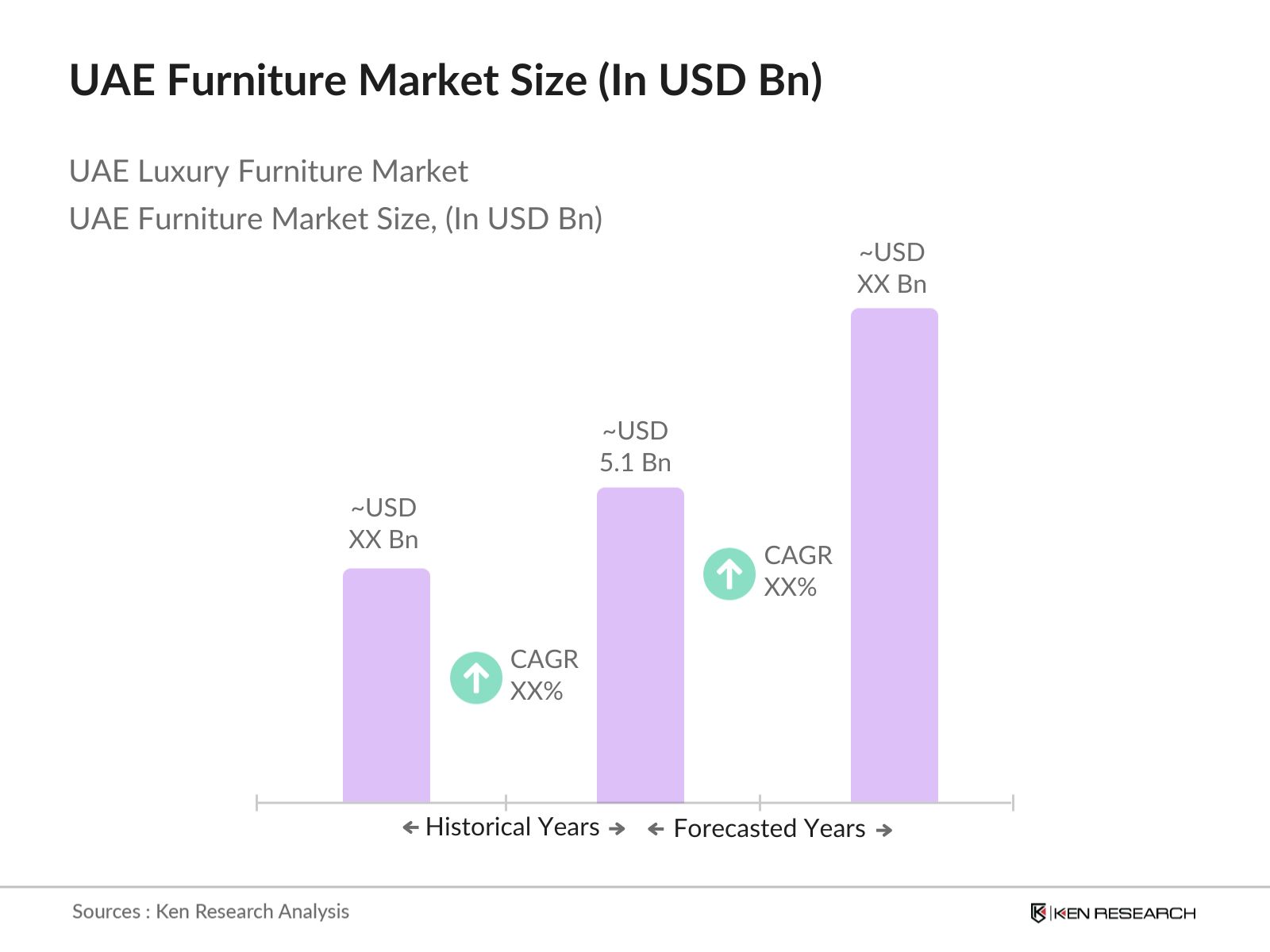

UAE Furniture Market Overview

The UAE Furniture Market is valued at USD 5.1 billion, based on a five-year historical analysis. The market has grown steadily due to the countrys thriving real estate sector, increasing urban density, and the dominance of expatriate consumers. The volume reached 4.3 million units, driven by consumer preference for premium and customized furniture options. Urbanization and continuous demand from the residential and hospitality sectors have supported stable price points and consistent procurement, reflecting resilience in both value and volume metrics.

Dubai remains the dominant city in the UAE Furniture Market due to its high real estate investment value and dense urban population. With a real estate value of AED 112 billion, Dubai offers abundant commercial and residential furnishing opportunities. Its extensive office supply (11.6 million sqm) and retail presence fuel furniture demand from both B2B and B2C clients. Cities like Abu Dhabi and Sharjah also contribute, but Dubai's development pace and affluent population make it the epicenter for furniture consumption.

The UAE government has allocated AED 30 billion through the Ministry of Industry and Advanced Technology to drive self-reliance in strategic sectors. Ajman and Ras Al Khaimah are designated furniture manufacturing hubs. Tariff exemptions on imported machinery and raw materials further incentivize domestic production across the furniture value chain.

UAE Furniture Market Segmentation

By End-User: The UAE Furniture Market is segmented by end user into Residential, Commercial, Hospitality, Retail, and Others. Recently, the Residential segment has a dominant market share in the UAE under the end user segmentation. This is due to the rapid expansion of real estate projects and increasing homeownership among expatriates. Residential furniture demand remains strong for beds, sofas, dining sets, and kitchen fixtures, with consistent project launches fueling continuous procurement cycles.

By Material Type: The UAE Furniture Market is segmented by material type into Wood, Metal, Plastic, Glass, and Others. Recently, the Wood segment has a dominant market share in the UAE under the material type segmentation. The dominance of wood is attributed to its suitability for both traditional and contemporary furniture needs, especially in homes and hospitality properties. Additionally, woods aesthetic versatility and consumer preference for quality furnishings support its continued leadership.

UAE Furniture Market Competitive Landscape

UAE Furniture Market Competitive Landscape

The UAE Furniture Market is highly fragmented, with top players contributing approximately 20% of the total revenue. The market features a mix of global brands and local manufacturers, with IKEA, Home Centre, and PAN Home leading in omnichannel presence and product variety. While digital-first players like Western Furniture are gaining momentum, offline majors such as Home Centre and PAN Home still maintain dominance in physical store presence. The shift towards integrated omnichannel strategies has been observed across top players post-COVID-19.

UAE Furniture Market Analysis

Growth Drivers

Real Estate Expansion and Procurement Demand: Dubai recorded over AED 528 billion in real estate transaction volume, with large-scale residential and commercial developments boosting furniture demand. As urban expansion continues in Dubai, Abu Dhabi, and Sharjah, developers rely heavily on bulk furniture procurement for furnishing apartments, villas, and hotel units, driving sustained demand across custom furniture formats.

Expatriate Influence on Consumption: The UAE is home to over 8.8 million expatriates, with significant residential mobility. In Dubai alone, housing demand annually exceeds 45,000 units, driven by rental churn. This fuels continuous furniture repurchasing cycles, especially for affordable, ready-to-assemble, and modular furniture for leased or shared accommodations preferred by expat populations.

Hospitality Sector Expansion and Procurement Pipelines: Dubai welcomed 14.3 million tourists while Abu Dhabi clocked 24.2 million guest nights, sustaining procurement of high-end furnishings in the hospitality segment. Hotels and resorts invest in beds, sofas, and lobbies to align with global design trends, creating a recurring demand base for durable and aesthetic furniture solutions.

Market Challenges

Import Dependence and Supply Chain Disruptions: Over 70% of the UAEs furniture inputs are imported, exposing the market to risks such as global shipping delays and foreign exchange volatility. In 2023, UAE Customs reported that 25% of B2B furniture deliveries faced disruption due to raw material delays, particularly in sourcing wood, metal, and upholstery textiles.

Changing Consumer Expectations: UAE Customs data showed 3.5 million units of furniture were imported in 2023, reflecting consumer preference for international designs and frequent updates. Local manufacturers face challenges meeting trend-driven demand, with mid-tier players struggling to retain customers amid brand-switching behaviors and pressure to continuously innovate in design.

UAE Furniture Market Future Outlook

Over the next five years, the UAE Furniture Market is expected to sustain its upward growth momentum, driven by rising investments in residential and commercial infrastructure, the expansion of phygital retail, and increasing consumer demand for personalized furniture solutions. Real estate development in Sharjah and Ajman will open new regional growth opportunities. Strategic shifts toward e-commerce and local manufacturing will further enhance the markets resilience and accessibility.

Market Opportunities

Ajmans Production Base & Industrial Incentives: Ajman contributes over 60% of UAEs domestic furniture output, supported by the Ministry of Industry and Advanced Technologys industrial stimulus. Under Operation 300bn, SMEs receive land grants and financing support to enhance local production, presenting an opportunity for import substitution and export-ready manufacturing scale-up.

Sharjahs Commercial Project Pipeline: Sharjah has over 6 million square meters of mixed-use construction approved post-2029, with a projected residential addition of 100,000+ inhabitants. This expansion creates a strong demand base for institutional and retail furniture. Early engagement in B2B contracts with developers positions players to capitalize on long-term project furnishing needs.

Scope of the Report

|

End User |

Residential |

|

Material Type |

Wood |

|

Business Type |

B2B |

|

Distribution Channel |

Offline |

|

Region |

Dubai |

Products

Key Target Audience

- Real Estate Developers (Dubai Land Department, Sharjah Real Estate Registration Dept.)

- Interior Designers and Project Contractors

- B2B Furniture Procurement Teams (Corporate Buyers)

- B2C Retail Chains and Showroom Managers

- Investments and Venture Capitalist Firms

- Hospitality Industry Chains (e.g., EMAAR Hospitality, Jumeirah Group)

- Government and Regulatory Bodies (Ministry of Economy, UAE Ministry of Industry and Advanced Technology)

- Online Home Dcor and E-Commerce Startups

Companies

Players Mentioned in the Report

- IKEA Al-Futtaim

- Home Centre

- PAN Home

- Royal Furniture

- Danube Home

Table of Contents

1. Executive Summary

1.1. Market Snapshot and Ecosystem Overview

1.2. UAE Furniture Market Revenue and Volume Highlights (In USD Mn and Mn Units)

1.3. Competitive Structure and Fragmentation Overview

1.4. Real Estate Linkage and Demand Centers

1.5. Key Product Categories and Consumer Segments

2. UAE Furniture Market Overview

2.1. Definition and Scope of Furniture Market in UAE

2.2. Product Taxonomy and Category Classification

2.3. Market Segmentation Structure (End Use, Region, Material, Channel, Business Type)

2.4. GCC and UAE Macroeconomic Indicators (Urban Population %, Real Estate Value, Retail Supply)

2.5. Demand Linkages with Hospitality, Real Estate, and Interior Design Sectors

2.6. Timeline of Major Furniture Players' Expansion in UAE

3. UAE Furniture Market Size (In USD Mn & Mn Units)

3.1. Historical Market Size and Volume Analysis

3.2. Average Price Trend per Unit (USD)

3.3. Year-On-Year Sales Fluctuation and Economic Linkages

3.4. Market Size Evolution Residential, Commercial, Hospitality, Retail

3.5. Offline vs Online Furniture Sales Split

3.6. Market Density by Emirate Dubai, Abu Dhabi, Sharjah, Ajman, Others

4. UAE Furniture Market Analysis

4.1. Growth Drivers

4.1.1. Rise in Urbanization and Expat Influx

4.1.2. Real Estate Pipeline and Interior Design Contracts

4.1.3. Government Infrastructure and Hospitality Projects

4.2. Market Challenges

4.2.1. Timber Price Fluctuation & Import Dependency

4.2.2. Low Automation Among Local Manufacturers

4.3. Market Opportunities

4.3.1. Phygital Retail and Online Penetration Expansion

4.3.2. Interior Design Integration & B2B Customization Surge

4.4. Market Trends

4.4.1. Forward Integration Across Distribution Channels

4.4.2. Bespoke Product Demand Among HNWIs

4.4.3. Manufacturing Shift Toward Ajman and Ras Al Khaimah

4.5. Regulatory Environment

4.5.1. UAE Cabinet Decision on Luxury Goods Tariff

4.5.2. Ajman Free Zone Policies for Furniture Manufacturing

4.5.3. UAE Green Building Regulations for Sustainable Furniture

5. UAE Furniture Market Segmentation (In Value %, Units & Revenue Mn)

5.1. By End User (Residential, Commercial, Hospitality, Retail, Others)

5.2. By Material Type (Wood, Metal, Plastic, Glass, Others)

5.3. By Business Type (B2B, B2C)

5.4. By Distribution Channel (Offline, Online)

5.5. By Region (Dubai, Abu Dhabi, Sharjah, Ajman, Others)

6. Competitive Landscape

6.1. Market Share Analysis of Key Players (Top 10)

6.2. Omni Channel Positioning Matrix (Retail Presence vs Online Visibility)

6.3. Strategic Expansion Timelines Flagship Showrooms, Online Portals, Factory Setups

6.4. Cross Comparison Parameters (Inception Year, Factory Location, No. of Stores, Online Rank, Flagship Showroom Sq. Ft., B2B Partnerships, Local Manufacturing Status, Customization Capability)

7. Company Profiles (15 Major Players)

7.1. IKEA Al-Futtaim

7.2. Home Centre

7.3. PAN Home

7.4. Home Box

7.5. HomeRUs

7.6. Danube Home

7.7. Marina Home

7.8. Royal Furniture

7.9. Pottery Barn

7.10. United Furniture

7.11. Western Furniture

7.12. Royal Rest

7.13. VLite Furniture

7.14. Lucky Furniture

7.15. Highmoon Office Furniture

8. Construction Sector Linkage (Market Opportunity Mapping)

8.1. Construction Market Size (Residential, Hospitality, Office)

8.2. Mega Real Estate Projects by Emirate

8.3. Real Estate Value Chain Mapping Developer to Interior to Furniture Flow

8.4. Timeline of New Project Deliveries

9. UAE Furniture Future Market Size (In USD Mn and Units)

9.1. Volume and Value Forecasts by Segment

9.2. Demand Estimates End User Segments

9.3. Long-Term Trends: EV Mobility, Luxury Living, AI-Powered Interiors

10. UAE Furniture Market Future Segmentation

10.1. Future Split by End User (Residential, Commercial)

10.2. Future Segmentation by Distribution Channel (Online vs Offline)

10.3. Regional Penetration Projections (Sharjah, Ajman, Ras Al Khaimah)

10.4. Business Type Evolution B2B Orders from Real Estate Developers

11. Analyst Recommendations

11.1. Growth Strategy Roadmap (Phase-Wise Expansion: Digital, Retail, Factory)

11.2. Regional Focus Strategy (Dubai, Abu Dhabi, Sharjah, Ajman)

11.3. Product and Material Optimization Recommendations

11.4. Pricing Strategy Across Material Types

11.5. Tech and CRM Adoption Strategy for B2B Clients

12. Appendix

12.1. UAE Furniture Import Analysis by HS Code

12.2. Logistics and Cost Benchmarking for Imports

12.3. UAE Furniture E-Commerce Drivers and Consumer Metrics

Disclamer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This stage involved ecosystem mapping across manufacturers, retailers, and developers. Variables such as showroom size, online ranking, and end user customization levels were identified through proprietary databases and secondary sources.

Step 2: Market Analysis and Construction

The market was evaluated based on past five-year trends in price, unit volume, and channel-specific sales behavior. Residential and hospitality real estate expansion and showroom footprint were used as base factors to construct segment-wise revenue distribution.

Step 3: Hypothesis Validation and Expert Consultation

Through CATI with 15+ retail chain managers and B2B buyers across Ajman, Dubai, and Sharjah, data hypotheses around channel mix, demand variance, and procurement cycles were validated for accuracy.

Step 4: Research Synthesis and Final Output

This phase involved triangulation using brand interviews, import data, and showroom sales trends. Companies such as PAN Home and Royal Furniture provided insights into material sourcing, custom orders, and showroom conversion, finalizing the validated market structure.

Frequently Asked Questions

01. How big is the UAE Furniture Market?

The UAE Furniture Market was valued at USD 5.1 billion, supported by strong residential demand, local manufacturing in Ajman, and retail expansion in metro cities like Dubai and Abu Dhabi.

02. What are the challenges in the UAE Furniture Market?

Challenges in UAE Furniture Market include fluctuating timber prices, high import dependence with tariffs on luxury goods, and supply disruptions affecting local production timelines and inventory control.

03. Who are the major players in the UAE Furniture Market?

UAE Furniture Market Key players include IKEA Al-Futtaim, Home Centre, PAN Home, Royal Furniture, and Danube Home, supported by regional players like Pottery Barn, Homes R Us, and Western Furniture.

04. What are the growth drivers of the UAE Furniture Market?

In UAE Furniture Market Growth is driven by real estate expansion in Dubai and Sharjah, increased focus on omnichannel retail, high online engagement in metro areas, and rising demand for bespoke interior projects.

05. What are the trends reshaping the UAE Furniture Market?

Key trends include in UAE Furniture Market are rise of phygital showrooms, integration of AR/VR in furniture buying, and consumer demand for locally manufactured custom furniture solutions in urban emirates.

06. What future opportunities exist in the UAE Furniture Market?

In UAE Furniture Market Opportunities lie in manufacturing expansion in Ajman, deeper penetration of e-commerce into tier-2 cities, and a focus on contract furnishing for hospitality and commercial projects.

Why Buy From Us?

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.