USA Hospital Facilities Market Outlook to 2030

Region:North America

Author(s):Shubham Kashyap

Product Code:KROD2763

November 2024

88

About the Report

USA Hospital Facilities Market Overview

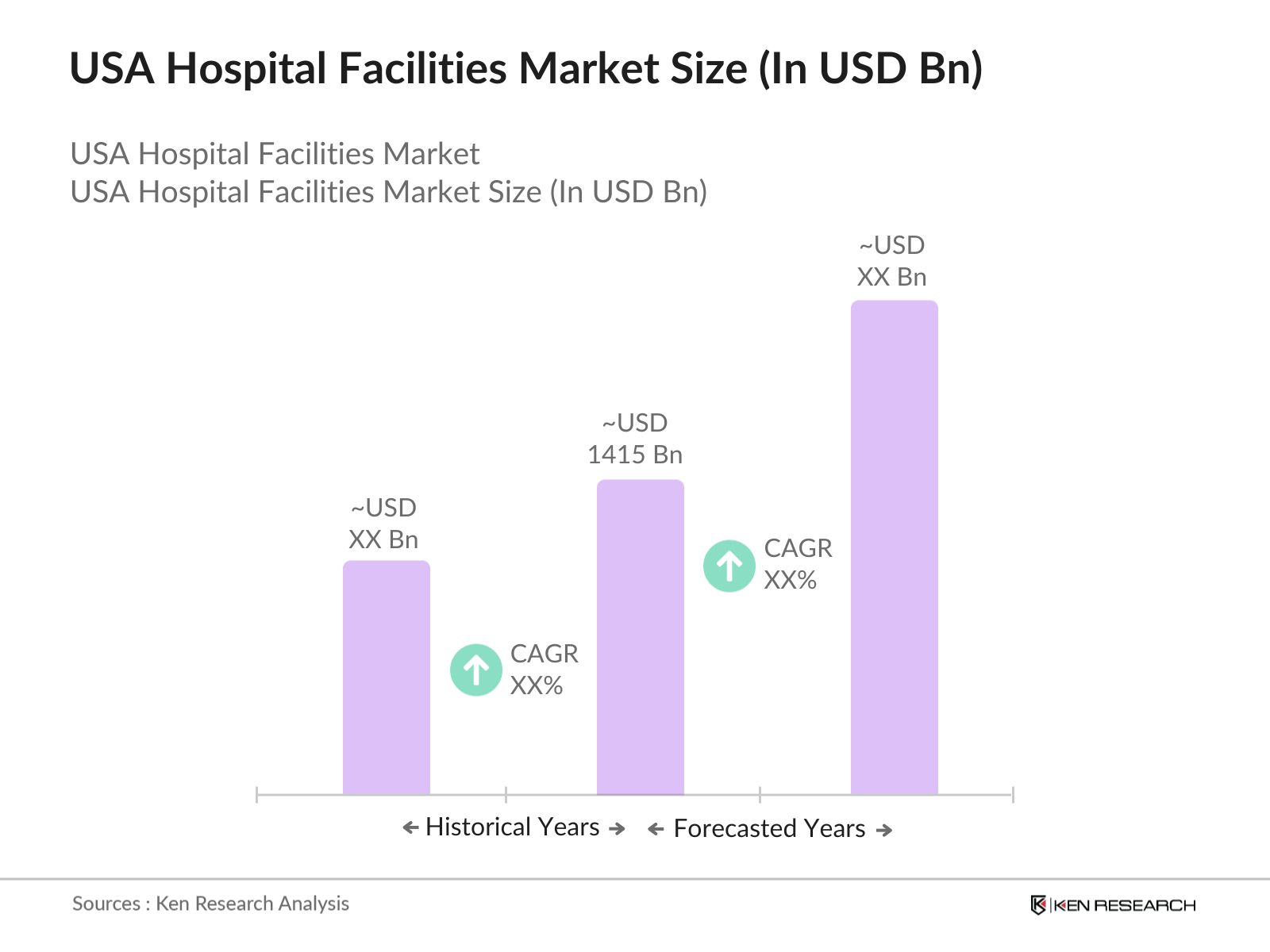

- Based on a five-year historical analysis, the USA Hospital Facilities market is valued at USD 1415 billion, supported by large investments in healthcare infrastructure, technology, and patient care services. The market is experiencing a substantial growth trajectory, driven by the increasing demand for healthcare services, particularly in response to an aging population and the rising prevalence of chronic diseases.

- Major cities such as New York, Los Angeles, and Houston are leading the expansion in this market due to the presence of large healthcare networks, advanced medical research centers, and high patient demand. In addition, rural areas are seeing growing investments in hospital facilities as part of government initiatives to improve healthcare accessibility across the country.

- The U.S. Department of Health and Human Services (HHS) has established strict regulatory guidelines to ensure the safety, quality, and efficiency of healthcare services in hospital facilities. In 2023, HHS introduced new regulations aimed at improving patient safety and streamlining hospital operations. These guidelines include increased oversight of electronic health records (EHR) systems, patient care technologies, and facility management protocols.

USA Hospital Facilities Market Segmentation

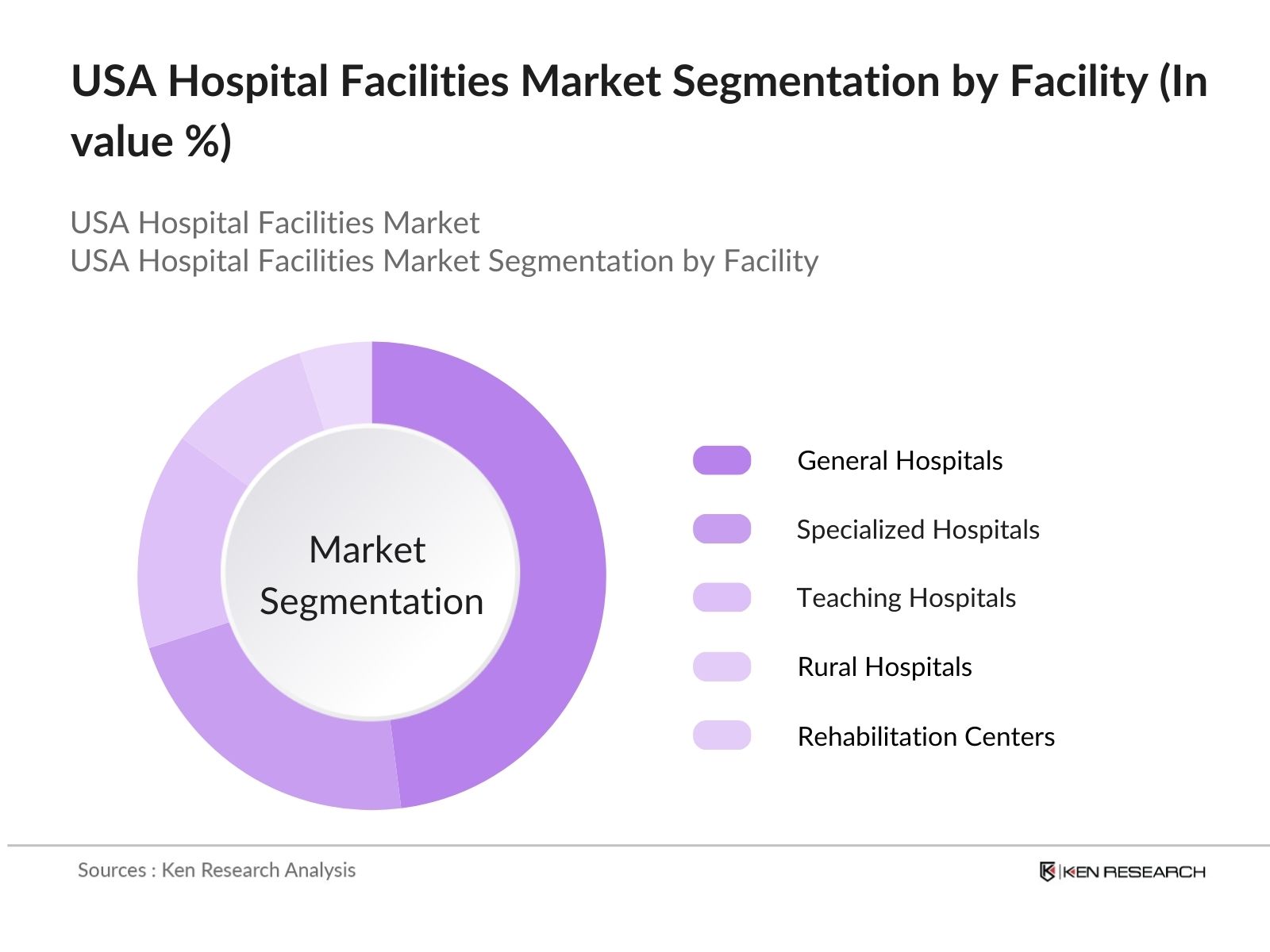

- By Type of Facility: The market is segmented by type of facility into general hospitals, specialized hospitals, teaching hospitals, rural hospitals, and rehabilitation centers. General hospitals dominate this segment due to their broad spectrum of services, ranging from emergency care to specialized treatments. Their wide availability across urban and rural regions, combined with their ability to cater to diverse patient needs, contributes to their market dominance. Moreover, general hospitals are often the first point of contact for healthcare, leading to increased patient volume and resource allocation. Major hospital networks such as HCA Healthcare and Ascension have focused on expanding general hospitals to cater to a growing population.

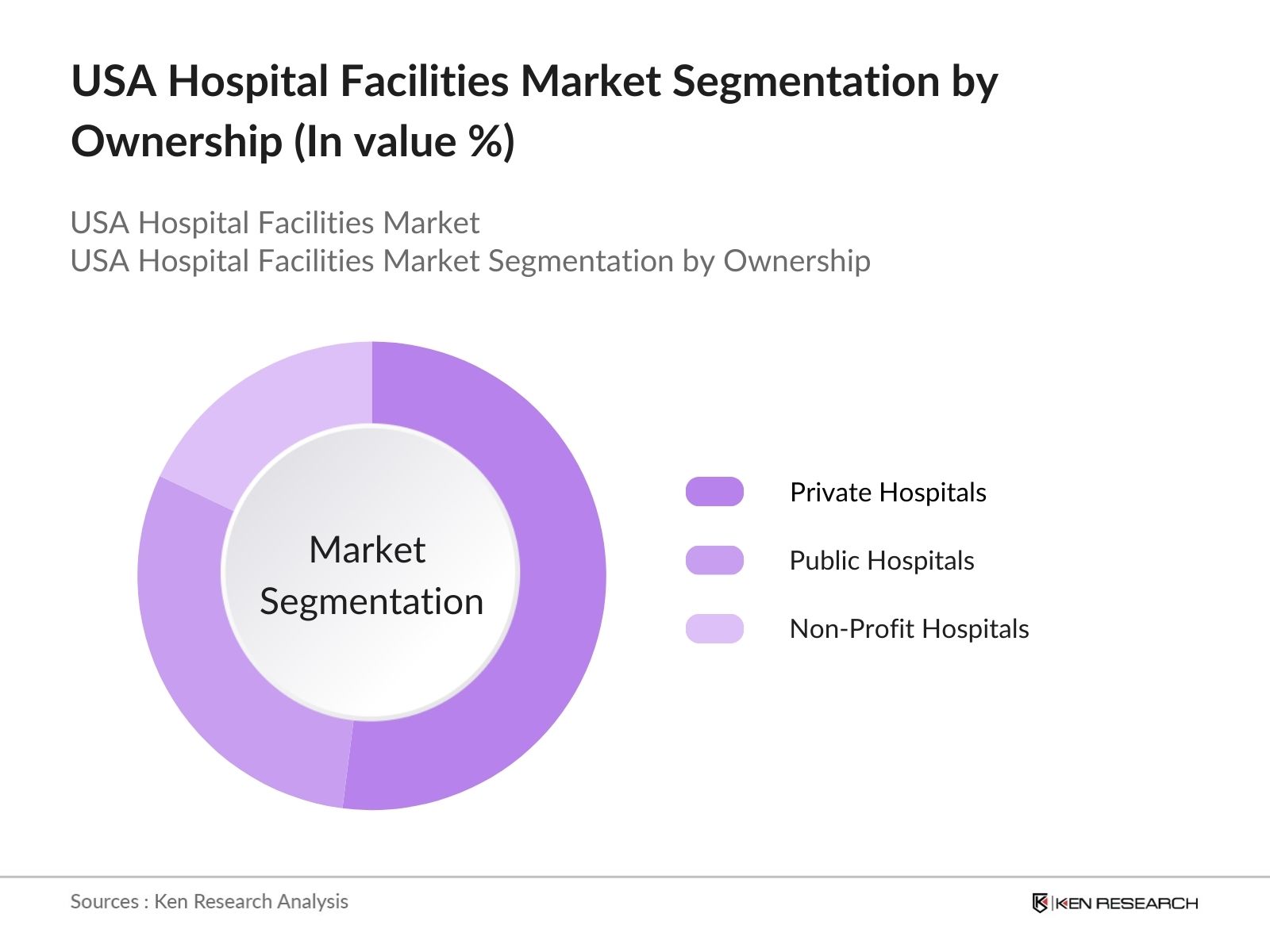

- By Ownership: The market is segmented by ownership into public hospitals, private hospitals, and non-profit hospitals. Private hospitals lead the ownership segment, primarily due to their access to higher investments, cutting-edge medical technology, and superior patient care services. These facilities often focus on advanced healthcare services and offer a more tailored patient experience. The flexibility in operation and management that private hospitals enjoy also allows them to rapidly adopt new medical technologies, contributing to their dominance in this market.

USA Hospital Facilities Market Competitive Landscape

The USA Hospital Facilities market is highly competitive, with several key players constantly innovating and expanding their hospital networks. Major players include HCA Healthcare, Ascension, and Tenet Healthcare, all of which are involved in large-scale healthcare service provision across the country. These companies are actively investing in modernizing hospital facilities, incorporating advanced medical technologies, and expanding their geographic footprint.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD) |

Key Services |

R&D Investments |

Geographical Reach |

Technology Adoption |

Partnerships |

|

HCA Healthcare |

1968 |

Nashville, TN |

|||||||

|

Ascension |

1999 |

St. Louis, MO |

|||||||

|

Tenet Healthcare |

1967 |

Dallas, TX |

|||||||

|

Mayo Clinic |

1889 |

Rochester, MN |

|||||||

|

Cleveland Clinic |

1921 |

Cleveland, OH |

USA Hospital Facilities Industry Analysis

Growth Drivers

- Expansion in Healthcare Infrastructure : The U.S. government continues to heavily invest in healthcare infrastructure. In 2023, federal healthcare spending exceeded USD 1.3 trillion, including significant allocations toward hospital infrastructure upgrades. This is supported by initiatives like the Hospital Preparedness Program (HPP), which provided $285 million for infrastructure in 2022. Private sector investments are also rising, with USA healthcare sales and financing volume for 2023 reaching 1.1 billion in 2023. The trend indicates continued infrastructure growth to meet rising demand for advanced care facilities. This investment is critical in expanding rural and underserved regions.

- Aging Population Impact on Healthcare Demand: The aging U.S. population, particularly those aged 65 and older, will reach 62 million in 2024, driving the need for senior care facilities and chronic disease management centers. The National Institute on Aging reports that 80% of seniors have at least one chronic condition, which intensifies hospital demand. The U.S. Census Bureau estimates that the elderly population will grow by 3 million by 2025, increasing healthcare facility pressure. Hospitals are responding by expanding geriatric care, with over prominent number of new hospital construction projects focused on elderly care by 2024.

- Technological Advancements AI in Healthcare: AI and robotics in healthcare have revolutionized patient care. By 2024, majority of U.S. hospitals have integrated AI systems for diagnostics, with leading institutions performing thousands of robotic surgeries annually. The telemedicine market has rapidly grown, with more than 40% of U.S. hospitals now offering remote patient monitoring. According to the Centers for Medicare and Medicaid Services (CMS), millions telehealth visits were conducted in 2023, a significant increase from pre-pandemic levels, signaling strong growth in digital health adoption.

Market Challenges

- High Operational and Maintenance Costs: U.S. hospitals face escalating operational costs, with labor costs accounting for a portion of expenditures. Registered nurses, specialists, and administrative staff salaries continue to rise, putting financial pressure on hospital operations. Additionally, hospitals invest heavily in new technologies to comply with regulatory requirements, such as the adoption of Electronic Health Records (EHR) and patient safety systems. Meeting safety and care standards, along with regulatory compliance, further increases operational costs, particularly as healthcare regulations become more stringent across federal and state levels.

- Regulatory and Policy Barriers: The complex landscape of healthcare regulations, including federal mandates and state-specific policies, presents challenges for hospitals. Compliance with healthcare reforms like the Affordable Care Act (ACA) requires hospitals to navigate numerous provisions, often leading to operational inefficiencies. Additionally, state-level Medicaid expansion policies differ widely, creating a fragmented regulatory environment that complicates nationwide hospital operations. Healthcare reforms and policies continue to impact hospital efficiency, as varying state and federal requirements often conflict, making it challenging to streamline operations across different regions.

USA Hospital Facilities Market Future Outlook

The USA Hospital Facilities market is expected to witness substantial growth over the next five years, driven by continuous investments in healthcare infrastructure, technological innovations, and the rising demand for hospital services. The integration of AI and robotic systems into hospital operations is expected to enhance patient care and operational efficiency, creating new growth opportunities.

Future Market Opportunities

- Integration of Digital Health Solutions: By 2024, more than majority of U.S. hospitals have adopted Electronic Health Records (EHR), with government programs such as the HITECH Act incentivizing over USD 35 billion in EHR implementation since 2022. Additionally, IoT (Internet of Things) is transforming hospital operations, with millions connected medical devices in use. Investments in hospital cybersecurity have also surged, with a substantial amount spent in 2023 on data security and protecting patient information against breaches.

- Expansion of Private Healthcare Networks: In 2023, over 100 mergers and acquisitions occurred in the U.S. healthcare sector, amounting to investments exceeding USD 7.5 billion. Large hospital networks, such as HCA Healthcare and Ascension Health, expanded their footprint, acquiring smaller facilities to improve operational efficiencies and patient services. These strategic partnerships allow hospitals to share resources and improve service quality.

Scope of the Report

|

By Type of Facility |

General Hospitals Specialized Hospitals Teaching Hospitals Rural Hospitals Rehabilitation Centers |

|

By Ownership |

Public Hospitals Private Hospitals Non-Profit Hospitals |

|

By Bed Capacity |

Small Hospitals (<100 beds) Medium Hospitals (100-300 beds) Large Hospitals (>300 beds) |

|

By Service Type |

Inpatient Services Outpatient Services Diagnostic Services Surgical Services Emergency Care Services |

|

By Region |

North East South West |

Products

Key Target Audience

Private Hospital Chains

Public Healthcare Administrations (U.S. Department of Health and Human Services)

Non-Profit Healthcare Organizations

Medical Device Manufacturers

Technology Solution Providers (Cerner Corporation, Epic Systems)

Government and Regulatory Bodies (Centers for Medicare & Medicaid Services, Food and Drug Administration)

Investments and Venture Capitalist Firms

Health Insurance Providers

Banks and Financial Institutions

Companies

Major Players in the Market

HCA Healthcare

Ascension

Tenet Healthcare

Community Health Systems

Universal Health Services

CommonSpirit Health

Mayo Clinic

Cleveland Clinic

Kaiser Permanente

Providence St. Joseph Health

Trinity Health

NewYork-Presbyterian Hospital

Advocate Aurora Health

Baptist Health

UPMC (University of Pittsburgh Medical Center)

Table of Contents

1. USA Hospital Facilities Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (Healthcare Infrastructure Investments, Patient Volume Growth, Technology Adoption Rate)

1.4 Market Segmentation Overview

2. USA Hospital Facilities Market Size (In USD Bn)

2.1 Historical Market Size (Hospital Construction Spending, Equipment Procurement, Staffing Expenditures)

2.2 Year-On-Year Growth Analysis (Facility Expansion, Healthcare Technology Integration, Patient Admissions)

2.3 Key Market Developments and Milestones (New Hospitals, Infrastructure Upgrades, Policy Changes)

3. USA Hospital Facilities Market Analysis

3.1 Growth Drivers

3.1.1 Expansion in Healthcare Infrastructure (Government Initiatives, Private Sector Investment)

3.1.2 Aging Population Impact on Healthcare Demand (Chronic Disease Management, Senior Care Facilities)

3.1.3 Technological Advancements (AI in Healthcare, Robotics in Surgery, Telemedicine Expansion)

3.1.4 Increasing Focus on Patient Safety and Quality Standards (Accreditation, Compliance with Safety Regulations)

3.2 Market Challenges

3.2.1 High Operational and Maintenance Costs (Labor Costs, Technology Investments, Regulatory Compliance)

3.2.2 Regulatory and Policy Barriers (Healthcare Reforms, Federal and State-Level Regulations)

3.2.3 Skilled Workforce Shortage (Nurses, Specialized Healthcare Workers, Administrative Efficiency)

3.3 Opportunities

3.3.1 Investments in Rural Healthcare Facilities (Government Grants, Public-Private Partnerships)

3.3.2 Integration of Digital Health Solutions (EHR, IoT in Hospitals, Data Security)

3.3.3 Expansion of Private Healthcare Networks (Mergers, Acquisitions, Strategic Partnerships)

3.4 Trends

3.4.1 Adoption of Telemedicine and Remote Patient Monitoring (Telehealth Platforms, Home Care Integration)

3.4.2 Rise in Patient-Centric Hospital Designs (Outpatient Services, Comfort-Oriented Facilities)

3.4.3 Energy-Efficient and Sustainable Hospital Infrastructure (LEED-Certified Buildings, Smart Hospital Designs)

3.5 Government Regulation

3.5.1 U.S. Department of Health and Human Services (HHS) Standards

3.5.2 Federal Healthcare Facility Guidelines (HIPAA Compliance, Safety Standards)

3.5.3 Medicaid and Medicare Hospital Facility Regulations

3.5.4 Public-Private Partnerships in Healthcare Development

3.6 SWOT Analysis

3.7 Stake Ecosystem (Hospitals, Suppliers, Regulators, Investors)

3.8 Porters Five Forces (Bargaining Power of Suppliers, Threat of New Entrants, Industry Rivalry)

3.9 Competition Ecosystem

4. USA Hospital Facilities Market Segmentation

4.1 By Type of Facility (In Value %)

4.1.1 General Hospitals

4.1.2 Specialized Hospitals

4.1.3 Teaching Hospitals

4.1.4 Rural Hospitals

4.1.5 Rehabilitation Centers

4.2 By Ownership (In Value %)

4.2.1 Public Hospitals

4.2.2 Private Hospitals

4.2.3 Non-Profit Hospitals

4.3 By Bed Capacity (In Value %)

4.3.1 Small Hospitals (Less than 100 beds)

4.3.2 Medium Hospitals (100-300 beds)

4.3.3 Large Hospitals (More than 300 beds)

4.4 By Service Type (In Value %)

4.4.1 Inpatient Services

4.4.2 Outpatient Services

4.4.3 Diagnostic Services

4.4.4 Surgical Services

4.4.5 Emergency Care Services

4.5 By Region (In Value %)

4.5.1 North

4.5.2 East

4.5.3 South

4.5.4 West

5. USA Hospital Facilities Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 HCA Healthcare

5.1.2 Ascension

5.1.3 Tenet Healthcare

5.1.4 Community Health Systems

5.1.5 Universal Health Services

5.1.6 CommonSpirit Health

5.1.7 Mayo Clinic

5.1.8 Cleveland Clinic

5.1.9 Kaiser Permanente

5.1.10 Providence St. Joseph Health

5.1.11 Trinity Health

5.1.12 NewYork-Presbyterian Hospital

5.1.13 Advocate Aurora Health

5.1.14 Baptist Health

5.1.15 UPMC (University of Pittsburgh Medical Center)

5.2 Cross Comparison Parameters (Bed Capacity, Revenue, Headquarters, Inception Year, No. of Employees, Patient Care Revenue, Technological Investment, Geographic Presence)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. USA Hospital Facilities Market Regulatory Framework

6.1 Federal Hospital Compliance Regulations (EHR, Patient Safety)

6.2 Certification Processes (JCAHO, LEED Certification, ISO Standards)

6.3 Healthcare Facility Accreditation Requirements (Healthcare Inspections, Compliance Programs)

7. USA Hospital Facilities Future Market Size (In USD Bn)

7.1 Future Market Size Projections (Hospital Construction, Patient Demand, Technological Integration)

7.2 Key Factors Driving Future Market Growth (Healthcare Spending, Policy Changes, Technological Advancements)

8. USA Hospital Facilities Future Market Segmentation

8.1 By Type of Facility (In Value %)

8.2 By Ownership (In Value %)

8.3 By Bed Capacity (In Value %)

8.4 By Service Type (In Value %)

8.5 By Region (In Value %)

9. USA Hospital Facilities Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Available Market, Serviceable Obtainable Market)

9.2 Customer Cohort Analysis (Patient Demographics, Care Preferences, Insurance Coverage)

9.3 Marketing Initiatives (Digital Transformation, Patient Experience, Community Outreach)

9.4 White Space Opportunity Analysis (Untapped Geographic Regions, New Facility Designs, Specialized Care Opportunities)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the USA Hospital Facilities market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the USA Hospital Facilities market. This includes assessing market penetration, hospital capacity, and the resultant revenue generation. An evaluation of service quality statistics is also conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of hospitals and healthcare organizations. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple healthcare facility managers to acquire detailed insights into operational efficiency, technology adoption, and patient care services. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the USA Hospital Facilities market.

Frequently Asked Questions

01. How big is the USA Hospital Facilities Market?

The USA Hospital Facilities market was valued at USD 1415 billion, driven by the increasing demand for healthcare services, rising investment in healthcare infrastructure, and the rapid adoption of advanced medical technologies.

02. What are the challenges in the USA Hospital Facilities Market?

Challenges in the USA Hospital Facilities market include high operational and maintenance costs, regulatory compliance requirements, and a shortage of skilled healthcare professionals. These factors limit the ability of hospital facilities to scale quickly and maintain cost efficiency.

03. Who are the major players in the USA Hospital Facilities Market?

Key players in the USA Hospital Facilities market include HCA Healthcare, Ascension, Tenet Healthcare, Mayo Clinic, and Cleveland Clinic. These companies dominate due to their extensive hospital networks, strong financial backing, and advanced healthcare services.

04. What are the growth drivers of the USA Hospital Facilities Market?

Growth drivers in the USA Hospital Facilities market include the aging population, technological advancements in healthcare, and increasing investments in digital health solutions such as electronic health records (EHR) and telemedicine platforms. Additionally, government funding for healthcare infrastructure continues to support market expansion.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.