Vietnam Plastic Market Report Outlook to 2028

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD10957

January 2025

91

About the Report

Vietnam Plastic Market Overview

- The Vietnam Plastic Market is valued at USD 4.2 billion, based on a five-year historical analysis. This market growth is primarily driven by an increased demand in packaging, automotive, and construction industries, alongside government incentives aimed at industrial expansion. With continuous infrastructure projects and the burgeoning e-commerce sector fueling the need for efficient packaging solutions, the market's trajectory is robust. Additionally, a significant shift towards eco-friendly materials is gradually influencing the plastic sector.

- Vietnams plastic market dominance can be seen mainly in Ho Chi Minh City and Hanoi due to their established industrial base and the high concentration of manufacturing units. Ho Chi Minh City, as a commercial hub, serves as the main production center, supplying to both domestic and international markets. Furthermore, Hanois growth in construction and consumer goods manufacturing accelerates demand for plastics, positioning it as a pivotal region within the sector.

- To ensure quality and safety in recycled plastics, Vietnams government has introduced specific standards for plastic recyclables, covering contamination limits and reuse criteria. These standards aim to improve recycling efficiency and encourage manufacturers to use recycled inputs in production.

Vietnam Plastic Market Segmentation

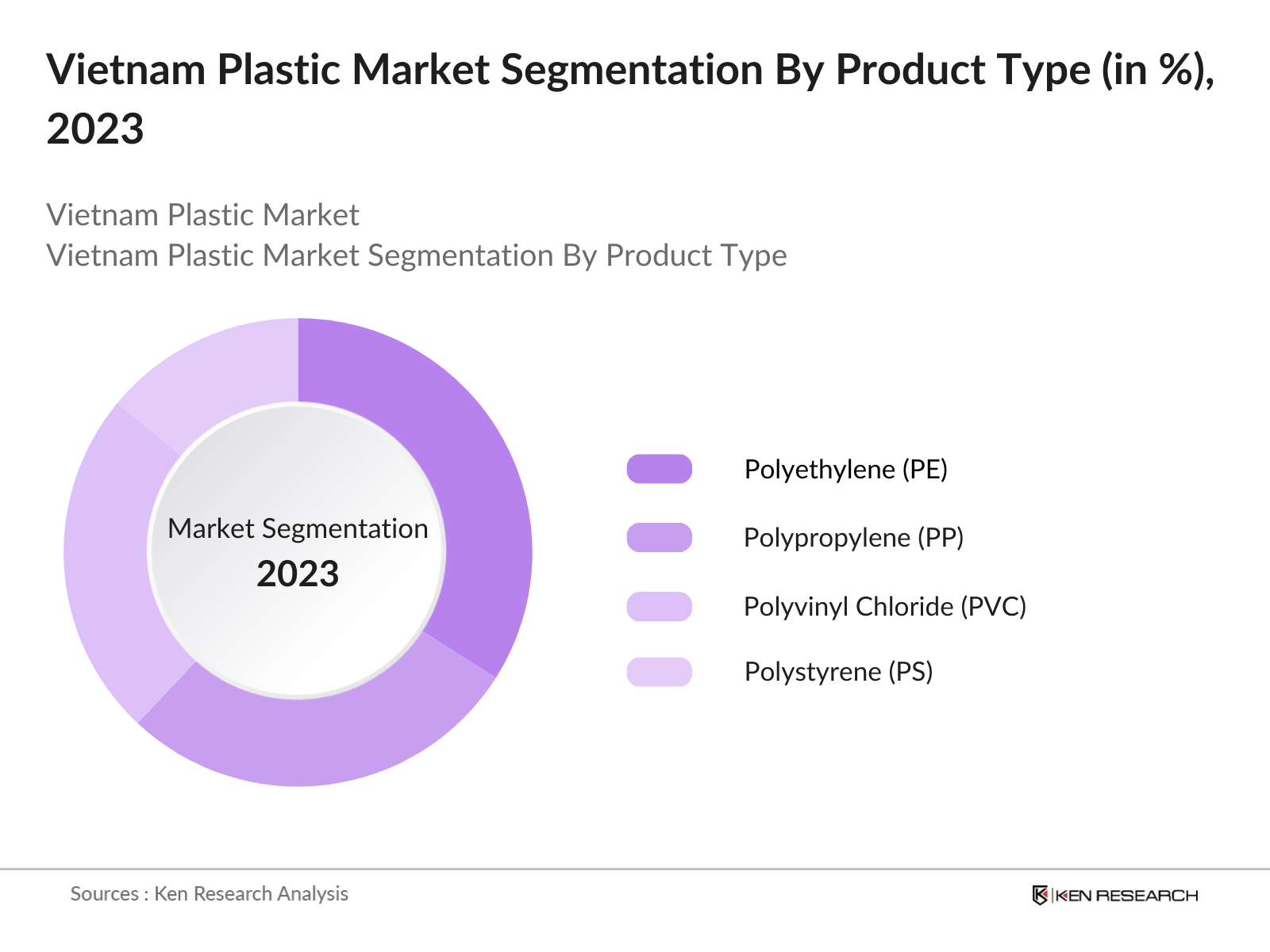

By Product Type: The Vietnam Plastic Market is segmented by product type into Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), and Polyethylene Terephthalate (PET). Recently, Polyethylene (PE) has shown a dominant market share within this segmentation. The materials versatility and cost-effectiveness make it widely adopted for applications in packaging and consumer goods. Its high resistance to chemicals and durability further drive its preference across multiple industries, particularly in the booming food and beverage packaging segment, which requires safe, durable materials to meet demand.

By Application: The Vietnam Plastic Market is further segmented by application into Packaging, Construction, Automotive, Electronics, and Agriculture. Within this category, packaging holds a significant share, driven by the countrys expanding food and beverage industry and the rise in e-commerce activities. The demand for protective and flexible packaging options that preserve product quality and extend shelf life is a critical factor. Moreover, the use of lightweight and durable plastic in packaging minimizes transport costs, making it a preferred choice for many manufacturers.

Vietnam Plastic Market Competitive Landscape

The Vietnam Plastic Market is dominated by a few major players, including both domestic giants and global brands with strong manufacturing and distribution networks in the region. This consolidation highlights the substantial impact of these companies in driving market trends and meeting diverse customer demands across industries.

Vietnam Plastic Industry Analysis

Growth Drivers

- Rapid Urbanization and Infrastructure Development: Vietnam's urban population has been growing significantly, with around 37 million people now living in urban areas. As of 2024, this urban shift is creating increased demand for infrastructure projects, including residential, commercial, and industrial developments, driving up plastic requirements for construction applications. For instance, high-density polyethylene (HDPE) and polyvinyl chloride (PVC) are heavily used in water pipes, insulation, and cables in the construction industry.

- Expanding Manufacturing Sector: Vietnam's manufacturing sector, valued as one of the highest contributors to the GDP, has been experiencing growth due to increased foreign direct investment (FDI). The government reports 2,000+ FDI projects in 2024, primarily in electronics, automotive, and textiles. This expansion significantly drives plastic demand for components, packaging, and equipment used in manufacturing. High levels of polypropylene usage, a plastic integral to electronic components, are observed.

- Rising Demand in Packaging Industry: Vietnam's packaging industry has surged, with annual demand reaching billions of units, largely due to e-commerce and the food and beverage sector. Polyethylene and PET plastics are particularly in demand for packaging solutions. The Ministry of Industry and Trade projects sustained growth in packaging needs, driven by both domestic consumption and export-oriented manufacturing.

Market Challenges

- Environmental Concerns and Regulations: Vietnam generated over 3.2 million tons of plastic waste in 2023, leading to strict policies on waste management and single-use plastic reduction. The government is enforcing recycling mandates and restrictions on certain plastic products, impacting industry players. The push toward compliance with sustainable practices poses logistical and financial challenges. Source.

- High Cost of Raw Materials: Vietnams reliance on imported raw materials has escalated production costs, with 70% of plastic resins sourced globally. This dependency exposes local manufacturers to price volatility in the international market, impacting profitability. Imported plastic resins saw an increase in

Vietnam Plastic Market Future Outlook

Over the next five years, the Vietnam Plastic Market is anticipated to experience notable growth, driven by rising industrial production, government incentives for eco-friendly manufacturing, and continuous technological advancements. The push for biodegradable and sustainable plastics, coupled with growing awareness around environmental protection, will influence material innovations within the sector. Additionally, the surge in urban infrastructure and the evolution of packaging solutions tailored for Vietnams expanding e-commerce sector are expected to reinforce market growth, paving the way for further investments.

Opportunities

- Technological Advancements in Bioplastics: Vietnam has seen growing interest in bioplastics, with local companies investing in research for biodegradable alternatives. The Ministry of Science and Technology has supported projects focusing on bio-based PET and PLA, which reduce reliance on traditional plastics. Bioplastics research funding has increased, offering significant opportunities in packaging and consumer goods.

- Growing Export Demand: Vietnams exports of plastic products increased to $5 billion in 2023, with strong demand from the U.S., Japan, and Europe. The countrys competitive advantage in manufacturing, coupled with high-quality production, presents robust growth prospects for plastic exports. Supportive trade agreements further bolster these export opportunities.

Scope of the Report

|

Product Type |

Polyethylene Polypropylene Polyvinyl Chloride Polystyrene Polyethylene Terephthalate |

|

Application |

Packaging Construction Automotive Electronics Agriculture |

|

Processing Technology |

Injection Molding Extrusion Blow Molding 3D Printing |

|

End-User Industry |

Consumer Goods Industrial Manufacturing Healthcare Food & Beverage |

|

Region |

Hanoi Ho Chi Minh City Da Nang Mekong Delta Northern Vietnam |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

- Investor and Venture Capitalist Firms

- Government and Regulatory Bodies (Vietnam Ministry of Industry and Trade)

- Plastic Product Manufacturing Companies

- Packaging Industries

- Environmental and Sustainability Companies

- Construction Sector Companies

- Automotive Industries

- Electronics Manufacturing Companies

Companies

Players Mentioned in the Report

- SCG Chemicals

- Binh Minh Plastic

- An Phat Holdings

- SABIC Vietnam

- Formosa Plastics Group

- Tien Phong Plastic

- LG Chem

- BASF Vietnam

- Dow Chemical Vietnam

- Reliance Industries

Table of Contents

1.Vietnam Plastic Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Vietnam Plastic Market Size (in USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Vietnam Plastic Market Analysis

3.1. Growth Drivers

3.1.1. Rapid Urbanization and Infrastructure Development

3.1.2. Expanding Manufacturing Sector

3.1.3. Rising Demand in Packaging Industry

3.1.4. Government Policies and Incentives for Industrial Growth

3.2. Market Challenges

3.2.1. Environmental Concerns and Regulations

3.2.2. High Cost of Raw Materials

3.2.3. Recycling Infrastructure Limitations

3.3. Opportunities

3.3.1. Technological Advancements in Bioplastics

3.3.2. Growing Export Demand

3.3.3. Expansion in Eco-friendly Product Lines

3.4. Trends

3.4.1. Shift to Sustainable Packaging Solutions

3.4.2. Adoption of Advanced Manufacturing Technologies

3.4.3. Growth of E-commerce Boosting Demand for Packaging

3.5. Government Regulations

3.5.1. Plastic Waste Management Policies

3.5.2. Standards for Recycled Plastics

3.5.3. Import-Export Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Vietnam Plastic Market Segmentation

4.1. By Product Type (in Value %)

4.1.1. Polyethylene (PE)

4.1.2. Polypropylene (PP)

4.1.3. Polyvinyl Chloride (PVC)

4.1.4. Polystyrene (PS)

4.1.5. Polyethylene Terephthalate (PET)

4.2. By Application (in Value %)

4.2.1. Packaging

4.2.2. Construction

4.2.3. Automotive

4.2.4. Electronics

4.2.5. Agriculture

4.3. By Processing Technology (in Value %)

4.3.1. Injection Molding

4.3.2. Extrusion

4.3.3. Blow Molding

4.3.4. 3D Printing

4.4. By End-User Industry (in Value %)

4.4.1. Consumer Goods

4.4.2. Industrial Manufacturing

4.4.3. Healthcare

4.4.4. Food & Beverage

4.5. By Region (in Value %)

4.5.1. Hanoi

4.5.2. Ho Chi Minh City

4.5.3. Da Nang

4.5.4. Mekong Delta

4.5.5. Northern Vietnam

5. Vietnam Plastic Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. SCG Chemicals

5.1.2. Binh Minh Plastic Joint Stock Company

5.1.3. Tien Phong Plastic Joint Stock Company

5.1.4. An Phat Holdings

5.1.5. SABIC Vietnam

5.1.6. PetroVietnam

5.1.7. LG Chem

5.1.8. BASF Vietnam

5.1.9. Dow Chemical Vietnam

5.1.10. Reliance Industries

5.1.11. Formosa Plastics Group

5.1.12. Eastman Chemical Company

5.1.13. Evonik Industries

5.1.14. Mitsui Chemicals Vietnam

5.1.15. Toray Industries

5.2. Cross Comparison Parameters (Headquarters, Inception Year, Revenue, Market Position, Number of Production Units, Annual Production Volume, Regional Reach, Key Clients)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6. Vietnam Plastic Market Regulatory Framework

6.1. Environmental Standards

6.2. Plastic Recycling Regulations

6.3. Import-Export Compliance

6.4. Health and Safety Standards

7. Vietnam Plastic Market Future Size (in USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8. Vietnam Plastic Market Future Segmentation

8.1. By Product Type (in Value %)

8.2. By Application (in Value %)

8.3. By Processing Technology (in Value %)

8.4. By End-User Industry (in Value %)

8.5. By Region (in Value %)

9. Vietnam Plastic Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. White Space Analysis

9.3. Marketing Strategy Recommendations

9.4. Emerging Market Opportunities

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase focuses on constructing an ecosystem map, encompassing all primary stakeholders within the Vietnam Plastic Market. Extensive desk research is undertaken using secondary databases, proprietary databases, and government publications to define critical variables influencing market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data related to production, consumption, and import-export dynamics in the Vietnam Plastic Market is gathered and analyzed. An evaluation of the distribution networks efficiency is also conducted to ensure reliable revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through expert consultations using computer-assisted telephone interviews (CATIs) with representatives from leading plastic manufacturers. This step provides critical insights into operational trends and helps refine market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with various plastic industry stakeholders, including suppliers and end-users, to gather detailed information on segment performance, consumer preferences, and emerging trends. This comprehensive approach ensures that the final output is accurate and thoroughly validated.

Frequently Asked Questions

01. How big is the Vietnam Plastic Market?

The Vietnam Plastic Market is valued at USD 4.2 billion, driven by high demand from sectors such as packaging, construction, and consumer goods, and supported by government policies aimed at industrial expansion.

02. What are the challenges in the Vietnam Plastic Market?

Key challenges include stringent environmental regulations, limited recycling infrastructure, and volatility in raw material prices, which impact production costs and sustainability.

03. Who are the major players in the Vietnam Plastic Market?

Prominent companies include SCG Chemicals, Binh Minh Plastic, An Phat Holdings, and SABIC Vietnam, each with a strong market presence and extensive distribution networks across various industries.

04. What are the growth drivers of the Vietnam Plastic Market?

Growth is propelled by increasing demand in packaging and construction sectors, government incentives for eco-friendly manufacturing, and the expansion of Vietnams e-commerce sector.

Why Buy From Us?

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.