Vietnam Steel Market Outlook to 2028

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD1327

October 2024

94

About the Report

Vietnam Steel Market Overview

-

The Vietnam Steel Market production was volumed at 13 million tons. This growth is primarily driven by increased infrastructure development, rising demand in the construction sector, and expansion in manufacturing activities. The Vietnamese government's continuous investment in infrastructure projects, coupled with foreign direct investment (FDI) in manufacturing, has significantly contributed to this upward trend.

-

The key players in this market, include Hoa Phat Group, Pomina Steel Corporation, Vietnam Steel Corporation (VNSTEEL), and Nam Kim Steel. These players are involved in both the production and distribution of various steel products, catering to domestic and international markets.

-

A significant development in the Vietnam steel market was the inauguration of Hoa Phat Group's Dung Quat Iron and Steel Complex in early 2023. This complex is one of the largest steel production facilities in Southeast Asia, with an annual production capacity of 6 million tons.

-

Ho Chi Minh City is the dominant region in the Vietnam steel market, due to the city's rapid industrialization, extensive infrastructure projects, and its role as a major commercial hub. The presence of large industrial parks and manufacturing facilities further consolidates its leading position.

Vietnam Steel Market Segmentation

The market can be segmented into various factors like product type, end-user, and region.

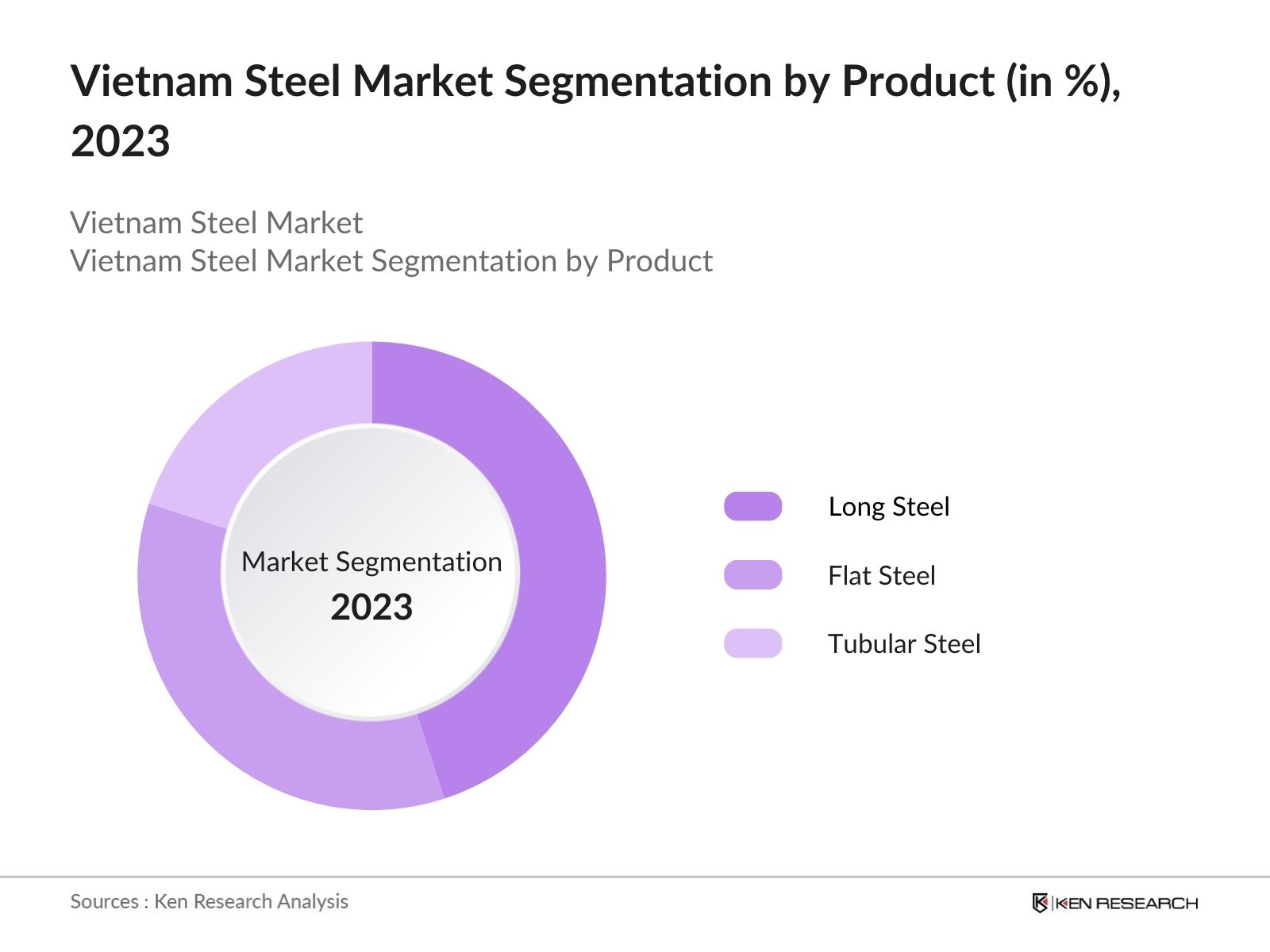

By Product Type: The market is segmented by product type into long steel, flat steel, and tubular steel. In 2023, long steel held the dominant market by its extensive use in construction and infrastructure projects. The versatility and strength of long steel make it a preferred choice for building bridges, roads, and high-rise buildings.

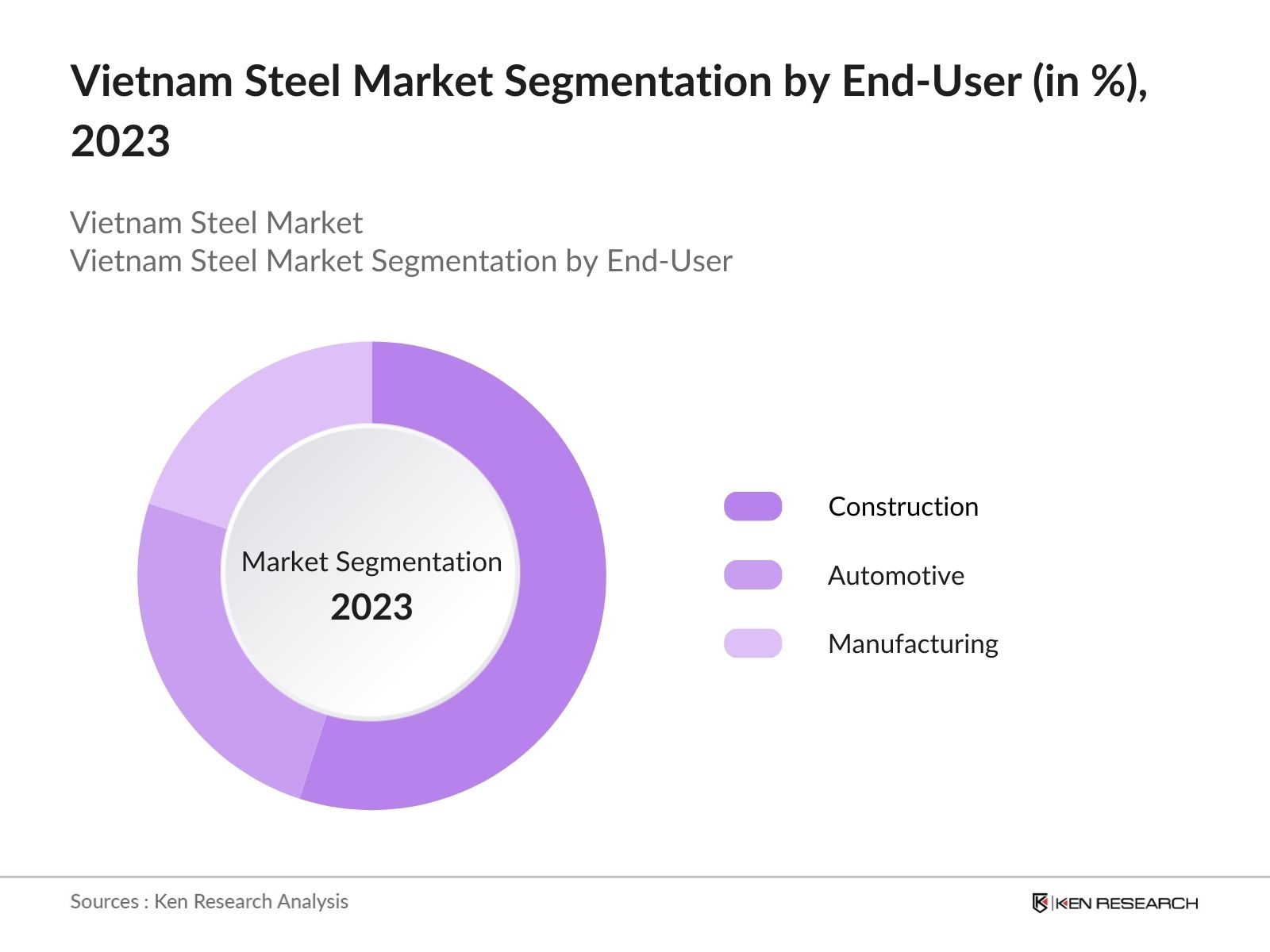

By End-User Industry: The market is segmented by end-user industry into construction, automotive, and manufacturing. In 2023, the construction industry was the largest consumer, due to the rapid urbanization and significant government spending on infrastructure projects have spurred the demand for steel in the construction sector.

By Region: The market is segmented by region into north, east, west and south. In 2023, the Northern region’s dominance is due to its concentration of industrial zones, access to raw materials, and well-established infrastructure. The presence of major steel production facilities, along with strategic proximity to key export markets such as China and ASEAN countries.

Vietnam Steel Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

Hoa Phat Group |

1992 |

Hanoi, Vietnam |

|

Pomina Steel Corporation |

1999 |

Ho Chi Minh City |

|

Vietnam Steel Corporation (VNSTEEL) |

1960 |

Hanoi, Vietnam |

|

Nam Kim Steel |

2002 |

Binh Duong, Vietnam |

|

Southern Steel Company |

1976 |

Ho Chi Minh City |

-

VNSTEEL: In 2022-23, VNSTEEL faced significant challenges, with a nearly 31% drop in net revenue, resulting in an after-tax loss of 216 billion VND in the first half of 2023. This decline was attributed to reduced domestic demand and a struggling real estate market, impacting the overall steel industry in Vietnam.

-

Pomina Steel Corporation: In the first nine months of 2023, Pomina Steel Corporation reported a net loss of 648 billion dong. This significant loss is attributed to reduced sales volume, lower selling prices, and increased production costs. Pomina's revenue for this period decreased by 74% to 2,948 billion dong compared to the same period last year, highlighting ongoing financial challenges in a competitive market.

Vietnam Steel Market Analysis

Market Growth Drivers

-

Manufacturing Expansion: The manufacturing sector is set to expand with an additional 100,000 new manufacturing facilities expected to be established in 2024, leading to increased steel consumption for machinery, equipment, and construction.

-

Automotive Industry Growth: With the production of 500,000 vehicles anticipated in 2024, the automotive industry will significantly drive the demand for high-quality steel for vehicle manufacturing and assembly processes.

-

Infrastructure Investments: The Vietnamese government plans to invest 400 trillion dong in infrastructure projects in 2024, including highways, urban railways, and bridges. These projects will significantly boost steel demand, providing substantial growth opportunities for the steel industry.

Market Challenges

-

Trade Barriers: The imposition of trade tariffs and anti-dumping duties on Vietnamese steel exports by various countries could impact the competitiveness and profitability of local steel producers, reducing export volumes and revenues.

-

Raw Material Price Volatility: The price of iron ore, a key raw material for steel production, is expected to remain volatile, with fluctuations between 100-150 USD per ton in 2024. This volatility poses challenges for cost management and pricing strategies for steel manufacturers.

Government Initiatives

-

National Steel Development Plan: In 2022, the Vietnamese government will implement a National Steel Development Plan, allocating VND 2.87 million to modernize steel production facilities, enhance research and development, and improve production capacity.

-

Green Transformation Commitment: The Vietnamese government, alongside the Vietnam Steel Association, has emphasized a commitment to transitioning the steel industry towards more sustainable practices. This initiative is part of the broader strategy to reduce carbon emissions and enhance environmental sustainability in line with global trends.

Vietnam Steel Market Future Outlook

The future outlook includes increased steel demand, technological advancements in production, adoption of sustainable practices, and growth in steel exports.

Future Market Trends

-

Export Growth: Vietnam's steel exports are expected to growing more as it was 11.13 million tons in 2023. This growth is driven by competitive pricing, improved production capacities, and expanding market access in ASEAN and European countries.

-

Adoption of Advanced Manufacturing Technologies: By 2028, 60% of Vietnam’s steel manufacturing facilities are expected to adopt Industry 4.0 technologies, including automation and AI, to enhance production efficiency and reduce costs. This technological shift is projected to result in a increase in production efficiency across the industry.

Scope of the Report

|

By Product |

Long Steel Flat Steel Tubular Steel |

|

By End-User |

Construction Automotive Manufacturing |

|

By Region |

North East West South |

Products

Key Target Audience – Organizations and Entities Who Can Benefit by Subscribing This Report:

- Steel Manufacturers

- Construction Companies

- Automotive Manufacturers

- Industrial Machinery Manufacturers

- Investment Firms

- Energy and Power Companies

- Mining Companies

- Export-Import Banks

- Financial Institutions

Companies

Players Mentioned in the Market Report

-

Hoa Phat Group

- Pomina Steel Corporation

- Vietnam Steel Corporation (VNSTEEL)

- Nam Kim Steel

- Southern Steel Company

- Thép Vi?t Ý

- Tôn Hoa Sen Group

- Tôn ?ông Á

- Vina Kyoei Steel

- SMC Trading Investment Joint Stock Company

- Thép Ti?n Lên

- Dong A Steel Joint Stock Company

- Hoa Sen Group

- Thai Nguyen Iron and Steel Corporation (TISCO)

- Dong Anh Lic

Table of Contents

1. Vietnam Steel Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Vietnam Steel Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Vietnam Steel Market Analysis

3.1. Growth Drivers

3.1.1. Infrastructure Development

3.1.2. Manufacturing Expansion

3.1.3. Automotive Industry Growth

3.1.4. Foreign Direct Investment

3.2. Restraints

3.2.1. Raw Material Price Volatility

3.2.2. Environmental Regulations

3.2.3. Trade Barriers

3.2.4. Technological Upgradation

3.3. Opportunities

3.3.1. Expansion of Production Facilities

3.3.2. Green Steel Initiatives

3.3.3. Export Market Expansion

3.3.4. Strategic Partnerships

3.4. Trends

3.4.1. Technological Advancements in Production

3.4.2. Adoption of Sustainable Practices

3.4.3. Increased Focus on High-Value Steel Products

3.4.4. Regional Market Integration

3.5. Government Regulation

3.5.1. National Steel Development Plan

3.5.2. Environmental Standards and Regulations

3.5.3. Export Promotion Policies

3.5.4. Public-Private Partnerships in Infrastructure

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4. Vietnam Steel Market Segmentation, 2023

4.1. By Product Type (in Value %)

4.1.1. Long Steel

4.1.2. Flat Steel

4.1.3. Tubular Steel

4.2. By End-User Industry (in Value %)

4.2.1. Construction

4.2.2. Automotive

4.2.3. Manufacturing

4.3. By Region (in Value %)

4.3.1. North

4.3.2. South

4.3.3. East

4.3.4. West

5. Vietnam Steel Market Cross Comparison

5.1 Detailed Profiles of Major Companies

5.1.1. Hoa Phat Group

5.1.2. Pomina Steel Corporation

5.1.3. Vietnam Steel Corporation (VNSTEEL)

5.1.4. Nam Kim Steel

5.1.5. Southern Steel Company

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. Vietnam Steel Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7. Vietnam Steel Market Regulatory Framework

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8. Vietnam Steel Market Future Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. Vietnam Steel Market Future Segmentation, 2028

9.1. By Product Type (in Value %)

9.2. By End-User Industry (in Value %)

9.3. By Region (in Value %)

10. Vietnam Steel Market Analysts’ Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step:1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step:2 Market Building:

Collating statistics on Vietnam steel industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Vietnam steel Industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step:3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step:4 Research output:

Our team will approach multiple steel manufacturers companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such steel manufacturers companies.

Frequently Asked Questions

01 How big is the Vietnam Steel market?

The Vietnam Steel Market production was volumed at 13 million tons. This growth is primarily driven by increased infrastructure development, rising demand in the construction sector, and expansion in manufacturing activities.

02 What are the challenges in the Vietnam Steel market?

The major challenges in the Vietnam Steel market include raw material price volatility, stricter environmental regulations, trade barriers, and the need for continuous technological upgradation.

03 Who are the major players in the Vietnam Steel market?

Key players in the Vietnam Steel market include Hoa Phat Group, Pomina Steel Corporation, Vietnam Steel Corporation (VNSTEEL), Nam Kim Steel, and Southern Steel Company.

04 What are the main growth drivers of the Vietnam Steel market?

The growth of the Vietnam Steel market includes substantial government investment in infrastructure projects, the expansion of the manufacturing sector, significant foreign direct investment, and the growth of the automotive industry.

Why Buy From Us?

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.