USA Telecommunication Market Outlook to 2030

Region:North America

Author(s):Shambhavi Awasthi

Product Code:KROD9294

January 2025

88

About the Report

USA Telecommunication Market Overview

- The USA Telecommunication Market is currently valued at USD 400 billion, driven by advancements in wireless communication technologies, including the expanded deployment of 5G networks and the shift towards high-speed broadband connectivity. These developments are facilitating enhanced data transmission capabilities and fostering increased digital adoption across various industries. Rapid technological innovations are creating a strong demand for faster and more reliable communication infrastructure to meet the growing digital economy's needs.

- Major cities like New York, San Francisco, and Los Angeles dominate the market due to their high population density and technological infrastructure, creating significant demand for telecommunications services. These cities are home to leading tech companies and innovation hubs, further spurring the adoption of advanced telecommunication solutions to support both consumer and business demands.

- The FCC plays a pivotal role in regulating the telecommunications industry, establishing policies that govern everything from net neutrality to spectrum allocation. Recent developments indicate that new regulations on net neutrality will be enforced by the end of 2024, requiring service providers to treat all internet traffic equally. This regulatory environment creates a framework within which telecom companies must operate, influencing their pricing strategies, service delivery models, and overall market competitiveness. Compliance with these regulations is essential for maintaining operational licenses and avoiding legal repercussions.

USA Telecommunication Market Segmentation

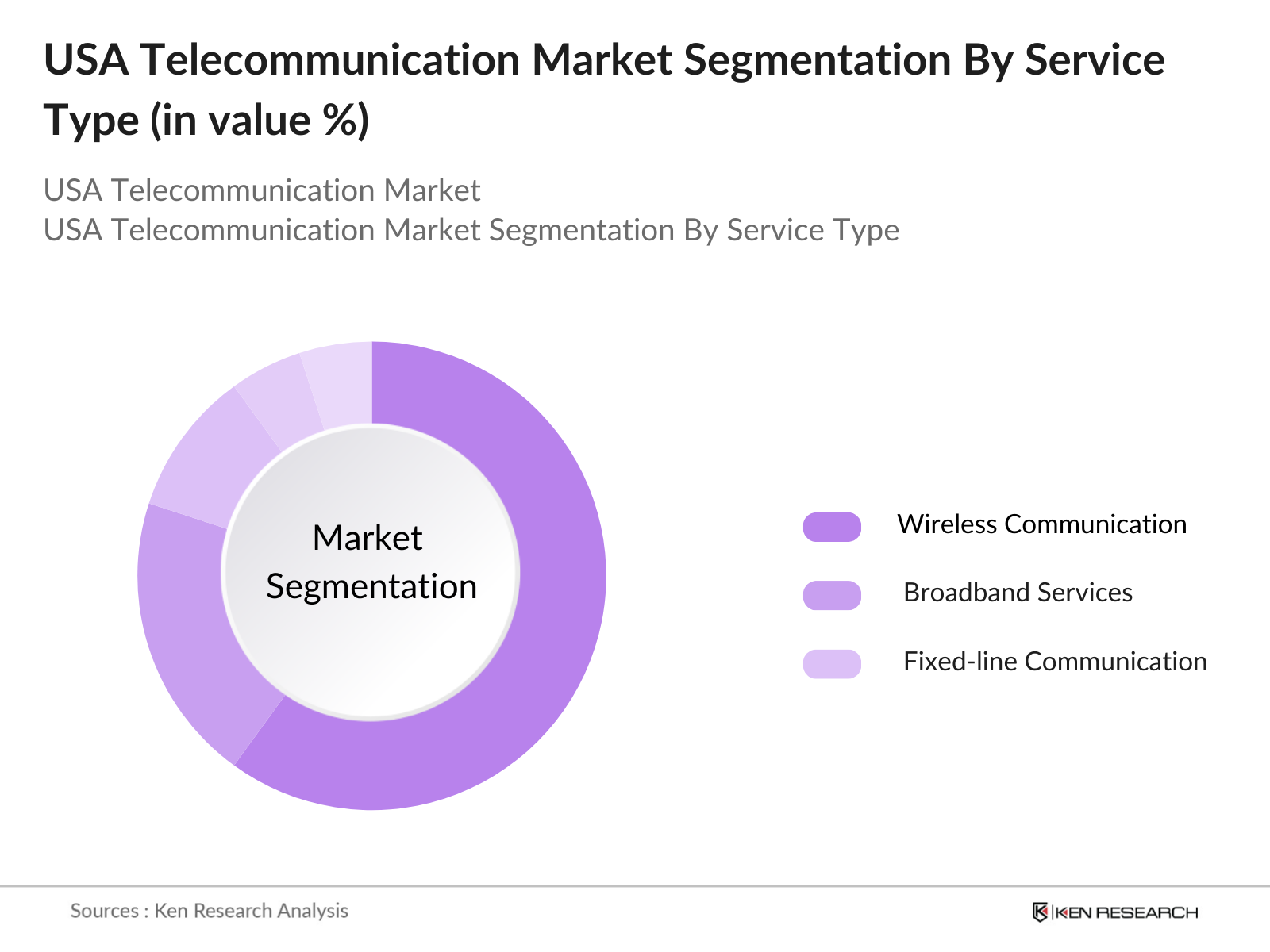

- By Service Type: The USA Telecommunication market is segmented by service type into wireless communication, broadband services, and fixed-line communication. Wireless communication holds a dominant share due to the increasing demand for mobile connectivity, largely driven by the widespread usage of smartphones and the extensive rollout of 5G. Leading wireless providers like AT&T and Verizon have successfully adapted their infrastructure to cater to the high-speed demands, reinforcing this segment's position in the market.

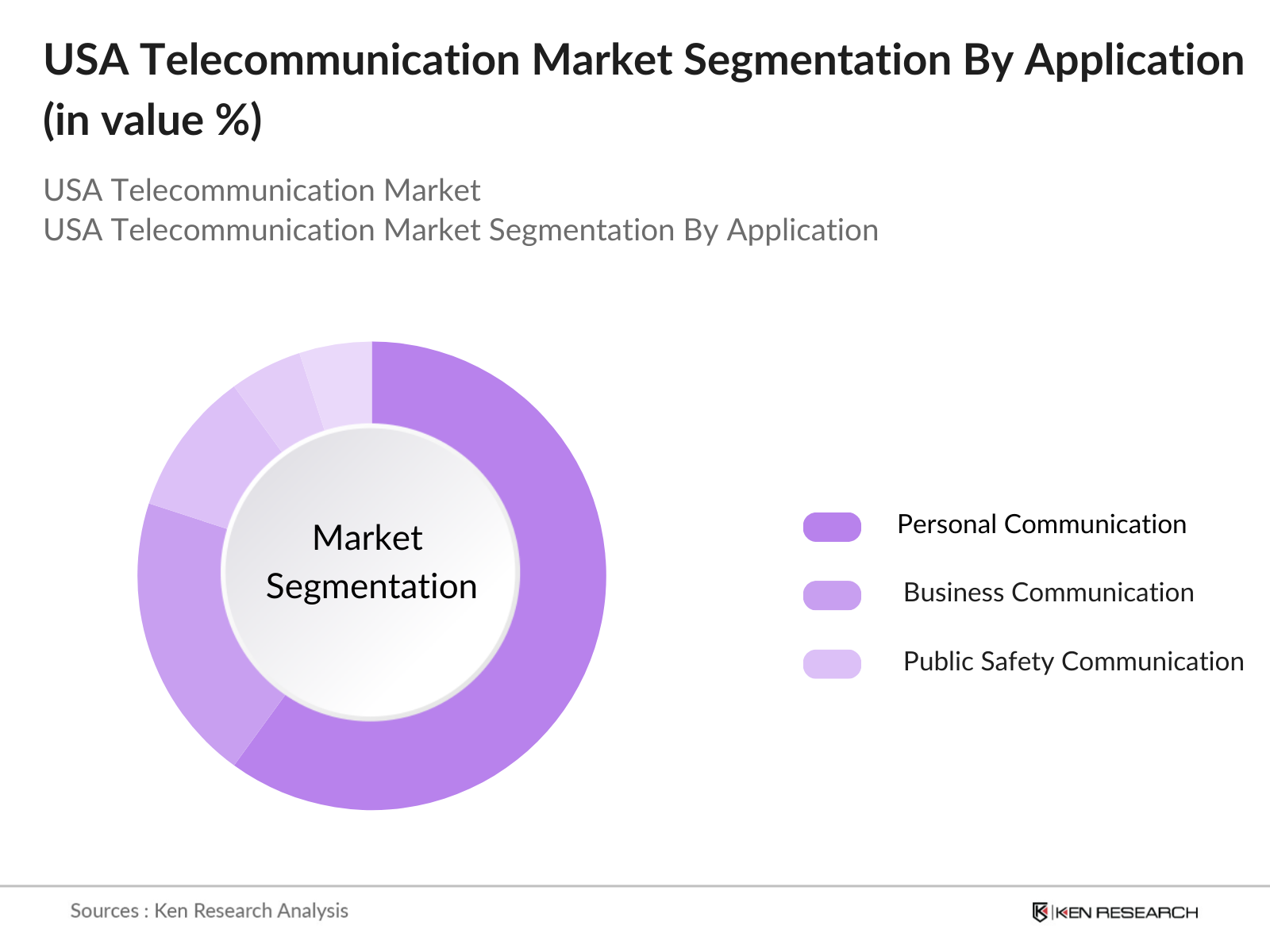

- By Application: The USA Telecommunication market is segmented by application into personal communication, business communication, and public safety communication. Business communication leads the application segment due to the increasing demand for cloud-based solutions and unified communication systems across corporate sectors. The adoption of remote work models and the digital transformation of business processes have propelled this segment, with companies relying heavily on advanced telecommunications for efficient operations.

USA Telecommunication Market Competitive Landscape

The USA Telecommunication market is dominated by key players, each contributing significantly to the industrys growth through technological advancements and extensive market reach. The USA Telecommunication market is consolidated, with major players such as Verizon, AT&T, T-Mobile, and Comcast, which leverage extensive infrastructure, technological expertise, and customer loyalty to maintain their competitive positions. These companies' significant investments in expanding 5G networks highlight their commitment to strengthening market presence.

USA Telecommunication Market Analysis

Growth Drivers

- Increasing Smartphone Penetration: The growing adoption of smartphones continues to significantly impact the telecommunications market. In 2024, smartphone users in the U.S. are expected to reach approximately 298 million, up from around 275 million in 2022. This surge in smartphone usage is driven by advancements in technology, making devices more accessible and affordable. With over 80% of the U.S. population now owning a smartphone, telecom companies are witnessing increased demand for data services and applications, thereby enhancing their revenue streams. The trend indicates a strong trajectory for continued growth within the telecom sector as more users engage with mobile services.

- Expansion of 5G Networks: The roll-out of 5G technology is a pivotal growth driver for the U.S. telecommunications market. By the end of 2024, 5G subscriptions are projected to exceed 200 million, marking a significant increase from the current 5G adoption rate. This growth is fueled by the demand for faster data speeds and lower latency, which 5G networks can provide. The technological advancements associated with 5G not only enhance mobile broadband services but also pave the way for innovations in IoT, smart cities, and advanced mobile applications. The telecom industry's ability to capitalize on 5G technology will be crucial for sustaining growth in the coming years.

- Rise in Data Consumption: The telecommunications market is experiencing an unprecedented increase in data consumption, with the average monthly data usage per smartphone user projected to reach 12.5 GB in 2024, up from 10.5 GB in 2022. This growth is attributed to the increasing reliance on streaming services, social media, and online gaming. As data-intensive applications become more prevalent, telecom providers are investing in infrastructure upgrades and expanded bandwidth to meet customer demands.

Market Challenges

- Regulatory Compliance and Legal Issues: The telecommunications industry in the U.S. faces substantial regulatory challenges, particularly regarding compliance with Federal Communications Commission (FCC) policies. In the past year, the FCC has enforced over 1,500 compliance measures to ensure service providers adhere to standards that protect consumer rights and promote competition. These regulations can impose significant operational costs on telecom companies, potentially leading to financial strain, particularly for smaller players. Moreover, evolving regulatory frameworks may require ongoing investments in compliance technologies and legal expertise, affecting overall market agility and profitability.

- Cybersecurity Threats: As telecommunications networks become increasingly digitized, they are also more vulnerable to cyberattacks. The industry has witnessed over a 30% increase in cyberattacks targeting telecom networks in 2023, posing significant risks to both service providers and customers. Cybersecurity breaches can lead to data loss, service disruptions, and a decline in consumer trust, all of which can result in substantial financial losses. Telecom companies are therefore required to invest heavily in cybersecurity measures, which can divert funds from other critical areas of growth and innovation.

USA Telecommunication Market Future Outlook

Over the next five years, the USA Telecommunication market is expected to experience steady growth fueled by the ongoing 5G rollout, increased demand for high-speed internet, and the integration of advanced technologies such as AI and IoT. The evolution of cloud computing and edge technology will further drive the need for reliable telecommunications infrastructure, enabling seamless connectivity for both businesses and consumers.

Market Opportunities

- IoT Integration: The integration of Internet of Things (IoT) technology presents a significant growth opportunity for the U.S. telecommunications market. With over 50 billion connected IoT devices anticipated globally by 2025, telecom companies are positioned to capitalize on this trend by offering tailored connectivity solutions. These devices require robust and reliable network infrastructure, driving demand for advanced telecommunications services. By developing IoT-specific offerings, such as smart home technology and industrial IoT applications, telecom providers can diversify their service portfolios and capture a larger share of the growing market.

- Expansion into Emerging Markets: Emerging markets represent a vast opportunity for U.S. telecommunications companies looking to expand their customer base. With an estimated 3 billion potential customers in underserved regions globally, telecom firms can leverage their expertise and technology to provide essential communication services. Initiatives targeting mobile payments, affordable data plans, and rural connectivity can foster growth in these markets. Companies that successfully penetrate these emerging areas can significantly enhance their revenue streams and global presence.

Scope of the Report

|

Segment |

Sub-Segment |

|

By Service Type |

Voice Services |

|

Data Services |

|

|

Value-Added Services |

|

|

By Technology |

4G |

|

5G |

|

|

Fixed Wireless |

|

|

By End-User |

Residential |

|

Commercial |

|

|

Government |

|

|

By Region |

Northeast |

|

Midwest |

|

|

South |

|

|

West |

|

|

By Device Type |

Smartphones |

|

Tablets |

|

|

Laptops |

Products

Key Target Audience

Telecommunication Service Providers

Network Infrastructure Companies

Government and Regulatory Bodies (e.g., FCC)

Internet Service Providers

Device Manufacturers

Investors and Venture Capitalist Firms

Technology Integrators

Cloud Service Providers

Companies

Players mentioned in the report

Verizon Communications Inc.

AT&T Inc.

T-Mobile US, Inc.

Comcast Corporation

Sprint Corporation

CenturyLink, Inc.

Charter Communications, Inc.

DISH Network Corporation

Frontier Communications Corporation

Altice USA, Inc.

Cincinnati Bell Inc.

U.S. Cellular

Windstream Holdings

GTT Communications

Vonage Holdings

Table of Contents

1. USA Telecommunication Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Telecommunication Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Telecommunication Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Smartphone Penetration (smartphone users in the U.S. reached approximately 298 million in 2024)

3.1.2. Expansion of 5G Networks (5G subscriptions in the U.S. are projected to exceed 200 million by the end of 2024)

3.1.3. Rise in Data Consumption (the average monthly data consumption per smartphone user is forecasted to be 12.5 GB in 2024)

3.1.4. Government Investments in Digital Infrastructure (over $65 billion allocated for broadband expansion in rural areas)

3.2. Market Challenges

3.2.1. Regulatory Compliance and Legal Issues (the FCC enforced over 1,500 compliance measures in the past year)

3.2.2. Cybersecurity Threats (over 30% increase in cyberattacks targeting telecom networks reported in 2023)

3.2.3. High Competition (top 4 telecom companies hold approximately 70% market share, intensifying competition)

3.3. Opportunities

3.3.1. IoT Integration (over 50 billion connected IoT devices anticipated globally by 2025)

3.3.2. Expansion into Emerging Markets (estimated 3 billion potential customers in underserved regions)

3.3.3. Adoption of Artificial Intelligence (AI solutions expected to reduce operational costs by 20% in telecom)

3.4. Trends

3.4.1. Shift towards Subscription-Based Services (subscription services projected to contribute to over 80% of revenue by 2025)

3.4.2. Focus on Sustainability (70% of telecom companies committing to carbon neutrality by 2030)

3.4.3. Enhanced Customer Experience Initiatives (personalized services leading to a 15% increase in customer retention rates)

3.5. Government Regulation

3.5.1. FCC Policies and Guidelines (new regulations on net neutrality to be enforced by the end of 2024)

3.5.2. Broadband Deployment Initiatives ($42 billion dedicated to improving broadband access in underserved areas)

3.5.3. Spectrum Allocation Policies (spectrum auctions generating over $22 billion in revenue in 2023)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. USA Telecommunication Market Segmentation

4.1. By Service Type (In Value %)

4.1.1. Voice Services

4.1.2. Data Services

4.1.3. Value-Added Services

4.2. By Technology (In Value %)

4.2.1. 4G

4.2.2. 5G

4.2.3. Fixed Wireless

4.3. By End-User (In Value %)

4.3.1. Residential

4.3.2. Commercial

4.3.3. Government

4.4. By Region (In Value %)

4.4.1. Northeast

4.4.2. Midwest

4.4.3. South

4.4.4. West

4.5. By Device Type (In Value %)

4.5.1. Smartphones

4.5.2. Tablets

4.5.3. Laptops

5. USA Telecommunication Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. AT&T Inc.

5.1.2. Verizon Communications Inc.

5.1.3. T-Mobile USA Inc.

5.1.4. Comcast Corporation

5.1.5. Charter Communications Inc.

5.1.6. Sprint Corporation

5.1.7. CenturyLink (Lumen Technologies)

5.1.8. Dish Network Corporation

5.1.9. Frontier Communications Corporation

5.1.10. US Cellular Corporation

5.1.11. Altice USA Inc.

5.1.12. Cox Communications Inc.

5.1.13. Windstream Holdings, Inc.

5.1.14. Mediacom Communications Corporation

5.1.15. Cincinnati Bell Inc.

5.2. Cross Comparison Parameters (No. of Subscribers, Revenue, Market Share, Network Coverage, Customer Satisfaction Index, Investment in R&D, Number of Service Outages, Regulatory Compliance Score)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Telecommunication Market Regulatory Framework

6.1. FCC Regulations

6.2. Compliance Requirements

6.3. Certification Processes

7. USA Telecommunication Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Telecommunication Future Market Segmentation

8.1. By Service Type (In Value %)

8.2. By Technology (In Value %)

8.3. By End-User (In Value %)

8.4. By Region (In Value %)

8.5. By Device Type (In Value %)

9. USA Telecommunication Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This initial stage focuses on mapping out the telecommunication ecosystem, identifying core players and service types. Through desk research, both secondary data s and proprietary databases are utilized to gather foundational insights.

Step 2: Market Analysis and Construction

Historical data collection is conducted to assess market development, penetration rates, and the impact of technological changes. This stage verifies service demand statistics and infrastructure trends.

Step 3: Hypothesis Validation and Expert Consultation

Through in-depth interviews with industry stakeholders, primary insights are gathered to validate market hypotheses, enhancing the precision of market projections.

Step 4: Research Synthesis and Final Output

Collating feedback from telecom providers and infrastructure developers, the research consolidates market insights, providing an accurate and comprehensive market analysis.

Frequently Asked Questions

01. How big is the USA Telecommunication Market?

The USA Telecommunication Market is valued at USD 400 billion, with substantial growth driven by 5G deployment and the digital transformation across various sectors.

02. What are the challenges in the USA Telecommunication Market?

Key challenges include regulatory restrictions, high infrastructure costs, and security risks associated with data transmission, which telecom companies must navigate.

03. Who are the major players in the USA Telecommunication Market?

Major players include Verizon, AT&T, T-Mobile, Comcast, and Sprint, who dominate due to their extensive network infrastructure and innovative service offerings.

04. What are the growth drivers of the USA Telecommunication Market?

The market is driven by the increasing demand for high-speed internet, advancements in wireless communication, and the integration of IoT in business operations.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.